On March 9, 2018 Brian Robert Sodi aka ‘Mailman’ was arrested and criminal and civil charges were announced against him. See the SEC press release and the Department of Justice press release. I have been behind in my blogging and did not realize just how important Brian Sodi allegedly was to the pump and dump industry until I finally got around to reading the criminal indictment and the SEC complaint.

How did Sodi acquire the nickname “mailman”? According to the SEC complaint he ran a large number of stock promotions (both online and physical mail) for 17 years.

91. From 1998 through at least 2015, Sodi’s Penny Stock Promotion Platform was a significant disseminator of penny stock promotional materials, handling, at its peak, as many as two dozen or more such campaigns annually

First, the allegations from the above-mentioned press releases. I start with excerpts from the DoJ press release:

A ten-count indictment filed in U.S. District Court charges BRIAN ROBERT “Mailman” SODI, 46, of Boca Raton, with conspiracy to commit securities fraud and mail fraud, and related charges.

…

According to the indictment, Sodi used his Florida-based publishing houses to distribute deceptive promotional mailers recommending the purchase of select penny stocks, while hiding from potential investors that he secretly was selling the stocks he was urging them to buy. The indictment also charges that Sodi obscured his involvement in the scheme by using offshore accounts and intermediaries to launder the proceeds of his fraud back to himself and his publishing houses.

According to the indictment, Sodi conducted his scheme as follows:

He would acquire shares of a publicly-traded stock, positioning himself to benefit from selling the shares at inflated prices. Sodi would try to induce the public to purchase the stock by developing and disseminating promotional and marketing mailers that exaggerated the stock’s prospects for growth and urged readers to purchase it. The mailers would falsely and deceptively conceal and fail to disclose that Sodi intended to sell the stock he was urging others to buy. After the stock price rose, Sodi would sell the stock for a profit.

Sodi hid his ownership interest in the promoted stock by trading through Arliss, a Swiss account, instead of through a brokerage account held in his own name. He brought the proceeds of his fraud back to himself and his publishing houses through offshore accounts held by firms in Switzerland, the Cayman Islands, and elsewhere.

Now excerpts from the SEC press release:

The SEC’s complaint alleges that Brian Robert Sodi, known in penny stock circles as “Mailman” for his pervasive participation in direct-mailed penny stock promotions, committed a fraud known as scalping. He allegedly disseminated promotions recommending the purchase of the stocks in Southern USA Resources Inc. and Goff Corporation without disclosing he owned shares and planned to sell them through a foreign bank. Sodi also allegedly hid from investors that he was being paid in stock for one of these promotions. According to the SEC’s complaint, Sodi proceeded to unload hundreds of thousands of his own shares to the detriment of other investors who bought in to the hype.

…

The SEC’s complaint filed February 26 charges Sodi and two of his publishing houses, Capital Financial Media LLC and List Data Solutions LLC, with violating Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934 and Sections 17(a) and (b) of the Securities Act of 1933. The complaint also charges Sodi with violating Section 13(d) of the Exchange Act and Rule 13d-1 as well as Sections 5(a) and (c) of the Securities Act. Among other things, the complaint seeks an accounting of all of Sodi’s and his entities’ sales of all U.S. penny stocks that Sodi’s platform promoted within the last five years.

Perhaps most interestingly, the list of domestic and foreign regulatory agencies that assisted in the investigation is long:

The SEC appreciates the assistance of the U.S. Attorney’s Offices for the Northern District of Alabama, District of New Jersey, Eastern District of New York, and Eastern District of Virginia as well as the Criminal Fraud Section of the U.S. Department of Justice, Federal Bureau of Investigation, U.S. Postal Inspection Service, U.S. Department of Homeland Security, Alabama State Securities Commission, Financial Industry Regulatory Authority, Alberta Securities Commission, British Columbia Securities Commission, Cayman Islands Monetary Authority, the Cyprus Securities and Exchange Commission, Dubai Financial Services Authority, Guernsey Financial Services Commission, Hong Kong Securities and Futures Commission, Liechtenstein Financial Market Authority, the Malta Financial Services Authority, the Mauritius Financial Services Commission, Investigation Section of the Financial Services Regulation Division of the Government of Newfoundland and Labrador, Ontario Securities Commission, Québec Autorité des Marchés Financiers, Monetary Authority of Singapore, Swiss Financial Market Supervisory Authority, United Arab Emirates Securities and Commodities Authority, and United Kingdom Financial Conduct Authority.

There are three court cases that have been generated by this so far. The first (and least interesting) is United States v. Sodi (9:18-mj-08088) in the US District Court of the Southern District of Florida. All my links to court cases in this post are to the freely-available docket on CourtListener.com. In addition to the docket, some of the court documents are available to download from that website for free.

The criminal indictment was originally filed in the US District Court, Northern District of Alabama before being removed to the Southern District of Florida — where it was promptly transferred back to Alabama. My guess is that the only reason for the brief removal of the case to Florida was because Sodi was arrested there so therefore bond had to be set there. On March 8, 2018, was released on $250,000 bond (pdf).

The second case is Securities and Exchange Commission v. Sodi (5:18-cv-00313) in the US District Court, Northern District of Alabama. Read the complaint (pdf). As is normal when a defendant is facing parallel civil and criminal charges, Sodi and his companies (Capital Financial Media, LLC and List Data Solutions, LLC) filed a motion to stay the proceedings of the civil case while the criminal case is litigated. From that motion:

Pursuant to Rule 7 of the Federal Rules of Civil Procedure, Defendants Brian Robert Sodi (“Sodi”), Capital Financial Media, LLC, and List Data Solutions, LLC (collectively, “Defendants”), respectfully move the Court for an order staying this matter pending resolution of the criminal case against Sodi in this District.

On June 28th lawyers for the SEC and the defendants had a telephone conference to discuss the motion to stay. On June 29th the judge ordered:

Consistent with discussion on the record during the telephone conference on June 28, 2018 in this matter, on or before July 20, 2018, the parties shall please submit a proposed partial stay order that addresses the Fifth Amendment concerns in this case. The Court STAYS the defendants’ obligations to respond to the complaint in this matter until the Court reviews the parties’ joint submission and enters an appropriate order. Signed by Judge Madeline Hughes Haikala on 6/29/2018.

The third and most important case is United States v. Sodi (5:18-cr-00056) in US District Court, Northern District of Alabama. Read the criminal indictment (pdf). The indictment was filed under seal on February 22, 2018.

I will skip discussion of the indictment to briefly address the other filings in the case so far, most of which are procedural and uninteresting. Unsurprisingly, both sides moved for the case to be ruled complex (which gives both sides more time to prepare for trial) and the judge ordered that motion approved. From the motion:

A first production of discovery has already been delivered to the defense and further productions are being prepared. The Government estimates that the organized discovery ultimately made available to the defense will amount to at least 100 gigabytes of data, mostly in the form of thousands of documents, with additional materials to be made available for inspection or copying.

A telephone status conference

has been scheduled for July 30, 2018 to discuss the timeline for pretrial motions, plea notification, and trial.

One interesting fact garnered from the government’s motion for alternative victim notification procedures (pdf):

The Indictment alleges that Sodi participated in such fraud schemes involving four separate stock tickers during 2012 and 2013.

Because the frauds alleged in the Indictment were directed at influencing the stock price of each of the targeted stocks, and thereby influencing the market for the stocks as a whole, the number of victims harmed by the defendant’s activities reaches far beyond the typical range for ordinary financial fraud cases. The Government currently estimates that 48,848 investors, in the United States and elsewhere, purchased manipulated stock during Sodi’s frauds.

Considering that the same people would tend to trade many different pumps, rather than dividing 48,848 by 4 to get 12,000 traders/investors during each pump and dump, I would estimate 24,000 traders/investors traded each of the stocks Sodi is alleged to have promoted.

The Indictment

We return to review the indictment (pdf). I will excerpt what I think are the most important parts of the indictment. First, the people and entities involved:

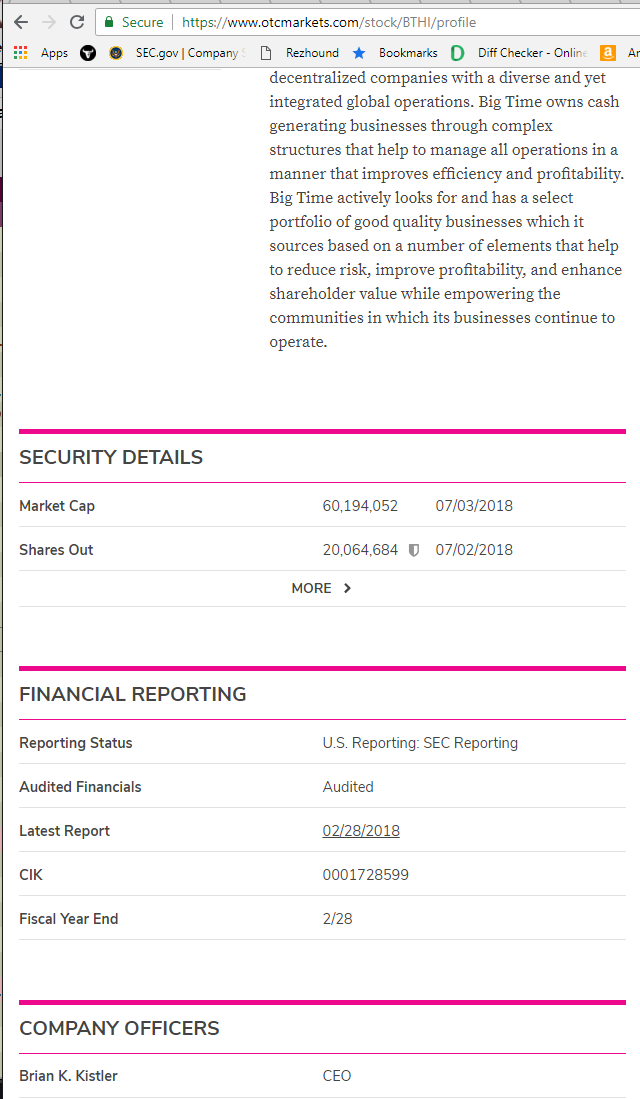

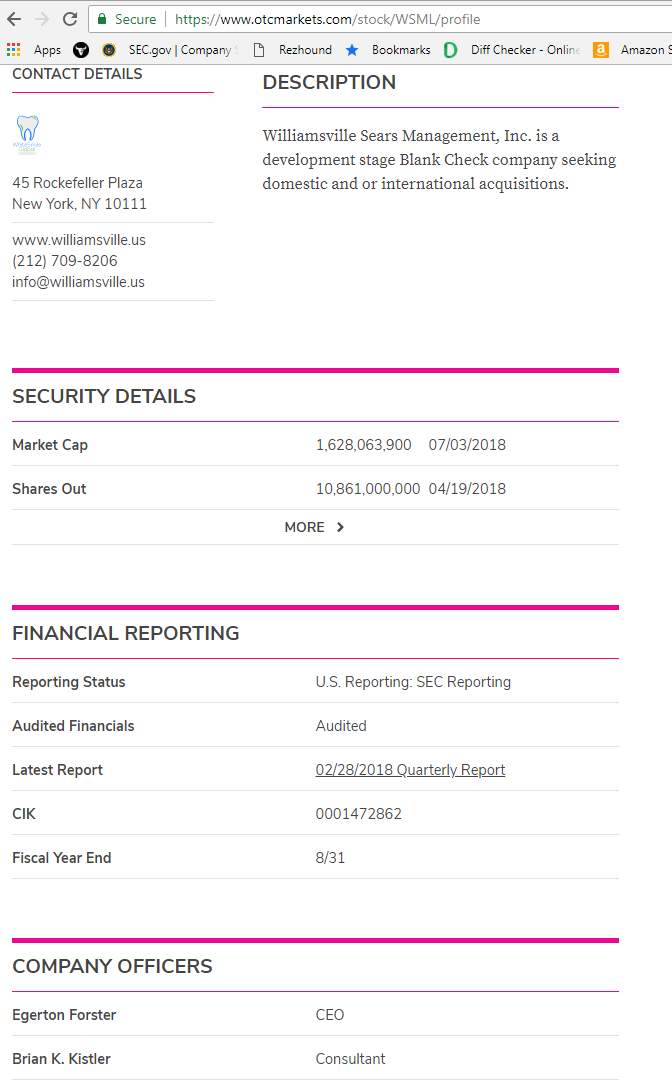

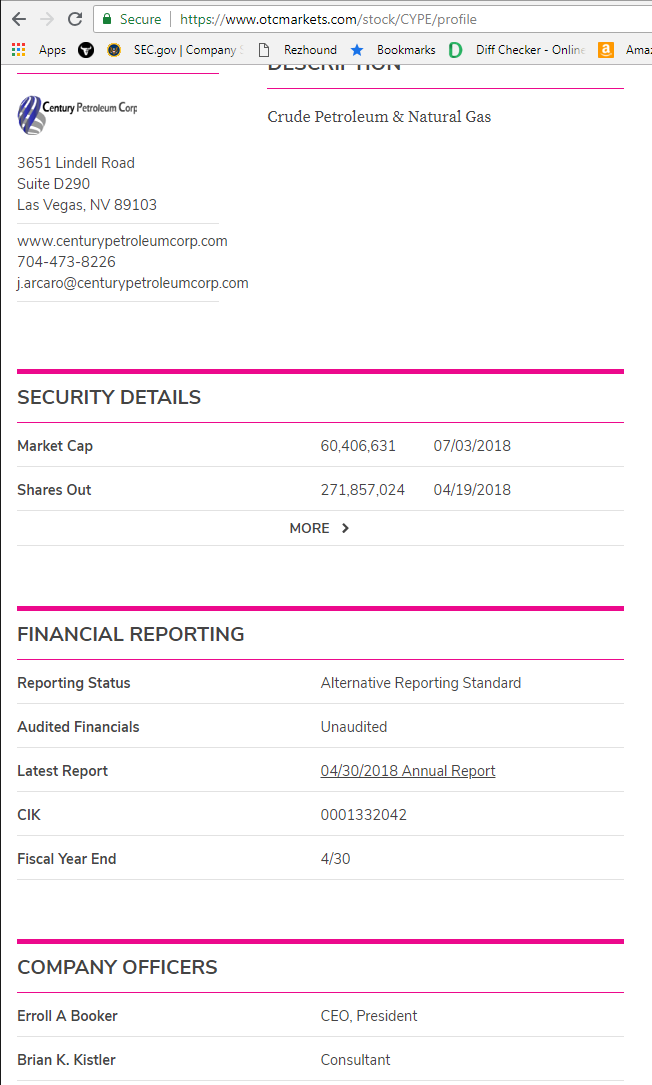

c. The defendant, BRIAN ROBERT SODI, known to others involved in penny stock fraud as “Mailman,” personally controlled companies Capital Financial Media, LLC (CFM), List Data Solutions, LLC (LDS), GLJ Holdings, LLC (GLJ), Trinity Investment Research, LLC (TIR), and other companies using the same business address in Delray Beach, Florida. BRIAN ROBERT SODI and his entities were involved in penny stock promotion s, primarily through the distribution of mailers by postal mail, email, and online advertising.

d. Cooperating Witness 1 (CW-1) and Cooperating Witness 2 (CW-2) were co-conspirators with BRIAN ROBERT SODI as described below

e. Arliss International, Inc. (Arliss) was a corporate entity incorporated in the British Virgin Islands in and around October 2009. BRIAN ROBERT SODI used Arliss to scalp stock during the pump-and-dump schemes described in this Indictment. Although Arliss’s manager was nominally an official of EuroHelvetia Trustco S.A. (EHT), a wealth administration firm headquartered in Geneva, Switzerland, Arliss was in fact used by and operated for the benefit of BRIAN ROBERT SODI.

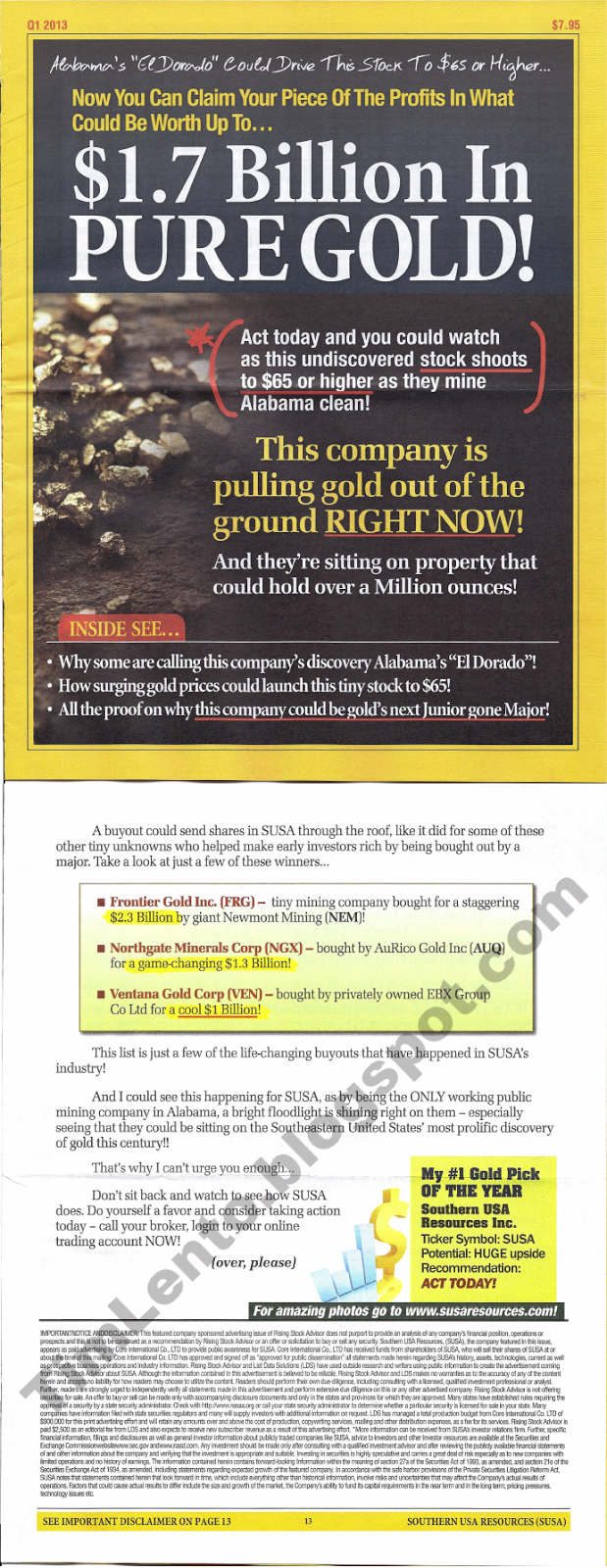

f. Southern USA Resources, Inc. (SUSA) was a Delaware corporation doing business in Ashland, Alabama, in Clay County, within the Northern District of Alabama. From in and around 2012 to in and around 2013, SUSA operated a gold mine in the Northern District of Alabama. SUSA registered its common stock with the U.S. Securities and Exchange Commission (SEC) under Section 12 of the Securities Exchange Act of 1934 on or about May 10, 2012. SUSA securities were quoted on OTC Link, an electronic inter-dealer quotation system for over-the-counter securities, under the ticker symbol “SUSA.” SUSA shares were available for public trading until on or about March 1, 2013, when the SEC issued an order suspending trading in SUSA stock. BRIAN ROBERT SODI used Arliss to scalp SUSA stock during a promotion by BRIAN ROBERT SODI’s publishing houses that was executed from in and around 2012 to in and around 2013. On or about November 22, 2013, the SEC revoked SUSA’s registration for various violations of the securities laws.

g. Great Wall Builders Ltd. (GWBU) was a Texas corporation. GWBU common stock was registered with the SEC under Exchange Act Section 12(g) and was quoted on OTC Link under the ticker symbol “GWBU.” BRIAN ROBERT SODI used Arliss to scalp GWBU stock during a promotion by BRIAN ROBERT SODI’s publishing houses in and around 2012.

h. Potash America, Inc. (PTAM) was a Nevada corporation headquartered in Boca Raton, Florida (originally named Adtomize Inc.). PTAM common stock was registered with the SEC under Exchange Act Section 12(g) and was quoted on OTC Link under the ticker symbol “PTAM.” BRIAN ROBERT SODI used Arliss to scalp PTAM stock during a promotion by his publishing houses in and around 2012.

i. Goff, Corp. (GOFF) was a Nevada corporation headquartered in Cork City, Ireland. GOFF common stock was registered with the SEC under Exchange Act Section 12(g). BRIAN ROBERT SODI used Arliss to scalp GOFF stock during a promotion run by his publishing houses in and around 2013. GOFF securities were quoted on OTC Link under the ticker symbol “GOFF” and were available for public trading until on or about June 29, 2013, when GOFF terminated its stock registration.

The main allegations from the indictment are as follows:

6. It was further a part of the scheme that BRIAN ROBERT SODI’s mailers would falsely, deceptively, and misleadingly conceal and fail to disclose the material fact that BRIAN ROBERT SODI intended to sell the very stock that he was urging others to buy.

…

8. It was further a part of the scheme that sometimes, accomplices and co-conspirators of BRIAN ROBERT SODI, both known and unknown to the Grand Jury, would use “match trading,” i.e.,coordinated transactions designed to manipulate the stock price, to deceive investors into believing that the public was actively trading in the stock.

9. It was further a part of the scheme that after the stock price rose, BRIAN ROBERT SODI would sell the stock for a profit.

10. It was further a part of the scheme that BRIAN ROBERT SODI would conceal his ownership interest in the promoted stock by trading through Arliss, a Swiss account, instead of through a brokerage account held in his own name.

11. It was further a part of the scheme that BRIAN ROBERT SODI would repatriate the proceeds to himself and his publishing houses through offshore accounts held by firms in Switzerland, the Cayman Islands, and elsewhere.

THE CONSPIRACY TO COMMIT SECURITIES FRAUD

12. From in and around 2012 through in and around 2013, all dates inclusive, BRIAN ROBERT SODI, together with CW-1, CW-2, and others known and unknown to the Grand Jury, conspired to defraud investors in the Northern District of Alabama and elsewhere through the fraud scheme described above by executing trades of SUSA stock.

The SEC complaint (pdf) against Sodi and his companies includes some other details not in the indictment:

IT IS LIKELY THAT SODI HAS ENGAGED IN ADDITIONAL

SCALPING FRAUD WITHIN THE LAST FIVE YEARS

Sodi for Years Had Access to Administrative Firm A’s Network of Offshore Accounts

83. Sodi made regular use of Swiss Administrative Firm A – administered accounts from as far back as 2005 and continuing through at least 2015, as demonstrated by, among other things:

a. both Front Company A and Front Company B being Swiss Administrative Firm A-administered accounts;

b. a third, older account (“Front Company C”), which was active from at least early 2005 through early 2010, and which was also Swiss Administrative Firm A-administered – having been used repeatedly to make payments for Sodi’s benefit to many of the same persons and entities to which Front Company A likewise made payments, including parties who designed, built and landscaped Sodi’s vacation home on Nicaragua’s Pacific Coast, “Casa Sodi”;

c. Swiss Administrative Firm A itself having sent at least one wire, on September 8, 2010, to Sodi’s very same “player account” at the very same Casino to which Front Company A also wired funds (as alleged in paragraph 28 above);

d. other Swiss Administrative Firm A-administered accounts, including “omnibus” accounts, transferring funds to, and/or receiving funds from, the Front Company A account; and

e. other Swiss Administrative Firm A-administered accounts wiring funds to reload the very same Swiss Visa Card that Front Company B, as alleged in paragraph 81.c above, wired funds to reload.

After that section the SEC complaint details alleged scalping in PTAM and GWBU in 2012. One alleged detail of note (emphasis mine):

At the time of these purchases, Sodi knew that the massive GWBU promotional campaign his Penny Stock Promotion Platform had prepared was about to launch, and that it would also coincide and be coordinated with a massive APS campaign likewise promoting GWBU.

The complaint continues to allege other stocks scalped after 2013, although it lists only one stock, Graham & Hill Industries (GHIL):

88. In addition to the Front Company A and Front Company B-linked funds that were routed circuitously to Sodi’s CFM entity in April 2014 via Hong Kong Account A, as alleged in paragraph 81.b above, other funds followed a similar path. These include six transfers totaling $950,000 between June 18 and September 22, 2014 from Hong Kong Account A to Sodi’s LDS entity.

89. Sodi’s Penny Stock Promotion Platform booked all $950,000 of the aforementioned wires from Hong Kong Account A as income relating to the Sodi Platform’s promotion of a marijuana stock called Graham & Hill Industries (GHIL). Every penny of this $950,000 however, was first sent to Hong Kong Account A by the very same account – which happened to be at a Cayman Islands bank – that was selling GHIL stock into the price and volume rises generated by that touting campaign. Moreover, every penny of this $950,000 was funded by sales of GHIL stock.

The SEC complaint also alleges that Sodi lied to SEC staff:

93. During the staff’s investigation leading to the filing of this action, Sodi appeared for testimony. During that testimony, Sodi made false statements, including claims that he (i) never had, and never was given the use of, any foreign accounts; (ii) never received or shared, directly or indirectly, in any proceeds of any sales of any of the stocks his publishing houses promoted; and (iii) had never – apart from a single instance over twelve years ago – been paid in stock for running a promotional campaign.

My Records of CFM and LDS stock promotions

I have collected a large number of records of stock promotions on this blog. While this collection is not exhaustive, I do make sure to collect disclaimer info and details of the promotion for each big promotion I have blogged about. Below are all the stocks not mentioned in the SEC complaint or indictment for which I have records showing CFM or LDS as being involved in the promotion. I blogged about many of these but many of the promotions below are linked only to archived webpages at The Internet Archive showing the promotion; others are linked to PDF copies of the online landing pages promoting the stocks that I made at the time of the promotion.

Note that my inclusion of the promotions in this below list does not mean that I believe that Sodi or his companies violated the law in promoting these companies — it is possible to legally promote a company — I only indicate that he and/or his companies promoted these stocks. Dates below are approximate — many of these promotions ran for many months.

Green & Hill Industries (GHIL): List Data Solutions (June, 2014)

Mining Metals of Mexico (WIIM): List Data Solutions (April, 2014)

Black River Petroleum (BRPC): Capital Financial Media (April, 2014)

Guar Global (GGBL): List Data Solutions (December, 2013)

Amazonica Corp (AMZZ): Capital Financial Media (November, 2013)

Xumanii Corp (XUII): Capital Financial Media (July, 2013)

Lot78 Inc (LOTE): Capital Financial Medial (March, 2013)

PacWest Industries (PWEI): Capital Financial Media (March, 2013)

Swingplane Ventures (SWVI): Capital Financial Media (February 2013) (Thanks to Tim Lento for the scan of the mailer)

Graphite Corp (GRPH): List Data Solutions (February 2013)

Lifetech (LTCH): Capital Financial Media (November, 2012)

Stevia Corp (STEV): Capital Financial Media (September, 2012)

Stevia Nutra (STNT): Capital Financial Media (August, 2012)

Boldface Group (BLBK): Capital Financial Media (August, 2012)

American Energy Development (AEDC): Capital Financial Media (July, 2012)

Psychic Friends Network (PFNI): Capital Financial Media (May, 2012)

Sunpeaks Ventures (SNPK): Capital Financial Media (April, 2012)

North Springs Resources (NSRS): Capital Financial Media (January, 2012)

Xcelmobility (XCLL): Capital Financial Media (January, 2012)

White Smile Global (WSML): Capital Financial Media (November, 2011)

TakeDown Entertainment (TKDN): Capital Financial Media (September, 2011) (Archived copy of promotion landing page)

Allezoe Medical (ALZM): Capital Financial Media (July, 2011) (Archived copy of promotion landing page)

Portage Resources (POTG): Capital Financial Media (June, 2011)

Xinde Technology (WTFS): Capital Financial Media (June, 2011)

OncoSec Medical (ONCS): Capital Financial Media (May, 2011)

First American Silver (FASV): Capital Financial Media (April, 2011)

Avatar Ventures Corp (AVVC): Capital Financial Media (April, 2011) (Archived copy of promotion landing page)

Kunekt Corp (KNKT): Capital Financial Media (February, 2011)

Hiroyoshi Worldwide (HHWW): Capital Financial Media (February, 2011)

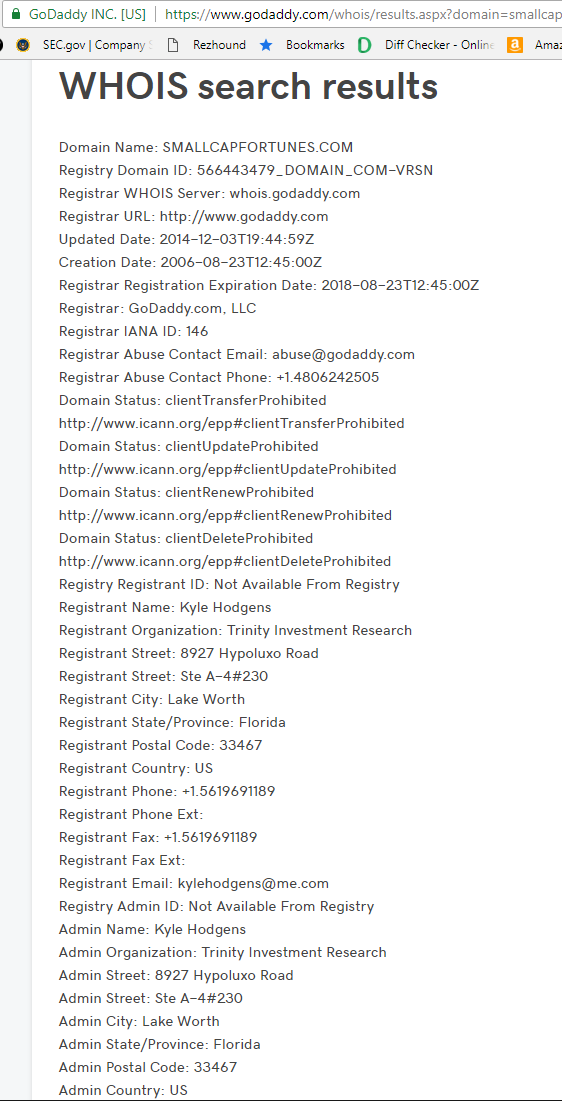

Many more stock promotions run by List Data Solutions and/or Capital Financial Media can be found by using the Internet Archive Wayback Machine on SmallcapFortunes.com although the pump pages were not accessible directly from the main page, so a reader needs to find the direct link to find the archived page. It appears that at least at one point Capital Financial Media LLC owned SmallCapFortunes.com (another messageboard source from someone I trust saying the same thing). The current owner of the SmallCapFortunes.com domain name is Trinity Investment Research LLC of Florida (per current WHOIS search; screen capture).

Correction 2019-6-25: Typo fixed in name of Stevia Nutra. Year 2108 corrected to 2018.

Disclaimer: I have no position in any stock mentioned above. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}