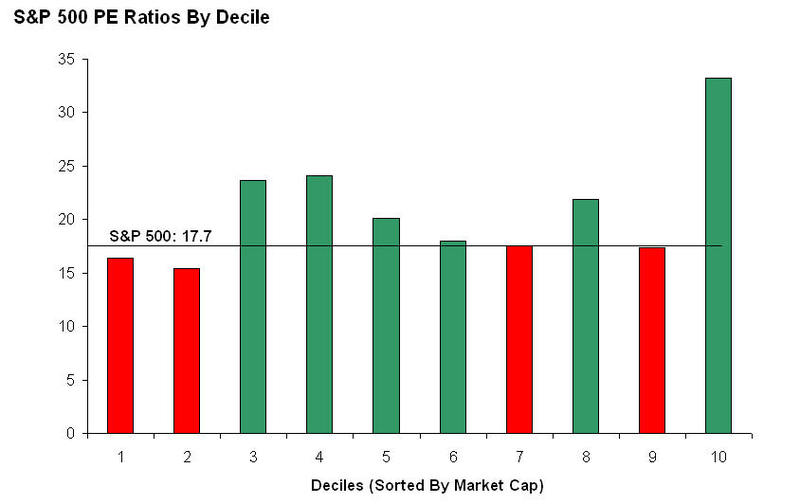

Judging from this graph, larger companies look to be better values now.

The Best Source for Penny Stock Insight

Judging from this graph, larger companies look to be better values now.

I have already mentioned a few of the greatest value investors of our time in this short guide. I want to take a bit of a longer look at the best, though. By examining what Warren Buffet has done, we can perhaps learn from both his mistakes and his successes.

Warren Buffett worked for the father of value investing, Ben Graham. Afterwards, he started multiple investment partnerships with himself as the managing partner, and friends, relatives, and acquaintances as limited partners. In 1967 he bought Berkshire Hathaway, a money-losing textile mill, and in 1969 he closed his investment partnerships.

Buffet made many great investments before buying Berkshire, but it is convenient to start analyzing his record starting with Berkshire. First off, Berkshire Hathaway was probably Buffet’s worst investment: the textile mill never made much money, and Buffet was forced to shut it down in 1985. Until that time, the rest of Berkshire Hathaway, composed of Buffet’s other investments, had to support the textile business.

Why was Berkshire Hathaway (the textile business) a bad investment? Buffet bought it cheap, but he bought a company that had no special competitive advantage; even worse, it was in a dying industry (also a dyeing industry).

Now let’s look at one of Buffett’s successes: Berkshire Hathaway bought shares of The Washington Post Company in 1973. This was a better investment, because it was undervalued, plus its assets were highly desirable. In addition, the management was good. This was quite different from Berkshire Hathaway; Berkshire’s assets, even at the time Buffet acquired the company, were not desirable. Also, the management was not very good, and Buffet had to replace the management of the textile mill.

The rest of the 1970s saw Berkshire Hathaway buy shares of GEICO insurance along with all of National Indemnity Company and Cypress Insurance. All of these are insurance companies.

What’s so special about insurance? There are some details that I cannot address here due to a lack of space, but one of the key reasons why Buffet has bought so many insurance companies is that the stock market tends to undervalue small insurance companies. See the low P/E ratios of, for example, ASI, BER, and UFCS (this does not constitute a recommendation of these companies, however).

Buffet has continued his interest in insurance; since 1990, GEICO was completely bought, General Reinsurance was bought, and many other smaller insurers were bought as well. In fact, much of Berkshire Hathaway’s income is from its insurance businesses.

What can we learn from this? What is important is that we find profitable companies that are undervalued. We won’t find many high-profile companies that are undervalued, and we certainly won’t find many stocks in hot industries that are undervalued. Therefore, many of our investments will be in companies in boring, unglamourous industries, like insurance.

As if to emphasize that point, in recent years Berkshire Hathaway has acquired such exciting companies as Acme Brick, Shaw Industries (a carpet manufacturer), and Clayton Homes (a manufacturer of mobile homes).

One last example of a good move that Buffet made was in buying many Washington Public Power Supply (WPPS) bonds in 1983 and 1984. Two new nuclear units had begun construction but had then defaulted on their bonds. The market reacted and even the price of the bonds secured by the old facilities (that were still generating money to pay off those bonds) fell drastically. There was nothing fundamentally wrong with the old bonds, so they made a nice profit for Buffet. The market will often unduly punish good companies in bad industries, just like with these bonds. That is when adroit value investors will buy.

If you wish to read more about Buffet’s investment style, I highly recommend reading his annual letters to his shareholders, available for free at the Berkshire Hathaway website.

Disclosure: I hold shares of BRK.B and I am also a customer of GEICO. See the disclosure policy.

What would you pay for a gallon of milk? Would you pay $2? $3? Would you pay $4? What if it was very popular milk, and everyone was buying this particular brand of milk? Would you then be willing to pay $5 for a gallon? No?

Why not? Because milk at $5 is overpriced–it’s a bad value. Stop and think about it–why is milk any different from stocks? A stock is not a piece of paper that has no true value that is meant to be traded back and forth among a group of people acting like manic-depressive lemmings. A stock is part-ownership of a company. Companies, like the goods you buy at the grocery store, have a true value.

It is true that companies are more complicated than milk; however, they still have a fair value that can be calculated. Actually, in some ways, companies are simpler to value than milk, because we can measure and attempt to predict the profits they produce and the assets they hold. Measuring the benefits that milk gives us, on the other hand, can be quite hard.

If you agree with what I have just said about the possibility of calculating (albeit approximately) the fair value of a company, then you are well on your way to being a successful value investor. The secret to value investing is this: find a company that is being sold below its true value and then buy it.

It is incredibly simple, and its simplicity puts all of the stock market hucksters to shame. There are many investment newsletters that claim to be able to help you achieve spectacular gains quickly. Their cachet is the complexity of their methods. (See, for example, the Delta Society.) However, the complexity of their methods keeps you from understanding them and deciding for yourself whether they actually work. I’ll admit that some methods of speculation may actually work. However, even the methods that work have large risks, and you can lose a lot of money really quickly. Why not use a simple system that you can understand, a system that works, and a system that you can use without a PhD or 30 hours a week studying, without having to pay for expensive seminars or thousand dollar per year newsletters?

The only thing that is difficult about value investing is that it is not for those who lack ‘intestinal fortitude’. Value investing will often call for buying a stock precisely when everyone else is screaming ‘sell!’ Value investing often requires buying unknown companies in unglamorous business. Value investing will often involve buying stocks that are selling at all-time lows, rather than all-time highs.

Therefore, in value investing, you will not sell a stock just because its market price has gone down (nor should you sell it just because the price goes up). If the price of a gallon of milk goes down, the milk is an even better value. Therefore, you would buy more (up to a point). Likewise with stocks, if a good company is available for half as much, it is twice the value. The only situation which would change that would be if the company’s business were to start deteriorating. Just as you avoid paying any amount for sour milk, you should avoid paying any amount for a bad company (or, at the very least, pay very little and only do so if you are confident the company can turn itself around).

You have probably heard the term ‘contrary investor’ or ‘contrarian’ before. If not, why not look it up on Investopedia? At its heart, the concept of benefiting by going against the crowd is both incredibly stupid and incredibly smart.

Going against the crowd would be stupid when you do it right in the middle of the crowd’s actions. A good example of stupidly going against the crowd would have been going short technology stocks in 1999, just a year before the internet bubble burst. You could have easily lost everything.

So if you want to profit from speculating (benefiting from future stock price moves that you predict), it would be foolish to go against the crowd. But what about value investors? Does being a contrarian hurt or help us?

When everyone is selling, there is usually panic and fear. When there is panic and fear, there is very little reasoned thought. When people are not being reasonable, prices in the stock market will tend to go far away from fair values. In this case, this usually means there is a good chance for a stock to be bought really cheap. It is our job to buy from panicked sellers, and thus make easy money later on when we can sell those same stocks at fair values.

The opposite situation, selling when everyone else appears bullish, applies to speculators but not to us. A smart speculator could have foreseen the bursting of the Internet stock bubble that burst in 2000. Early in that year, there was IPO mania, executives were exuberant, and people talked of naught but their tech stocks. That would indicate that everyone who was going to buy stocks already had. There was no one left to buy, and the stocks had no where to go but down. The smart speculator would then have sold, reaping enormous profits. If he were adventurous, he could have even sold tech stocks short, making even more money.

We would not have acted in the same manner, though. None of those tech stocks were good values in 1999. Value investors may have bought into some of them earlier on, but a value investor will always sell out when prices become way overvalued, before they become obscene.

So when investing, look for areas where others are fearful. If you find those fears to be unfounded, you might find yourself a good investment.

On news that an activist hedge fund has taken a 5% stake. I bought this company a couple months ago at book value. I continue to believe that there is little risk in buying good insurance companies near book value as long as they do not have large exposure to catastrophes.

Disclosure: I hold shares of MIGP. See the disclosure policy. I own other insurers as well, including RTWI, BRK.B, and the preferred stock of QNTA, QNTAP.

Where do I get my stock ideas? Where does anyone get their stock ideas? Well, the simplest and easiest way, besides listening to perennial blowhard Jim Cramer, is to screen for stocks like one would for a car or a washing machine. Since Consumer Reports doesn’t review stocks, we will have to turn to the Yahoo Finance stock screener. MSN money also has a stock screener, and Morningstar does as well. I like Yahoo’s the best, simply because it is the most flexible.

In screening, we can use our usual suspects: P/E, PEG ratio, dividend yield, market cap, price to book ratio, past earnings growth, as well as ROE or ROA. I’m sure you have done this before, so I won’t dwell on it.

By the way, the PEG ratio is what you get when you divide the P/E ratio by percentage annual earnings per share (EPS) growth. Thus, it is a measure of both current value and recent growth. As with P/E ratios, lower PEGs are better. There are a couple in depth articles about PEG ratios at investopedia linked from the above definition.

While you can calculate PEGs using past growth or predicted future growth, I know that analysts’ projections of future earnings are usually wrong. Yahoo Finance includes PEG ratios (listed under key statistics), but they are based on predicted growth, so I ignore them.

There are other ways to search for stocks, though. Since we are value investors, we will oftentimes be the buyers of last resort. When everyone else has sold a stock, and those who hold it are too shell-shocked to care anymore, when a stock is completely boring, we will buy. Of course, that is assuming that we want the company. Sometimes, companies such as this will be on their way to de-listing and bankruptcy. A few of those companies are good companies, perhaps with a few problems, perhaps just in unglamourous industries.

How can we search for companies such as this? Why not check public bulletin boards on the internet? For example, check out (briefly) the message board for XJT at Yahoo. There have only been a few posts in the last month. Both the bulls and the bears are just bored. That is a good sign that the stock is out of favor.

While we cannot sort the stock message boards at Yahoo by the number of posts, if we go to The Motley Fool, we can. Note: you have to complete a free registration to have guest access to Fool Bulletin Boards, although you do not need it just to glance at them, as we will do.

So, go to the Fool BB, and look at the ‘A’ stock boards. We can then sort by number of posts, and look at only those stocks with, say, 10 or fewer posts. We can look each of them up at Yahoo Finance, and then set aside any that have profits and a reasonable P/E ratio for a more detailed look. I did this today and then screened to remove stocks with lackluster PEG ratios.

Of course, since I was browsing through about 100 stocks and going by the past earnings growth of these companies, I was not actually calculating PEG ratios. I just eyeballed it. That is fine, as my goal was to find a few stocks, not 50 stocks. If I missed one or two, that was fine. Screening for stocks on such an abstract criterion as how ‘forgotten’ they is more of an art than a science. I’ll be mentioning a few of these stocks in detail in this and later letters, plus I will track the group as a whole just as an intellectual exercise. If you care to investigate them yourself, here they are: acu, atpl, aea, bcs, ezpw, gnw, hwg, max, nxy, oxm, oxps, ppp, ttm, vlgea, vsl, wlda. See stock quotes on all of them here.

Notice that a few of those (TTM and VSL) do not really belong on this list, as they are Indian stocks, and thus would likely be discussed less here in the US. Now, this is not an ideal screen, and many of these companies are probably a waste of our time (such as HWG, which has a P/E of 1 only because they sold off a huge chunk of their company). That being said, I hope this serves as a good example of a slightly different way to search for stocks.

[This was originally published October 2005 in The Everyday Investor, my defunct investing newsletter.]

Addendum: in the year since I published this article, the stocks mentioned soundly beat the stock market as a whole. Also, now that Motley Fool has its CAPS paper trading game, you can search for unloved stocks by searching CAPS for highly rated stocks that are rated by only a few people.

Sometimes an opportunity hits you over the head and you have to take advantage of it. That has been the case for me with Movie Star Inc (MSI), soon to be merged with Frederick’s of Hollywood. This is an interesting investment because MSI is smaller than Frederick’s, but it was the public company and Frederick’s wanted to go public. They sensed synergies (MSI manufactures store-brand lingerie for Sears and Wal-Mart) so they agreed to a merger. The combined entity will have a lot of cash on hand and will look to drastically increase the number of Frederick’s of Hollywood stores.

There are few better investments in the business world than to find a good brand and then invest money in spreading it. This is exactly what will happen with Frederick’s. The company invented the push-up bra and introduced the thong to the United States. Its water-filled bra is an excellent feat of engineering that offers lifelike feel whilst enhancing cleavage. While the company had a bit of a sleazy image in the past, it has focused for the last few years on updating its image and becoming more mainstream (think Victoria’s Secret).

As always, I encourage you to view the relevant financial data yourself, straight from EDGAR. Following is my pro-forma pro-forma [sic] analysis. I took the pro-forma financials from the proxy statement and used my own pro-forma voodoo on them.

The combined company will have book value of about $60 million (including $20 million in cash it will use to expand). It had pro-forma sales of $190 million for the year ending July 2006. After the merger, there will be $50.8 million shares outstanding. This gives the combined entity a current market cap of $130 million (using $2.55 per share current price).

I get a 2007 estimated EBITDA for the combined entity of $10.6 million. Given an implied enterprisevalue if the deal goes through at the current price of about $108 million, this implies an EV/EBITDA ratio of 12.3x. Frederick’s has 133

stores and looks to increase that by 50 over the next 3 years (a rate of increase of over 16% per year). 34% of Frederick’s sales (not MSI or the combined company pro-forma) are from mail order or internet. Increasing the store count significantly should thus ramp up profits (excluding organic growth) at over 5% per year. I would also expect significant same store sales growth and online sales growth as the company increases advertising. There should also be some synergies since Frederick’s has a brand name and retail presence while MSI actually manufactures lingerie. I have not modeled those synergies. The median peer EV/EBITDA ratio is about 8.0x. I expect MSI to grow significantly faster than its peers over the next few years, so a somewhat higher EV/EBITDA ratio is warranted. At the current price, though, the company seems fairly valued.

While I am not excited at the company’s current price, if it should fall, I will gladly increase my stake. An opportunity to buy a brand like Fredericks for cheap does not come around often.

Disclosure: I own shares of MSI. I always disclose when I have an interest in a stock about which I write, as you can find on my disclosure page. You can see what stocks I own whenever you want (although this may not always be up to date).

More to come later. I need to post a disclaimer before I post anything about stocks.

Michael