If you read the papers and watch the news, you may believe that we are in and have been in a subprime mortgage crisis for the last year or so. That is true. Many pundits are also saying that the subprime crisis is nearing its end. That is also true, to a point. Subprime mortgage troubles will not inflict that much more damage on the broader economy. However, prime and Alt-A mortgages with toxic features will cause troubles that will make the current troubles look like a walk in the park. Furthermore, broad-based declines in housing prices will start to wreak havoc on housing markets across the country.

The Cataclysmic Shift

The problem with the housing market bulls is that they are thinking within the framework of past housing downturns. The current downturn is unlike any other since the Great Depression. No other downturn has started with houses so overpriced relative to rents. Few downturns started with such reasonable interest rates. No other downturn saw double digit house price declines across the country. This downturn is different, and it is going to lead homeowners (or homedebtors, as the Irvine Housing Blog calls those who have little equity) to change their behavior in ways that only the pessimists such as myself anticipate.

The problem with most predictions is that they are linear extrapolations of the past into the future. Have global temperatures been rising? They will continue to rise at the same rate. Has crime been increasing? It will continue to increase at a similar rate. The problem is that significant change often comes suddenly. That is why no one who knows anything is worried about the gradual increases in the Earth’s temperature that will occur if global warming continues. What really scares people is the possibility (however remote) that the changes could accelerate or could cause something unexpected to happen (such as the jet stream moving or the ocean currents changing). A thorough review of the history of global temperatures reveals that such cataclysmic change is not unusual.

In the case of housing, the cataclysm will come within the next couple years. It will be fueled by two factors: option ARM mortgage recasts and house price declines. (Slate has a worthwhile take on what will happen, but its analysis is less detailed than mine.)

Why House Prices will Continue to Decline

House prices are elevated relative to rents and relative to incomes, especially in the hottest markets, such as California, Nevada, Florida, and Arizona. However, price increases in middle America have been no less astonishing. One example with which I am all too familiar is the house I just sold in the Saint Louis suburb of Maplewood. Zillow has a decent graph of the house’s value, although it is not completely correct. If you look at the county assessor’s website (and search by the address) you can see that the house sold for $100k back in 1997 and then for $188k in 2004. I just sold it for $165k. Over this period of time few renovations of note were done on the property and the neighborhood did not improve significantly. The employment situation in the area has not changed. So from 1997 to 2004 the house appreciated by 88%, while between 1990 and 1997, during great economic times, the house appreciated by only 25%. In relation to both rents and area incomes, the house is still probably 20% overvalued.

Moving from the anecdotal to the statistical, we can see that this is not an isolated situation. The chart above shows housing starts and permits for the last 30 years. Over this period the population has increased at a fairly steady rate. Since 2003 there have been too many houses built. This will lead inevitably to falling prices.

If you look at the ratio of income to house prices in the above graph (from Piggington’s Econo-Almanac), you will see that house prices are way higher than they should be relative to incomes (while this graph is for one area of California, prices are elevated relative to incomes across most of the country). While creative financing can lead to a bubble in prices, there is no way for house prices to remain unaffordable indefinitely.

Another thing to consider is that house prices remain tethered to rental prices over the long term. If renting is cheaper than buying, people will choose to rent rather than buy and house prices will fall. House prices have never been so much higher than rental prices than they are now. Above is a chart of the ratio of the OFHEO house price index to the CPI-Owner’s equivalent rent.

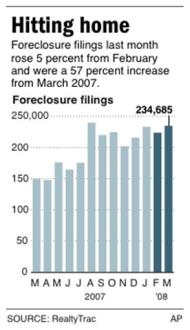

Another factor weighing on prices is the increase in foreclosures. Banks that own foreclosed houses are motivated sellers and they will cut the prices so that they can sell their inventory. Increasing foreclosures will increase supply and decrease prices of transactions. Why pay $200k for a house when your neighbor but his out of foreclosure for $140k? Foreclosures are actually understated because banks often don’t have the manpower necessary to foreclose and sell delinquent properties.

The foreclosure problem will soon get much worse. Considering that it often takes over half a year (and can take much longer) between when a homedebtor falls behind on a mortgage and when the house is repossessed, the current wave of foreclosures began before house prices had fallen significantly. With prices now down 20% in many areas and 30% or more in some areas, the rate of foreclosures will increase drastically over the next year. Those that need to sell and who have little equity will be unable to sell for more than they owe. Short sales are difficult, so foreclosure will be the last resort for many who need to move.

Even though asking prices for houses have fallen dramatically already, they have not fallen nearly enough: witness the low volume of house sales relative to prior years. In the graph below we can see that the spring selling season in San Diego has been a bust, as it has elsewhere (image from the Bubble Markets Inventory Tracker blog).

Option ARM Recasts

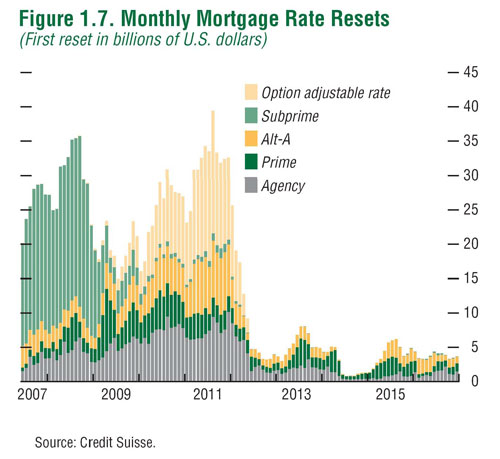

Besides falling house prices, another factor in the coming mortgage crisis is the coming recasts of millions of option ARM mortgages. Most of you will be familiar with the problem of interest rate resets on ARMs (adjustable rate mortgages). This problem is well-known. Almost all ARMs have fixed rates for the first couple years and then the rates reset to market rates. Considering the current low interest rate environment, this problem is likely overblown.

The greater problem, however, is recasts. Option ARMs allow for the choice of the size of the payment. Homedebtors can choose to pay an amortizing payment (such that their mortgage balance is reduced), an interest-only payment, or a negative-amortizing payment, where their mortgage balance increases. Recent data from Countrywide indicates that 71% of borrowers with option ARMs are only making the minimum, negative-amortizing payment. Option ARMs have provisions such that when the mortgage balance exceeds the original mortgage by 10% to 15%, the loan converts into a fully self-amortizing loan. Considering that many of these loans were made over the last few years (beginning in 2005), we should start to see a number of recasts. When a mortgage recasts, the payment size can easily double or triple. Those who could afford their payments before will no longer be able to do so.

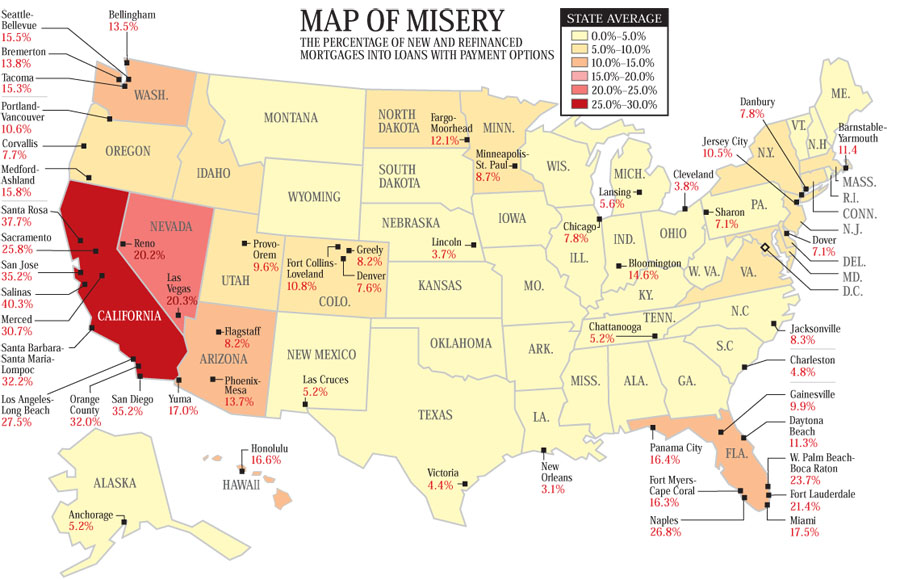

Option ARMs are highly prevalent, especially in the most bubbly markets. See the following map and click on it for a larger version (courtesy of the Irvine Housing Blog):

The Coming Crisis

The coming crisis will be caused by option ARM recasts, falling prices, and banks’ increasing reluctance to lend. The crisis will manifest itself in people simply walking away from houses where their mortgage is worth more than the house. Considering how many people have used home equity loans to remove equity, how many have had negative amortization in their loans, and considering how small down payments became over the last few years, very few homeowners will be left with equity in their houses. Economy.com currently estimates that 9 million households have negative equity. That figure could easily double or triple as house prices fall by another 20% to 30%.

The assumption on the part of mortgage lenders, regulators, and housing market optimists is that as long as people can afford to pay their mortgages, they will. But homedebtors faced with 20% to 30% negative equity will be much better off going through foreclosure than they will paying off their debts. Helping them is the fact that in a number of states, purchase money mortgages are non-recourse debt, meaning that banks cannot sue to recover the money they lose. The sheer number of foreclosures will mean that banks will not have the manpower to go after domedebtors even when they want to do so.

The rising tide of foreclosures caused by people walking away from houses in which they have negative equity will act as part of a positive-feedback loop to increase the rate of price declines. The housing market is not getting better anytime soon and it will soon get much, much worse.