On September 29th, 2017 the Indian film distribution company Eros International PLC (EROS) filed a complaint in New York state supreme court against many different short sellers who have criticized the company.

Below is the text of the company’s press release:

ISLE OF MAN, United Kingdom–(BUSINESS WIRE)–Oct. 3, 2017– Eros International Plc (NYSE: EROS) (“Eros”), a leading global company in the Indian film entertainment industry, today announced that it has filed a lawsuit in New York County Supreme Court against Mangrove Partners, Manuel P. Asensio, GeoInvesting, LLC, and numerous other individuals and entities. The lawsuit alleges the defendants and other co-conspirators disseminated material false, misleading, and defamatory information about Eros and are engaging in other misconduct that has harmed the Company. The lawsuit also names various “John Doe” defendants who will be identified and joined as the case unfolds.

The complaint alleges that Mangrove Partners and many, if not all, of its co-conspirators held substantial short positions in Eros stock and profited when its share price declined in response to their multi-year disinformation campaign. Eros seeks damages and injunctive relief for defamation, trade libel, civil conspiracy, and tortious interference, including but not limited to interference with its customers, producers, distributors, investors, and lenders.

The filing of this lawsuit marks another important step in Eros’ vigorous defense of itself and the Company’s stakeholders. On 25 September, 2017, Eros also reported that the United States District Court for the Southern District of New York dismissed a putative securities class action, with prejudice, that was originally filed in November 2015 and arose from a series of baseless accusations that the Eros complaint alleges were disseminated by short sellers.

The Company previously announced that it retained Michael J. Bowe, a partner of Kasowitz Benson Torres LLP, to investigate and pursue all available legal remedies against those responsible for these blatant attempts at market manipulation. Counsel is continuing its investigation. Anyone with information about those responsible for the dissemination of this disinformation can submit that information confidentially at (212) 506-1777.

The case is 653096/2017 at the New York County Supreme Court. The complaint (pdf) is 115 pages long. First, I’ll start with the defendants, some of whom are well-respected short sellers. I have grouped the defendants below according to firm and employee/employer relationships.

- Mangrove Partners and Nathaniel August

- Manuel Asensio, Asensio & Company Inc, and Mill Rock Advisors Inc

- Geoinvesting, LLC, Christopher Irons, Daniel David, FG Alpha Management LLC, FG Alpha Advisors, and FG Alpha, LP

- ClaritySpring Inc, ClaritySpring Securities LLC, and Nathan Anderson

- John Does 1 to 30

As many of the alleged negative comments at issue were only posted on Twitter, I have linked defendants to their Twitter accounts below:

- Alpha Exposure on SeekingAlpha (allegedly Mangrove Partners); @Alpha_Exposure

- @Asensiocom (Manuel Asensio)

- @Geoinvesting,@DanGeoinvesting (Dan David), @dan_fgalphamgmt (FG Alpha Management LLC / Dan David), @QTRResearch (Chris Irons)

- @ClarityToast (Nathan Anderson)

- The most prominent John Doe is @Unemon1. Other John Does are @HindenburgRes, Spotlight Research (writer on SeekingAlpha), and Orange Peel Investments (writer on SeekingAlpha).

Here is a full listing of all the John Does (from the complaint; emphasis added by me):

34. Defendant John Doe No. 1 refers to the individual or entity, whose identity is

presently unknown to Eros, behind the pseudonym “Spotlight Research.”

35. Defendant John Doe No. 2 refers to the individual or entity, whose identity is

presently unknown to Eros, behind the pseudonym “Orange Peel Investments.” Orange Peel

Investments purports to be a “family office” (or “family fund”) based in New York, New York.

36. Defendant John Doe No. 3 refers to refers to the individual or entity, whose

identity is presently unknown to Eros, behind the pseudonym “Parke Shall,” a purported

employee in the retail and consumer goods division of Orange Peel Investments and an

“anonymous contributor” for Orange Peel Investments’ two Seeking Alpha articles on Eros.

37. Defendant John Doe No. 4 refers to the individual or entity, whose identity is

presently unknown to Eros, behind the pseudonym “Thom Lachenmann,” a purported employee

in the technology division of Orange Peel Investments and an “anonymous contributor” for one

of Orange Peel Investments’ Seeking Alpha articles on Eros.

38. Defendant John Doe No. 5 refers to the individual or entity, whose identity is

presently unknown to Eros, behind the pseudonym “Unemon.”

39. Defendant John Doe No. 6 refers to the individual or entity, whose identity is

presently unknown to Eros, behind the pseudonym “Hindenburg Research.”

40. Defendants John Does Nos. 7-9 refer to Mangrove’s or August’s affiliate(s), or

any related investment fund(s) owned in whole or in part by Mangrove or August, that Mangrove

or August used between January 1, 2015 and the present to short Eros’ stock, whose identities

are presently unknown to Eros.

41. Defendants John Does Nos. 10-12 refer to the Asensio Defendants’ affiliate(s), or

any related investment fund(s) owned in whole or in part by the Asensio Defendants, that the

Asensio Defendants used between January 1, 2016 and the present to short Eros’ stock, whose

identities are presently unknown to Eros.

42. Defendants John Does Nos. 13-15 refer to the GeoInvesting Defendants’

affiliate(s), or any related investment fund(s) owned or in whole or in part by the GeoInvesting

Defendants, that the GeoInvesting Defendants used between 2013 and the present to short Eros’

stock, including but not limited to F.G. Alpha Management, LLC, FG Alpha Advisors, LLC and

FG Alpha, L.P., whose identities are presently unknown to Eros.

43. Defendants John Does Nos. 16-18 refer to the ClaritySpring Defendants’

affiliate(s), or any related investment fund(s) owned in whole or in part by the ClaritySpring

Defendants, that the ClaritySpring Defendants used between January 1, 2017 and the present to

short Eros’ stock, whose identities are presently unknown to Eros.

44. Defendants John Does Nos. 19-30 refer to other individuals or entities, whose

identities are presently unknown to Eros, who work with or at the direction of Defendants.

Below are references to pseudonymous or anonymous Twitter accounts in the complaint (emphasis added by me):

10. Defendants, in a tactic they used repeatedly throughout their conspiracy, created

an “echo chamber” for Asensio, Spotlight Research and Orange Peel Investment’s lies using the

social media site Twitter. Defendants exploited Twitter’s ability to disperse attention-grabbing

sound bites and buzzwords to a global Internet audience, and they created anonymous Twitter

shell accounts to multiply and spread their false and misleading allegations even further.

…

56. To further their scheme, Defendants used Twitter, which has a number of features

that make it the ideal platform for Defendants’ disinformation. Twitter allows its users to post

anonymously, and thus escape repercussions for false content. Twitter also allows its users to

publish posts, called “tweets,” that are public to any Internet user (not just those registered with

Twitter). Other users can then republish those tweets, called “re-tweeting.” Further, Twitter

allows users to “like” a tweet; the total number of “likes” and identities of the users who “liked”

a tweet are displayed at the bottom of each tweet. Users can thus take advantage of these

features, as Defendants have done, to create the appearance of more interest in a particular story

than there actually is, thus constructing an echo chamber.

…

215. Moreover, the Asensio Defendants fabricated Twitter aliases to further

reverberate their false, misleading and highly offensive themes. One such alias, “Forest Gump,”

joined Twitter in June 2016, at the precise time period Defendants re-commenced their short and

distort scheme. Forest Gump has only ever published 12 tweets. All of his tweets except for one

were negative commentary on Eros; in his standalone non-Eros tweet, Forest Gump reached out

to anonymous short-seller “Unemon” with the cryptic request, “Can you follow please.” A

sample of Forest Gump’s 11 Eros-related tweets, which all respond to pro-Eros tweets, reveals

that he attempted to spread salacious falsehoods about Eros’ management and to defend Asensio

under the guise of an independent twitter user.

216. Further, an anonymous user acting under the guise of the alias “Market Farce” resurfaced

on Twitter to hype Asensio’s and other conspirators’ lies, including during phases when

those defendants laid dormant. Market Farce’s false and defamatory tweets include, among

other fictions, the baseless assertion that Eros’ accounting practices warrant SEC scrutiny:

…

288. Defendants, in coordinated fashion, again amplified the baseless concerns they

touted in articles and blog posts using Twitter, including through new anonymous aliases such as

“Lolwut02” and “mboom1991.”

…

293. Moreover, Defendants fabricated Twitter aliases to further reverberate their false,

misleading and highly offensive themes. One such alias, “Lolwut02,” joined Twitter in May

2017. Lolwut02 has only ever published six tweets, all on May 23, 2017 and related to Eros. In

one tweet, Lolwut02 responds to Unemon’s derisive tweet concerning a securities filing by Eros

International Media with the mocking question, “[t]hey do this every year?” In another tweet,

Lolwut02, purports that it is “getting kind of nervous” at the baseless prognosis of the

Company’s looming liquidity crisis. Another alias, “mboom1991,” joined Twitter in June 2017.

Since then, mboom1991 has published zero tweets of his own but consistently rubber-stamps

Unemon’s negative tweets about Eros by “liking” them.

I cannot find Forest Gump on Twitter. Here is the link to Market Farce. Lolwut02 is on Twitter but shows no tweets. Mboom1991 has two tweets and 106 likes.

Regarding this assertion from the complaint: “Market Farce’s false and defamatory tweets include, among

other fictions, the baseless assertion that Eros’ accounting practices warrant SEC scrutiny:” I present without comment the report from ProbesReporter (John Gavin) on his inquiry into an SEC investigation into Eros.

Posted without comment. Our recent report on Eros International also free. No positions – never have. $EROS https://t.co/LDxJpalSWt pic.twitter.com/qMyd5o8Oo0

— Probes Reporter® (@probesreporter) October 3, 2017

Read the full ProbesReporter report on Eros (pdf).

One of the interesting things about this suit is how Eros used FOIA requests to purportedly identify Mangrove Partners / Nathaniel August as being behind Alpha Exposure:

67. Specifically, Alpha Exposure disclosed in a June 21, 2013 Seeking Alpha article

that it submitted a FOIA request letter to the SEC concerning Uni-Pixel, Inc. (“Uni-Pixel”).

Alpha Exposure’s article hyperlinked to a partially redacted response letter from the SEC, which

redacted its true identity, but did not redact the fact that the SEC received Alpha Exposure’s

request on June 10, 2013 and denied it in full.

68. The SEC, in turn, keeps public FOIA “logs” that record metadata for the FOIA

requests that it receives. FOIA logs are public and available on the SEC’s website.2 The

metadata recorded by FOIA logs reflect information such as the requestor’s name, the subject of

the request (e.g., company name), the date the SEC receives a request, the date it closes a request

and its final disposition.

69. Here, the SEC’s public FOIA records could not be clearer about the identity of

“Alpha Exposure.” The log dated FY 2013 reveals that the SEC received a FOIA request

concerning Uni-Pixel on June 10, 2013, the same date that the SEC received Alpha Exposure’s

request, and that the request was made by someone named “August, Nathaniel” of “Mangrove

Partners.” The log further reveals that August’s request was “[d]enied in full” and closed on

June 21, 2013, which again conforms to the SEC letter that Alpha Exposure hyperlinked in its

June 21, 2013 Seeking Alpha article.

70. Moreover, the same SEC log shows that the only FOIA request concerning UniPixel

in all of FY 2013 was from “August, Nathaniel” of “Mangrove Partners.” This irrefutable

fact, coupled with Alpha Exposure’s June 21, 2013 article, amount to conclusive proof that

August and Mangrove are, in fact, “Alpha Exposure.”

71. “Alpha Exposure” again leaked its identity through a slipshod admission in a

November 19, 2015 post on its blog (https://alphaexposure.wordpress.com/). In that post, Alpha

Exposure, after publicizing a FOIA letter it had sent the SEC demanding information on Eros,

divulged that its “last” FOIA request to the SEC concerned Uni-Pixel – which, as the SEC’s

FOIA log reveals, was made by none other than August himself

After reading this I would warn anyone considering submitting a FOIA request to not submit it in their own name but have an attorney submit it for them.

I will not rehash the details of the short sellers’ accusations against Eros International other than to say that there are many different accusations of impropriety. Here is a listing of all of the negative articles published about Eros referenced in the complaint (that I found). Please note that I take no position on whether any of these articles or the allegations in them are true or not.

Unemon1 blog posts on SeekingAlpha

EROS Is Everything But The Netflix Of India. I Honestly Believe This Company Is Going Down! (3/30/2017)

Eros Worldwide Pledged Shares In Eros Intl Media As Collateral Last Week: Liquidity Problems And Lack Of Alternatives Never Seemed So Real To Me (4/6/2017)

LIQUIDITY CRISIS AT EROS INTERNATIONAL IS REAL: HERE COMES THE PROOF! (5/10/2017)

EROS: Desperately Raising Cash And At The Same Time Buying Assets From Insiders. How Messed Up Is That? IMO: A LOT! (6/28/2017)

Alpha Exposure articles on SeekingAlpha

Unlike The Name, Investors Should Not Love EROS (10/30/2015)

Eros: Return Of The Short Seller (2015) (11/10/2015)

Eros: Is The Game Finally Over? We Think So (11/13/2015)

Eros: Revising Our TopCo Analysis (11/20/2015)

Eros: Roll The Credits (8/14/2017)

Manuel P. Asensio articles on SeekingAlpha

EROS’s ‘Dozen Unknown’ Unaudited Subsidiaries Out-Earn ‘Big Name’ Grant Thornton ‘Audited’ Parent (6/8/2016)

Eros Backs Away From Skadden’s Independent Review (6/8/2016)

ErosNow’s ‘Fullerton Deal’ Brings ‘New Round Of Questions’ (6/9/2016)

EROS: Prem’s Dilemma (7/18/2016)

Hindenburg Investment Research articles on SeekingAlpha

Eros Earnings Review: An Abundance Of Red Flags (8/2/2017)

Eros International: New Receivables Accounting Red Flags (8/24/2017)

Orange Peel Investments articles on SeekingAlpha

Continue To Avoid Eros After Terrible Earnings (2/18/2016)

New Red Flags About Eros Raised (6/9/2016)

Eros Stock Bump With Lack Of Cash Generation Makes It Attractive Short (7/4/2016)

Eros: Shelf Indicates Possible Coming Equity Issuance, Continued Pressure On Stock (8/2/2017)

Eros: Take Rumors With A Grain Of Salt (8/7/2017)

Geoinvesting articles on Geoinvesting.com

Eros’ Failed Bond Offering, S&P Downgrade, Could Signal a Very Real Liquidity Crisis (3/16/2017)

Eros Associated Execs Admit on Hidden Camera They Will Launder Money Through Films (3/29/2017)

Eros International (EROS): Critical Warning Signs Ahead of Upcoming Annual Report? (7/14/2017)

Spotlight Research articles on SeekingAlpha

EROS’s Secret: Undisclosed Related Party Links In The UAE? (6/9/2016)

Globus: EROS’s Elephant In The Room (8/18/2016)

Eros, not content to hit back with a simple libel/defamation suit, alleges in its lawsuit that the short sellers conspired against it. In the complaint the word “conspire” is used three times while “cabal” is used twice, “conspiracy” is used 13 times, and “conspirator” is used 32 times. I read through most of the complaint and I really don’t understand how any of the evidence provided supports the conspiracy claims.

The first two counts in the lawsuit are the expected (defamation per se and defamation, against all defendants). Count three is against all defendants and is for commercial disparagement (this is a new one to me — basically it is unfairly disparaging a business). Count four is false light (under Pennsylvania law) against Geoinvesting defendants only. Counts five and six are tortious interference and tortious interference with contract, against all defendants. Count seven is the big one, civil conspiracy, against all defendants. Now I am not a lawyer, but I do believe that Eros included the claim of civil conspiracy to be able to expand the scope of discovery and litigate all the claims against the various defendants in one suit, rather than having to file separate suits against each defendant.

The main lawyer for Eros International is Michael J. Bowe of Kasowitz Benson Torres LLP. Michael Bowe, besides having a sense of humor like mine, is most well known (at least among investors/traders) for representing Fairfax Financial against short sellers (this case lasted over a decade). The Fairfax Financial case also involved allegations of a conspiracy of short sellers.

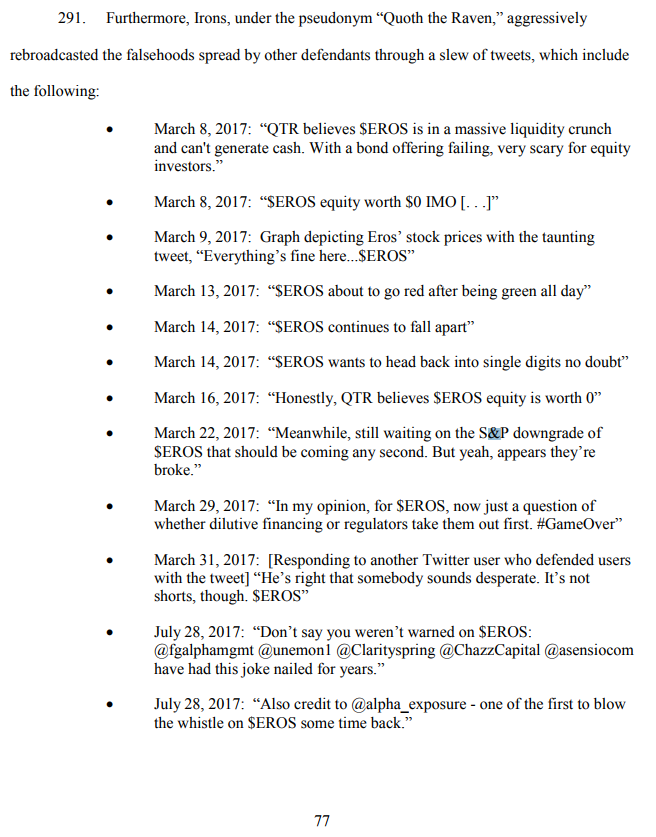

One last note: this case has a couple defendants (Chris Irons and the Clarity Spring defendants) who wrote no articles or blog posts but only tweeted about Eros. Below is a screenshot of the complaint showing Irons’ tweets:

Perhaps the scariest part of this complaint is the following:

86. Irons, using his “Quoth the Raven” alias, defamed and disparaged Eros, including

by redistributing false information about Eros on Twitter.

In other words, Eros International and its lawyers are asserting that merely spreading information on Twitter (commonly done through a retweet rather than an URL link) can qualify as defamation.

If Eros is victorious in its lawsuit (or even if this just drags on for years) this could have a chilling effect on criticism of controversial companies, online in general and in particular on Twitter.

Post updated on 10/4/2017 with links to more articles, more excerpts from complaint on John Doe defendants, and link to ProbesReporter report.

Disclaimer. No position in any stocks mentioned and I have no relationship with anyone mentioned in this post except that I follow some of them on Twitter and respect their work. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.