On May 15, 2019 the SEC announced a settlement (pdf) with microcap broker Wilson-Davis & Co. for failing to file suspicious activity reports (SARs) about suspicious activity by its clients.

Securities lawyer Laura Anthony described Wilson-Davis in 2016 as one of “only a limited number of clearing brokers” willing to clear penny stocks. Since that time, one of the other clearing brokers mentioned by Anthony, Cor Clearing, agreed in a September 2018 settlement with the SEC to stop accepting the deposit of penny stocks.

Here is the description of Wilson-Davis & Co. from the settlement:

Wilson is a registered broker-dealer located and organized in Utah. It has satellite offices in Colorado, Florida, Arizona, New Jersey, New York, and California. It has been registered with the Commission since 1968, has approximately 7,000-8,000 active customer accounts, and has approximately thirty-two registered representatives. Wilson’s primary business is the liquidation of microcap stocks and is a market-maker in approximately fifty securities.

page 2

There were many failures to file SARs, even in cases where Wilson-Davis closed accounts because of suspicious activity.

9. Although Wilson’s WSPs identify suspicious activity, list red flags, and describe Wilson’s responsibility to file SARs, Wilson failed to adequately conduct AML reviews and to identify, investigate, and report certain suspicious activity related to transactions or patterns of transactions in its customers’ accounts. Accordingly, Wilson failed to file necessary SARs.

10. Wilson’s primary business involves receiving stock in physical form, selling the position, and wiring out the proceeds from the transaction. Although this pattern is a red flag of potentially suspicious activity according to Wilson’s WSPs, Wilson often failed to investigate or to file SARs where necessary on these types of transactions.

11. Wilson failed to investigate or file SARs on numerous transactions in which Wilson’s customers exhibited the red flag pattern of depositing a physical certificate, liquidating shortly after the deposit, and wiring the proceeds.

12. In several instances the conduct reached such a level that Wilson froze or even closed the customer accounts. Even when the suspicious activity caused Wilson to close an account, it never filed a SAR.

page 4

The SEC’s descriptions of the details of deposits and sales of stock in three different companies (referred to as Issuers A, B, & C) are mind-blowing. Below are just the red flags associated with Issuer A:

13. From March 2014 to June 2016 (“relevant Issuer A period”), at least fifty-two different Wilson customers deposited approximately 576,540,673 shares of Issuer A. Many of these customers then liquidated 263,641,501 shares during the same period and wired out the proceeds. Issuer A’s CEO also maintained an account at Wilson.

14. During the relevant Issuer A period, the Commission filed an action against a Wilson customer for manipulating several stocks, including Issuer A. The Commission alleged that from January 24 through February 12, 2014, there was an active promotional campaign involving Issuer A. From January 24, 2014 through February 12, 2014, while the suspicious transactions were taking place, Issuer A’s stock price increased by 573%. Although the Commission’s complaint did not allege the manipulative conduct occurred at Wilson, a Wilson registered representative became aware of the Commission action when a customer emailed him an article discussing the SEC action on August 6, 2014. The registered representative notified the Wilson AML officer of the SEC action.

15. In early 2015, Wilson became aware of a news article that said Issuer A’s CEO and others sold shares of Issuer A through Wilson and broker-dealer B. Wilson requested brokerdealer B statements from Issuer A’s CEO and the other Wilson customers accused of selling. Wilson verified that Issuer A’s CEO and others sold Issuer A through broker-dealer B at the same time as selling at Wilson. Wilson immediately froze the accounts for any transactions in Issuer A. Issuer A’s CEO and others had signed a Wilson form at the time of each Issuer A deposit providing that they would not be permitted to sell Issuer A shares at another firm while also selling shares through Wilson.

16. In October 2015 Wilson’s compliance department told a customer it wanted a new attorney to draft opinion letters regarding Issuer A. Wilson had concerns because of the quality of the attorney opinion letters and because of the approximately sixty-seven deposits of Issuer A securities, this attorney authored fifty-eight attorney opinion letters from thirty-four different Wilson customers. Wilson told the customer that Wilson wanted a new attorney with more of an “arm’s length away from the company.”

17. In 2016, the Commission filed an action alleging that Issuer A and Issuer A’s CEO, among others, perpetrated a scheme to evade the antifraud and registration provisions of the federal securities laws. Wilson sent its customer an email saying that due to the SEC complaint, Wilson would not allow sales or deposits of Issuer A securities. Before filing its action, the Commission had sent ten document requests to Wilson regarding approximately ten customer accounts trading Issuer A securities. Wilson eventually determined the conduct to be concerning enough to close all accounts of the individuals named in the Commission’s complaint. Wilson also closed the accounts of family members and several employees of Issuer A.

18. Although many of Wilson customers engaged in transactions of $5,000 or more involving Issuer A that exhibited the red flag activity described above of depositing physical certificates, liquidating the shares, and wiring the proceeds, Wilson never filed a SAR in regard to customer transactions involving in Issuer A. In addition, there were numerous other red flags associated with these transactions. Wilson knew the Commission filed an action alleging manipulation of Issuer A securities. Wilson knew that although several of its customers signed a document saying they would not trade shares at other firms, those customers were liquidating shares at both Wilson and broker-dealer B. Wilson was concerned enough that the same attorney was writing attorney opinion letters to tell a customer he needed to find a different attorney. Finally, Wilson believed the conduct warranted closing numerous customer accounts. Despite all of these red flags, Wilson never filed a SAR on any suspicious trading in Issuer A securities.

pages 4-6

The Punishment

The punishment for all these failures to file SARs seems to me to be really weak: a $300,000 fine and a requirement to hire a consultant and follow the consultant’s recommendations on how to prevent these sorts of failures in the future.

Correction: 2019-7-23: I corrected the date of the settlement. This post originally stated the settlement as being dated 5/15/2018, not 5/15/2019.

Disclaimer: No position in any company mentioned. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

Marijuana stock Frelii (OTC: FRLI) has had a landing page promotion off and on for some months at TheNextBigThing.com (that landing page is currently promoting OTC stock Blue Eagle Lithium (BEAG): https://thenextbigthing.com/2018/11/20/artificial-intelligence-for-your-health-y/). (Check out this page to see all current landing page stock promotions.) On May 13th I became aware of another landing page with a purported big budget promoting the stock, when Tim Lento posted it on his blog. I then searched online for the language on that landing page (https://thehealthinvestor.com/) and found a second landing page at https://dnainvestoralerts.com/.

Below is a screenshot of the top of the first landing page:

The image below, taken from the same landing page promoting FRLI, is beyond absurd:

At least one person posted on

a message board that they have received a physical mailer

promotion on FRLI.

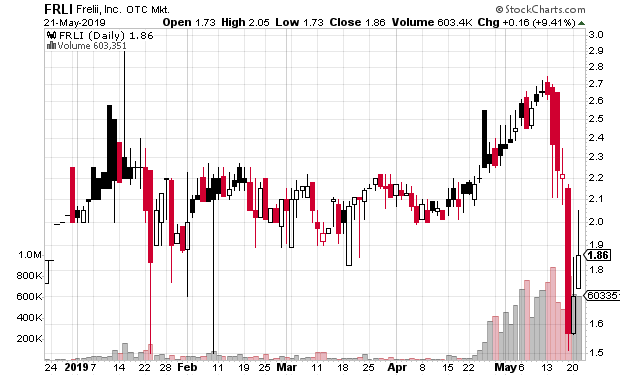

Due to how poorly pumps have done over the last couple years I started a short position in FRLI on May 7th. I planned to short more as I found more shares to short at Interactive Brokers but by the time I had found more shares to short on May 14th Interactive Brokers marked the stock as “No opening trades: Ineligible PINK stock”. IB has for over a year restricted trading of OTC stocks that are marked ‘Caveat Emptor‘ by OTCMarkets.com but this is the first time I have seen IB restrict a non-grey market OTC stock that isn’t marked Caveat Emptor. I contacted IB support to ask for an explanation and the following was the unhelpful reply:

After talking with several other traders I learned that IB had marked scores of other OTC stocks with that same trade restriction at the same time. They did not have one thing in common but it is likely that IB is looking at multiple risk flags that OTCMarkets.com is putting out (such as potential shell risk, stock promotion flag) and restricting stocks with multiple risks. CRSM and TOGL are two other such stocks restricted from trading by Interactive Brokers. OTCMarkets just recently introduced a tool for brokers and others to quantify risks of different stocks using numerous risk factors, called Canari. I think it likely that Interactive Brokers is now using that tool and restricting trading in stocks that score too high on a composite risk score.

FRLI landing page pump details:

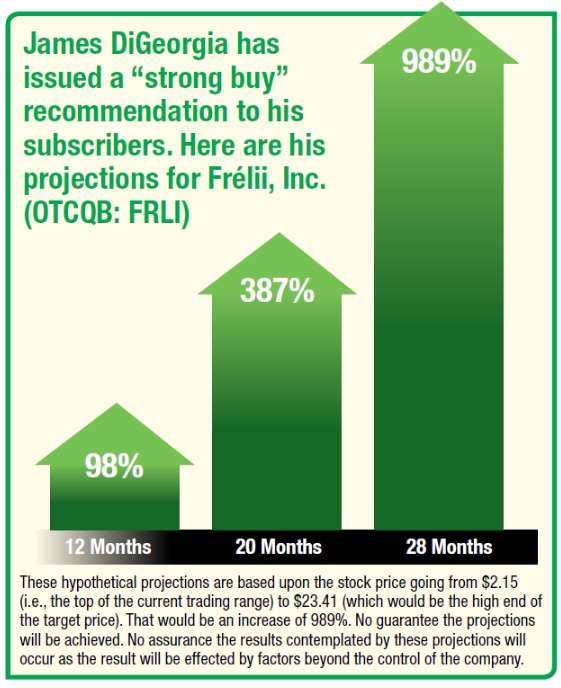

Disclosed budget: $2,183,616 Promoter: World Opportunity Investor / James DiGeorgia Paying party: TGB Media Limited Shares outstanding: 38,974,107 Free float: 9,538,629 Previous closing price: $1.86 Market capitalization: $72 million

In addition to the landing page promotion, FRLI was promoted via email starting on May 20th by the stock promoter group that I and others believe to be associated with AwesomePennyStocks / John Babikian and that I previously referred to as FinestPennyStocks. That group has stayed relatively under the radar until recently by constantly shifting websites. However, OTCMarkets.com appears to have targeted them, marking their last three large promotions, OOIL, BIIO, and KLMN, as Caveat Emptor and helping to end those promotions. The SEC even joined the act and suspended trading in OOIL (long after the pump was over). The disclaimer from the emails promoting FRLI is shown below:

Besides the stock promotion, Frelii also made news in Canada when its CEO (an American) attended a fundraising dinner for Prime Minister Justin Trudeau. The company then put out a misleading press release about that, which its outside PR person later walked back, saying in part “That was very probably inappropriate language at this point.”

Full disclaimer from online landing page:

All investments are subject to risk, which must be considered on an individual basis before making any investment decision. World Opportunity Investor is an investment newsletter being advertised herein. This paid advertisement includes a stock profile of Frélii Inc. (OTC: FRLI). This paid advertisement is intended solely for information and educational purposes and is not to be construed under any circumstances as an offer to buy or sell, or as a solicitation to buy or sell, any securities. In an effort to enhance public awareness of FRLI and its securities, TGB MEDIA LIMITED (Payor) provided advertising agencies with a total budget of approximately two million, one hundred eighty-three thousand, six hundred sixteen dollars to date to cover the costs associated with creating, printing and distribution of this advertisement for World Opportunity Investor. FRLI was chosen to be profiled in this advertisement after World Opportunity Investor conducted an investigation of the company. World Opportunity Investor was paid thirty thousand dollars as a research fee. In addition, World Opportunity Investor may receive subscription revenue in the future from new subscribers as a result of this advertisement. The advertising agencies will retain any excess sums after all expenses are paid. As of the date these materials are disseminated, neither the advertising agencies nor World Opportunity Investor nor any of their respective officers, principals or affiliates (as defined in the Securities Act of 1933, as amended, and Rule 501(b) promulgated thereunder) own or beneficially own any securities of FRLI. Neither the advertising agencies nor World Opportunity Investor or any of their respective officers, principals or affiliates will purchase or receive any securities of FRLI for a period of ninety (90) days following the date this advertising campaign is concluded. The Payor has represented in writing to World Opportunity Investor and the advertising agencies that neither the Payor nor any of its officers, directors, principals or affiliates (as defined in the Securities Act of 1933, as amended, and Rule 501(b) promulgated thereunder) owns or beneficially owns any securities of FRLI or will purchase or receive any securities of FRLI for a period of ninety (90) days following the conclusion of this advertising campaign. If successful, this advertisement will increase investor and market awareness, which may result in an increased number of shareholders owning and trading the securities of FRLI, increased trading volume, and possibly an increased share price of FRLI’s securities, which may be temporary. This advertisement, the advertising agencies and World Opportunity Investor do not purport to provide a complete analysis of this company’s financial position. They are not, and do not purport to be, broker-dealers or registered investment advisors. This advertisement is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor and only after reviewing the financial statements and other pertinent publicly-available information about the company and its industry. Further, readers are specifically urged to read and carefully consider the Risk Factors identified and discussed in FRLI’s SEC filings. Investing in micro cap securities such as FRLI is speculative and carries a high degree of risk. Past performance does not guarantee future results. This advertisement is based exclusively on information generally available to the public and does not contain any material, non-public information. The information on which it is based is believed to be reliable. Nevertheless, the advertising agencies and World Opportunity Investor cannot guarantee the accuracy or completeness of the information and are not responsible for any errors or omissions. This advertisement contains forward-looking statements, including statements regarding expected continual growth of FRLI. The advertising agencies and World Opportunity Investor note that statements contained herein that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect the company’s actual results of operations. Factors that could cause actual results to differ include the size and growth of the market for the company’s products and/or services, the company’s ability to fund its capital requirements in the near term and long term, pricing pressures, etc. World Opportunity Investor is the publisher’s trademark. All trademarks used in this advertisement other than World Opportunity Investor are the property of their respective trademark holders and no endorsement by such owners of the contents of this advertisement is made or implied. The advertising agencies and World Opportunity Investor are not affiliated, connected, or associated with, and are not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made to any rights in any third-party trademarks.

Disclaimer: I am short FRLI and may cover my position at any time. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

On October 5th, 2017 FINRA Enforcement filed a complaint (pdf) against Glendale Securities and its employees George Alberto Castillo (CRD No. 1936486), Paul Eric Flesche (CRD No. 3277904), Albert Raymond Laubenstein (CRD No. 303462), Jose Miguel Abadin (CRD No. 1273345), and Huanwei Huang (CRD No. 3268328). On April 5th, 2019 the FINRA Office of Hearing Officers released its Extended Hearing Panel Decision (pdf) regarding the allegations. The OHO decision is a 103-page beast that took me the better part of a day to read. See my highlighted and lightly-annotated copy (pdf). At the time I publish this there is no indication on FINRA’s website that the OHO decision has been appealed. I sent an email to Glendale Securities asking about that and they have not responded yet. I will update this article if they respond or if I learn that the decision is being appealed.

[Update 6/3/2019: Per my check of Glendale’s detailed BrokerCheck report today, FINRA Enforcement has appealed the OHO decision to the FINRA National Adjudicatory Council. Until the NAC has reached a decision the penalties against Glendale, Flesche, Laubenstein, and Huang will not go into effect.]

Currently, FINRA BrokerCheck shows that Castillo, Flesche, Abadin, and Huang remain registered with Glendale Securities. The BrokerCheck website indicates that Laubenstein left Glendale Securities after 12/31/2016 and has not worked at any registered broker since leaving Velox Securities on 2/10/2017.

Interestingly, this whole action “arose from a 2015 cycle examination of FINRA member firm Wilson-Davis & Co., Inc. (‘Wilson-Davis’), whose customers traded some of the same securities that Glendale’s customers traded and are the subject of this Complaint” (decision, page 2; all quotes in this article are from the hearing panel decision unless otherwise noted ). I have written previously about Wilson-Davis & Co., including an April 2017 SEC fine for Reg SHO violations and a February 2018 FINRA hearing panel decision (that has been appealed to the FINRA NAC). One important note: while Glendale Securities currently clears through Wilson-Davis, it did not do so during the period of time covered by the FINRA complaint and hearing panel decision.

Below is the overview of the complaint from the hearing panel decision:

FINRA’s Department of Enforcement filed a six-cause Complaint against Respondents. Cause one charges Glendale Securities, Inc. (“Glendale” or the “Firm”), acting through its President and head trader George Alberto Castillo (“Castillo”), with manipulating the price of NuGene International, Inc. (“NUGN”), to benefit two Firm customers who owned the stock. For this, Glendale and Castillo are charged with violating Section 10(b) of the Securities Exchange Act of 1934 (“Exchange Act”), Exchange Act Rule 10b-5 thereunder, and FINRA Rules 2020 and 2010.

Cause two charges Glendale, Paul Eric Flesche (“Flesche”), the Firm’s Chief Compliance Officer (“CCO”), andJose Miguel Abadin (“Abadin”), a registered representative and trader, with reselling unregistered or non-exempt shares of NUGN on behalf of two customers, in violation of Section 5 of the Securities Act of 1933 (“Securities Act”), which is a violation of FINRA Rule 2010. The Complaint alleges that a portion of the NUGN shares the two customers sold were bought from affiliates of the issuer and accordingly could not be re-sold within six months of acquiring them pursuant to the Securities Act and SEC Rule 144.

Cause three charges each of the Respondents with committing anti-money laundering (“AML”) violations of FINRA Rules 3310 and 2010 relating to customer deposits and liquidations of shares of NUGN and two other securities in 2015 and 2016: Broke Out, Inc. (“BRKO”) and Vitaxel Group Limited (“VXEL”). It charges Respondents with failing to establish a reasonable AML system to detect and report suspicious activities associated with Firm customers’ sales of NUGN, BRKO, and VXEL. Cause three also charges the Firm, Flesche, Laubenstein, and Huang with failing to comply with their obligations under the customer identification program (“CIP”) in connection with customers who deposited VXEL shares. Cause three further charges the Firm and Albert Raymond Laubenstein (“Laubenstein”), the Firm’s AML Compliance Officer (“AMLCO”), with AML violations for failing to establish and maintain an adequate due diligence program for customer correspondent accounts introduced to the Firm from 2007 to approximately 2011 by a bank based in Belize (“Belize Bank”). Belize Bank did not disclose the identities of approximately 18 customers who opened accounts at Glendale through the bank.

Cause four charges the Firm, Castillo, Flesche, and Laubenstein with supervisory failures in two distinct areas. It charges that Glendale, Castillo, and Flesche failed to establish and maintain a supervisory system, including written supervisory procedures (“WSPs”), reasonably designed to ensure the Firm’s compliance with Section 5 of the Securities Act for sales of unregistered, non-exempt securities. Cause four further charges the Firm, Flesche, and Laubenstein with failing to reasonably supervise Respondent Huanwei Huang’s (“Huang”) activities, specifically with respect to his Asian customers who deposited and sold BRKO and VXEL shares.

Causes five and six contain allegations only against Huang. Cause five charges Huang with improperly providing nonpublic personal information to third parties about his customers who deposited VXEL in their accounts, in violation of Securities and Exchange Commission (“SEC”) Regulation S-P, which constitutes a violation of FINRA Rule 2010. Cause six charges Huang with communicating about VXEL with a customer and another person in Asia via a cell phone text messaging service not approved by Glendale, in violation of FINRA Rules 4511 and 2010. The Complaint charges that Huang’s use of the unapproved text messaging service prevented Glendale from being able to preserve securities-related communications among its books and records.

Respondents filed Answers denying the allegations and requesting a hearing. In their Answer, Glendale, Castillo, Flesche, Laubenstein, and Abadin stated that Glendale “occupies a unique niche” in the securities industry because “[f]ew introducing brokers or clearing firms are willing to service the needs of early round investors and founders of microcap companies because of the intense regulatory scrutiny and labor-intensive processes that are required.” Glendale “believes that its experience in this type of trading has gotten the firm to the point where it can conduct this business without rule violations.”

pages 1-2

Below is the hearing panel’s decision / order in full:

As set forth above, the Hearing Panel dismisses causes one and two of the Complaint because Enforcement failed to meet its burden of proof. Enforcement failed to prove by a preponderance of the evidence that Glendale and Castillo violated Section 10(b) of the Securities Exchange Act of 1934, Rule 10b-5 thereunder, and FINRA Rules 2020 and 2010 by manipulating the price of NUGN.

A majority of the Panel also finds that Enforcement failed to prove by a preponderance of the evidence that Glendale, Flesche, and Abadin participated in the unlawful resale by customers RC and JH of NUGN shares, in violation of Section 5 of the Securities Act, which constitutes a violation of FINRA Rule 2010. These charges are therefore also dismissed.

As for the remaining causes of action in the Complaint, Respondents are sanctioned as follows:

Glendale Securities Inc.:

● Censured and fined $125,000 for the AML-related violations of FINRA Rules 3310 and 2010 associated with its customers’ deposit and liquidation of NUGN, BRKO, and VXEL (Cause Three).

● Censured and fined $30,000 jointly and severally with Paul Eric Flesche for failing to reasonably supervise Huanwei Huang, in violation of FINRA Rules 3110 and 2010 (Cause Four).

● This Decision shall serve as a Letter of Caution for the failure to conduct proper due diligence on Belize Bank and its customer accounts, in violation of FINRA Rules 3310 and 2010 (Cause Three).

Respondent Paul Eric Flesche:

● Suspended from associating with any FINRA member firm in any capacity for 30 business days and fined $30,000, jointly and severally with Glendale Securities, Inc., for failing to supervise Huanwei Huang, in violation of FINRA Rules 3110 and 2010 (Cause Four).

Respondent Albert Raymond Laubenstein:

● Suspended from associating with any FINRA member firm in any capacity for 18 months and fined $20,000 for AML-related violations of FINRA Rules 3310 and 2010 associated with the liquidations of NUGN, BRKO, and VXEL (Cause Three).

● Suspended from associating with any FINRA member firm in any capacity for 15 business days and fined $5,000 for failing to supervise Huang, in violation of FINRA Rules 3110 and 2010 (Cause Four). This suspension will run concurrently with the 18-month suspension imposed for misconduct alleged in cause three.

● This Decision shall serve as a Letter of Caution for the failure to conduct proper due diligence on Belize Bank and its customer accounts, in violation of FINRA Rules 3310 and 2010 (Cause Three).

Respondent Huanwei Huang:

● For sharing customers’ nonpublic personal information with third parties in violation of Regulation S-P, which is a violation of FINRA Rule 2010, this Decision shall serve as a Letter of Caution (Cause Five).

● Suspended from associating with any FINRA member firm in any capacity for ten business days and fined $5,000 for books and records violations of FINRA Rules 4511 and 2010 associated with engaging in securities-related communications with a customer and a third party via text instead of Firm email (Cause Six).

Respondents Glendale, Flesche, Laubenstein, and Huang are ordered to pay the costs of the hearing in the amount of $22,289.23, which includes a $750 administrative fee and the cost of the hearing transcript, $21,539.38. Their responsibility to pay these costs is apportioned as follows: Glendale is ordered to pay $12,289.23; Laubenstein is ordered to pay $5,500; Flesche is ordered to pay $2,500; and Huang is ordered to pay $2,000.

If this decision becomes FINRA’s final disciplinary action, the suspensions shall become effective with the opening of business on Monday, June 3, 2019. Respondent Laubenstein’s suspension of 15 business days for the misconduct alleged in cause four is to run concurrently with the 18-month suspension for the misconduct alleged in cause three. Respondent Huang’s suspension of ten business days shall end at the close of business on Friday, June 14, 2019. Respondent Flesche’s suspension of 30 business days shall end at the close of business on Monday, July 15, 2019.

(pages 97-99)

The names of two of the three companies mentioned in the complaint should be familiar to readers of this blog because I have written about them. I wrote about the mailer promotion of Nugene (NUGN) on May 27, 2015. I also wrote about Broke Out (BRKO) after the SEC suspended trading in it on March 17, 2016.

The Dissent

I have read every single FINRA Decision involving penny stocks that has been published over the last ten years (that I could find, searching the FINRA Disciplinary Actions database for “penny”). I have never seen a FINRA hearing officer dissent from findings of the extended hearing panel. This doesn’t mean that it hasn’t happened before but it is certainly noteworthy. Starting on page 100 of the decision, hearing officer Michael J. Dixon lays out a dissent from the panel’s decisions on causes two and four and furthermore describes increased fines that he wanted to levy. Bear in mind that each FINRA extended hearing panel consists of a hearing officer (who administers the proceeding) and “two industry panelists, drawn from a pool of current and former securities industry members of FINRA’s District and Regional Committees, current and former industry members of its Market Regulation Committee, former industry members of FINRA’s National Adjudicatory Council (NAC), and former FINRA Governors.” (That quote comes from FINRA’s OHO website.)

I encourage my readers to read the full dissent, but following are the excerpts I find most meaningful, first with regards to cause two from the complaint, which alleged, “Glendale, Flesche, and Abadin violated Section 5 of the Securities Act, which constitutes a violation of FINRA Rule 2010″ (emphasis mine):

The circumstances surrounding RC’s purchases of NUGN contained numerous red flags that should have triggered a true “searching inquiry,” as the SEC has instructed.

…

Additional factors were suspicious. The stock had traded just once as BLMK (in January 2015) and only recently (a week earlier, February 4) had begun trading as NUGN. RC opened its account solely for the purpose of liquidating its recently acquired NUGN shares. Also, relying on the transfer agent, as Respondents did, is insufficient to discharge a duty of reasonable inquiry.

…

JH’s deposit of another large tranche of NUGN shares on February 27 (which also was the day that RC started liquidating its shares), followed by SEI’s deposit on March 2 and JH’s second and much larger deposit on March 10, should also have raised red flags concerning RC’s deposit two weeks earlier. The three customers had purchased their BLMK shares nearly at the same time, and paid little for them. RC was able to generate enormous revenues from its sales as a result of NUGN’s dramatic price increase. Even assuming Respondent’s inquiry into RC’s deposit was reasonable at the time, JH’s and SEI’s deposits should have caused Respondents to reconsider whether RC’s deposit was part of a distribution of the issuer’s securities.

page 100

Next in the dissent is cause four from the complaint, which alleged that “Glendale, Castillo, and Flesche failed to establish and maintain a reasonable supervisory system.” Below are the most relevant excerpts (emphasis mine):

As Glendale, Castillo, and Flesche noted in their Answer, the Firm’s customers predominantly traded in low-priced securities, and accordingly they expect “virtually every one” of their customers to trigger at least one red flag. The Firm’s procedures do not reflect this view.

…

As implemented in practice, the Firm employed a “check-the-box” process for completing required forms and obtaining documents that it used to review a customer’s stock deposits. This process failed to identify for Firm personnel examples of red flags that could be indicative of an unlawful distribution of restricted securities.

page 101

My Take

I agree wholeheartedly with Hearing Officer Michael J. Dixon: in my opinion Glendale Securities’ procedures were inadequate and the numerous red flags particularly with the deposits and sales of NUGN should have called for a “searching inquiry”.

In my opinion the fine for Glendale is too small to provide a strong incentive for it to change its behavior and to motivate other brokers to do the same. Glendale was fined $125,000 individually, $30,000 jointly with Paul E. Flesche, and ordered to pay costs of $12,289.23. This is less than the firm earned from its commissions on one client’s (RC) sale of NUGN ($193,055; see decision page 27). I believe that at a minimum Glendale should have been forced to forfeit all the commissions it earned from the transactions discussed in the hearing (approximately $260,000; decision page 93).

Changing Clearing Firms

One interesting thing I learned in researching this article is that Glendale Securities has had a few different clearing firms over the past five years. According to the FINRA BrokerCheck detailed report, Glendale Securities currently clears through Wilson-Davis & Co. and it began that clearing relationship on January 29, 2018 (see page 11). By looking at the Archive.org archived version of Glendale Securities’ website, I found that on September 17, 2013 it cleared through Apex Clearing Corp. As of November 27, 2014 it cleared through Vision Financial Services. Vision Financial changed its policies in 2015 “to prohibit clearing deposits of physical certificates of penny stocks” and Glendale then switched clearing firms again (that quote is from Vision Financial Services recent settlement with the SEC for its failures to file SARs for penny stock share deposits and liquidations). As of August 14, 2015 Glendale cleared through Electronic Transaction Clearing (ETC).

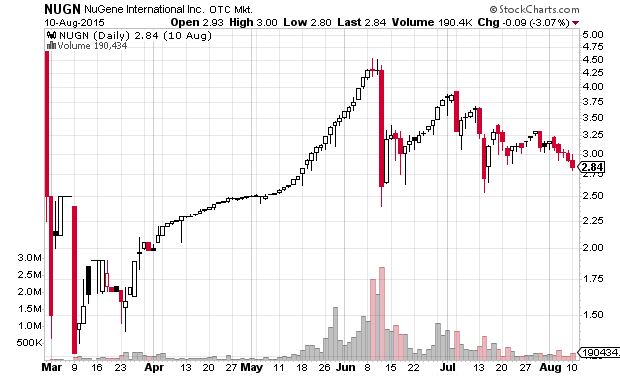

The Nugene Pump & Dump

For the reader interested in how people running pump and dumps acquire and then liquidate their shares, FINRA hearing panel decisions are a gold mine of knowledge. The Glendale Securities account holder that made the most money selling Nugene (NUGN) shares is referred to as “RC” in the decision. However, RC is easily de-anonymized because of how RC is described: “RC was incorporated in Nevada on January 29, 2015” (page 22). Later, on page 36, the decision states, “Beginning in March 2015, RC sponsored a promotional campaign that touted NUGN’s cosmetic products and urged investors to buy shares of the company.” Looking back at my blog post about the pump as it was happening, and then zooming in on the disclaimer, reveals RC to be Result Corporation. As shown by the Nevada Secretary of State website, one man — Robert J. Martins — is shown to have been the sole officer of the company. The corporation’s registration was revoked in 2016.

As I wrote on my blog post about the NUGN promotion, the budget listed in the mailer was $2,287,000. The hearing panel decision states, “A disclaimer at the end of the brochure disclosed that RC had paid $4.4 million ‘to marketing vendors to cover all the costs of creating and distributing this Advertisement'” (page 37). The different budget disclosures are not contradictory: promoters will sometimes update their disclaimers during the promotion as they increase their spending.

As for the shares Results Corporation would end up selling, they were purchased on the cheap: “According to the decision, Result Corporation paid $6009 for all its shares of BLMK that then turned into NUGN” (page 23). Result Corporation “bought the shares more than a month before its incorporation in Nevada” (page 23). The decision describes Result Corporation’s sales of NUGN in an odd way, stating that it sold NUGN shares for total proceeds of over $7.3 million, but that includes sales of shares it had bought in May and June 2015 for over $2.5 million. So the net proceeds from selling the shares is better described by the amount Result Corporation wired out of its account, $4,990,595 (page 27). Subtract the $4.4 million for the promotion and the $6009 for the shares and you end up with net profits of $584,586.

However, I believe this vastly understates the total profits from the pump for multiple reasons. First, “According to Enforcement’s investigator, customers at Wilson-Davis purchased most of the NUGN shares that RC sold. Wilson-Davis customers had also deposited shares of NUGN in their accounts” (page 27). Result Corporation had started selling shares of NUGN on February 27, 2015. I did not see anyone post about receiving the NUGN mailer prior to May 15, 2015. While I am certain people received it before that date, I think it likely that the actual promotion didn’t start until at least mid-April. That would mean that whomever was buying the shares from Result Corporation could have been associated with it, in which case their trading profits would have to be counted as well. Later in the decision the accounts at Wilson-Davis are mentioned again: “Enforcement argues that many persons played a part in the manipulation of NUGN—in particular, BS, ND, RC (which paid for a promotion campaign), and persons connected to the issuer, and Wilson-Davis, which made a market in NUGN and represented the buy side of NUGN transactions on February 24, 2015” (page 62). Also, one of the other sellers of NUGN shares mentioned in the hearing panel decision, “BS”, “later transferred his remaining NUGN shares to an account at Wilson-Davis” (page 62). Plus, there are the two other sellers of NUGN that held accounts at Glendale Securities — “JH” (whose NUGN sales proceeds were $812,989) and “SEI” (whose NUGN sales proceeds were $459,467).

So after adding up the profits of the three sellers of NUGN with accounts at Glendale Securities, it looks like about $1.8 million in profits. That is not bad, but there were millions of other free-trading shares outstanding at the time of the promotion held in accounts at other brokers (including Wilson-Davis as mentioned above). A writer on SeekingAlpha estimated that there were approximately 11 million free-trading shares at the time of the Nugene stock promotion. SEI deposited 216,410 shares, JH deposited 1,360,790 shares, and Result Corporation deposited 2,899,878 shares at Glendale Securities. That leaves 6,522,922 shares in the float that could have been controlled by others acting in concert and deposited at other brokers. Assuming an average sale price of $2.50 per share those shares could have resulted in an extra $16.3 million in profits for the people who owned them. That would be an impressive return on a $4.4 million investment in stock promotion.

NUGN daily chart starting 2/27/2015

Random Observation: If you can’t sell it, stock is worthless

One of the craziest things I read in the extended hearing panel decision was the following tidbit about a shareholder of Broke Out Inc (BRKO) (emphasis mine):

On March 17, 2016, three days after ECM’s last sale, the SEC announced the suspension of trading in BRKO until March 31, 2016, due to “concerns regarding the accuracy and adequacy of information in the marketplace and potentially manipulative transactions in BRKO’s common stock.” Huang informed ECM about the trading suspension. At the time of the trading halt, ECM had sold 472,782 BRKO shares and therefore still held 837,218 shares of the 1,310,000 shares he had deposited in his Glendale account. On the day of the trading suspension announcement, ECM emailed Huang asking if he would be able to resume liquidating his BRKO shares once the suspension ended or whether he needed to find another broker-dealer to sell the shares.

Huang and ECM did not communicate with each other for two months. On May 23, 2016, Huang emailed ECM, stating that Glendale had determined that ECM needed to close his account and that he could transfer his assets to another broker-dealer. Huang and Glendale never heard from ECM again. ECM effectively abandoned the BRKO shares left in the account.

page 47

Disclaimer: I have no positions in any stocks mentioned in this blog post. I have a brokerage account at Centerpoint Securities that is held at Vision Financial Services; otherwise, I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

On April 12, 2019 FINRA announced an AWC (Acceptance, Waiver, and Consent; they are essentially settlements with FINRA) with microcap broker and market-maker Wilson-Davis & Co. The firm agreed to a censure and a $32,500 fine. According to the AWC:

From January 2013 through August 2013, Wilson-Davis failed to establish, maintain, and enforce a supervisory system, including written supervisory procedures, reasonably designed to review email correspondence for indications of potential violations of federal securities laws or FINRA rules. In particular, Wilson-Davis lacked any pertinent written supervisory procedures, and its methods for reviewing email messages were ineffective and unreasonable given its business, size, structure, and customers. Through this conduct, Wilson-Davis violated NASD Conduct Rule 3010(a), (b), and (d), and FINRA Rule 2010.

FACTS AND VIOLATIVE CONDUCT

As part of an investigation of a former representative of Wilson-Davis that began in October 2014, FINRA obtained email messages that the former representative sent and received while he was still registered with the firm. FINRA’s review of these messages led it to conduct a follow-up review of Wilson-Davis’ supervisory system for email review.

NASD Rule 3010(a), which was in effect during the review period, required member firms to establish, maintain, and enforce a supervisory system, including written procedures, reasonably designed to achieve compliance with applicable federal securities laws and FINRA rules. NASD Rule 3010(b) provided general requirements for written supervisory procedures, or WSPs, and subsection (d)(2) required firms to develop WSPs specific to “the review of incoming and outgoing written (i.e., non-electronic) and electronic correspondence with the public relating to its investment banking or securities business.” These procedures must be “appropriate to [the firm’s] business, size, structure, and customers” and designed “to properly identify and handle customer complaints and to ensure that customer funds and securities are handled in accordance with firm procedures.” Subsection (d)(2) also required “surveillance and follow-up to ensure that [the firm’s] procedures are implemented and adhered to.”

A violation of NASD Rule 3010 also constitutes a violation of FINRA Rule 2010, which requires members and their associated persons to observe high standards of commercial honor and just and equitable principles of trade.

From January 2013 through August 2013 (the “Relevant Period”), Wilson-Davis’ WSPs did not include procedures describing how the firm would conduct its supervisory review of electronic communications sent or received by the firm’s registered individuals. Although the WSPs stated that “electronic communications are subject to review and retention,” the WSPs failed to describe the type or scope of review, how often the reviews would occur, and who at the firm was responsible for conducting the review.

While the firm lacked reasonably designed WSPs, Wilson-Davis conducted email reviews during the Relevant Period. The firm’s President and Chief Compliance Officer, JS, performed these reviews. In alternate weeks, JS reviewed either:

(a) 100 emails selected randomly by the firm’s email vendor, or

(b) messages flagged by the email system as containing a suspicious word or phrase from a lexicon of 24 search terms created by the firm.

The firm’s email reviews were not reasonable, however. The randomly selected messages did not constitute a reasonable amount of the firm’s overall electronic communications, and did not take into account the individuals, branch offices, departments, or business units generating the correspondence.’

The firm’s lexicon-based review was also not reasonable. The firm contacted its email provider to discuss appropriate lexicon search terms and selected 24 search terms that would ‘flag’ an email for a principal review. Collectively, these search terms were not comprehensive enough to yield a meaningful sample of flagged communications. Moreover, the lexicon was not based on an assessment of risk areas at the firm, nor was it reasonably tailored to the firm’s size, structure and business mode. As a result, most the search terms resulted in an unreasonably small number of emails flagged for review. Further, two search terms generated the vast majority of the flagged emails, and at least one of those terms was ineffective because it resulted in an unreasonably high percentage of “false positives.” Despite the obvious indications that the firm’s lexicon system was not reasonably designed, the firm did not evaluate the efficacy or make any changes to its lexicon system during the entire Relevant Period.

By virtue of the foregoing, Wilson-Davis violated NASD Rule 3010(a), (b), and (d), and FINRA Rule 2010.

I previously wrote about the FINRA OHO decision (pdf) against Wilson-Davis on February 27, 2018. That decision was appealed to the FINRA National Adjudicatory Council (NAC) on March 1st, 2018. When the NAC makes its decision it will be posted here. Back on April 28, 2017 I wrote about the SEC fining Wilson-Davis for Reg SHO violations.

Wilson-Davis has agreed to multiple AWCs over the past six years that I have not written about. They all included small fines. Below is a listing:

Disclaimer: I have no positions in any stocks mentioned in this blog post. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

On March 29, 2019 the SEC announced (pdf) an administrative proceeding in which it fined Vision Financial Markets LLC $625,000 for failures to file suspicious activity reports (SARs) regarding suspicious deposits and liquidations of penny stocks. These violations occurred from August 2013 to December 2014. Starting in 2012 Vision Financial began doing business with two introducing brokers that brought in significant penny stock business. These brokers are not named in the SEC order and are referred to as “Introducing Broker A” and “Introducing Broker B”. After a client of one of those brokers was indicted in July 2014 for a penny stock manipulation scheme Vision Financial reviewed its penny stock business and decided to cease doing business with both brokers. This decision also coincided with an SEC Office of Compliance Inspections and Examinations (SEC OCIE) inspection of Vision Financial’s penny stock business. By January 2015 Vision Financial was no longer clearing trades for those two introducing brokers. Vision Financial then updated its policies in 2015 “to prohibit clearing deposits of physical certificates of penny stocks.”

This matter concerns the failure by VFM, a registered broker-dealer, to file Suspicious Activity Reports (“SAR” or “SARs”) for voluminous suspicious activity relating to the deposit and sale of low-priced securities from at least August 2013 through December 2014 (the “Relevant Period”). In late 2012, VFM expanded its business of clearing equity securities by entering into clearing arrangements with several new introducing brokers. During the Relevant Period, VFM cleared millions of shares of transactions in low-priced securities on behalf of certain customers of certain of its new introducing brokers. These trades included instances in which newly introduced customer accounts exhibited a suspicious pattern in which the customer deposited a physical certificate for a substantial amount of a thinly-traded low-priced stock, systematically sold the shares into the market shortly thereafter, and then wired out the sale proceeds from its accounts. In some instances, the same customer engaged in this pattern with respect to multiple securities.

Despite clearing these suspicious transactions and other related red flags, VFM did not file timely SARs related to relevant activities by at least 100 of these accounts when it knew, suspected, or had reason to suspect that these transactions involved the use of VFM to facilitate fraudulent activity, or had no business or apparent lawful purpose.

Details on the suspicious activity of three customers (out of 101 accounts that deposited large blocks of penny stock shares and then quickly sold them and wired out the proceeds) are below:

Customer A

6. Between April 2014 and May 2014, Customer A engaged in three instances of suspicious deposit-sale-wire activity involving two different low-priced securities that generated sales proceeds of more than $1.1 million. Customer A deposited a physical certificate for 600,000 shares of a certain low-priced security (“Security A1”) and liquidated the entire amount on the same day that the deposit cleared with proceeds from the transaction wired out within three days. Customer A also deposited a physical certificate for 1,500,000 shares of a second-low priced security issuer (“Security A2”) and liquidated the entire amount by the day after the deposit cleared and wired out nearly all of the proceeds within a week of clearance. Customer A subsequently deposited a physical certificate for another 1,500,000 shares of Security A2 and systematically liquidated the entire amount within one week of the clearing date and again wired out nearly all of the proceeds within one week of liquidation. There was no other activity in this account during the Relevant Period. VFM did not file a SAR with respect any of the above-described activity in Customer A’s account.

Customer B

7. Between November 2013 and April 2014, Customer B engaged in several instances of suspicious deposit-sale-wire activity, including activity in at least two different low-priced securities that generated sale proceeds of approximately $1.8 million. Customer B deposited a physical certificate for 200,000 shares of a certain low-priced security (“Security B1”) and liquidated the entire amount within two days of clearance, with nearly all of the proceeds from the transaction wired out within a week of the liquidation. Customer B subsequently deposited a physical certificate for another 200,000 shares of Security B1 and liquidated the entire amount within three days of clearance, with proceeds wired out within a week of the liquidation. Customer B then made a third deposit of 200,000 shares of Security B1, began liquidating the shares, and wired out proceeds as blocks of sales occurred.

8. Customer B also deposited a physical certificate for 160,000 shares of a different low-priced security (“Security B2”), and later deposited a second physical certificate for an additional 80,000 shares of Security B2. Customer B proceeded to systematically liquidate the deposited shares and wired out proceeds of the sales as blocks of sales occurred.

9. In October 2014, shortly after VFM received a regulatory inquiry concerning the Customer B account, VFM informed the introducing broker of the Customer B account that the account had to be transferred “out of Vision ASAP” because of negative information concerning an individual associated with the account. The account subsequently sold previously-deposited penny stock positions of more than 650,000 shares and wired out proceeds exceeding $200,000 from VFM.

10. VFM did not file a SAR with respect any of the above-described activity in Customer B’s account. The Commission later brought charges against Customer B for violations of the antifraud provisions of the Securities Act of 1933 and the Exchange Act by engaging in market manipulation of Security B1 during the Relevant Period.

Customer C

11. Between January 2014 and October 2014, Customer C engaged in several instances of suspicious deposit-sale-wire activity, including activity in at least two different low-priced securities that generated sales proceeds of more than $490,000. Customer C deposited a physical certificate for 4 million shares of a certain low-priced security (“Security C1”), and began systematically liquidating the shares and wiring out proceeds as blocks of sales occurred. The entire deposit was liquidated in less than one month from clearance. Customer C then repeated this process with the deposit of another physical certificate for 2 million shares of Security C1, and systematically liquidated the entire deposit within approximately one month of clearance while wiring out proceeds as blocks of sales occurred. Customer C also deposited a physical certificate for 100,000 shares of a different low-priced security (“Security C2”), and immediately began systematically liquidating the shares, and wired out the proceeds the day after the liquidation was complete. Customer C then deposited another physical certificate for an additional 100,000 shares of Security C2, liquidated the entire deposit on the day that it cleared, and wired out proceeds shortly thereafter. VFM did not file a SAR with respect to any of the above-described activity in Customer C’s account.

Total proceeds from these deposits and sales of penny stock shares were over $50 million.

The order states that Vision Financial “failed to timely file SARs concerning any of at least 250 instances of the deposit-sale-wire pattern and failed to file any SAR at all pertaining to 88 of these accounts.” Given 250 SARs that were not filed and a total fine of $625,000, that works out to a fine of $2,500 per SAR that should have been but was not filed.

This action is but one of many recent actions in which the SEC has fined brokers for failing to file SARs or filing inadequate SARs regarding suspecious penny stock deposits and liquidations. In September 2018 the SEC settled with COR Clearing for failing to file SARs; COR was fined $800,000 and it agreed to almost completely stop accepting new shares of penny stocks for deposit. In July 2018 the SEC settled with ICBCFS and Chardan Capital, primarily for failures to file SARs regarding suspicious deposits and liquidations of penny stock shares. ICBCFS was fined $860,000 and Chardan was fined $1,000,000. A year ago in April 2018 the SEC fined Aegis Capital $750,000 for failures to file SARs regarding deposits and liquidations of shares of penny stocks.

Disclaimer: I have an account at Vision Financial (the introducing broker is Centerpoint Securities; Vision Financial has custody). I have no position in any stock mentioned above. I have no other relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

On March 8th, 2019 SEC Chairman Jay Clayton and SEC Director of Division of Trading and Markets Brett Redfearn gave a talk at Fordham University. A transcript of their talk was posted online. While they touched multiple topics, their comments about penny stocks may herald significant changes. I quote their remarks and give my take below.

First is Jay Clayton addressing Rule 15c2-11 (emphasis mine):

A particular focus of mine is Rule 15c2-11. This rule was designed to ensure that broker-dealers have sufficient information to understand and evaluate securities that trade off-exchange, or “OTC”, prior to publishing a quotation and also be in a position to provide this information to investors. At the Roundtable, however, panelists noted circumstances where the current operation of this rule may result in retail investors having little or no relevant information about a company.[16] I am concerned that these circumstances are an example of how uneven the information playing field can be for retail investors in this sector. I am particularly troubled by what I see — again said bluntly — as Rule 15c2-11 providing a significant exception to our disclosure rules for companies that (1) have not provided any recent information or (2) have conducted a reverse merger — e.g., a larger private company merging into a smaller or “shell” public company — and the post-merger company has no relevant public information available.

I have asked our Division of Trading and Markets staff to prepare promptly a recommendation to the Commission to update our rules to address these information issues, which experience tells us can be fertile ground for fraud and may be unnecessary to facilitate capital formation.

I also have a heightened level of concern for very low priced stocks known as penny stocks. These stocks, traded in the over-the-counter market, seem to have a special gravitational pull for fraudsters looking to take advantage of retail investors hoping for outsized returns. So I have also asked staff to review the sales practice requirements relating to penny stocks within Exchange Act Rule 15g-9 and the definition of “penny stock” within Exchange Act Rule 3a51-1. Again, I am sure that more can be done to help prevent fraud and manipulation in penny stocks.

The footnote [16] in the quote above is worth quoting in full as well:

See, e.g., Transcript of Roundtable on Regulatory Approaches to Combatting Retail Fraud (September 26, 2108), at 99 (Yvonne Huber, FINRA) (“I think under certain circumstances, piggyback eligibility should be taken away, such as in the reverse merger scenario, where there has been a completely different — a complete shift in the business line of a company, a complete change in ownership, a complete change in officers and directors. That’s essentially a new company and it probably doesn’t make sense in that space to allow piggybacking to continue.”), available at https://www.sec.gov/spotlight/equity-market-structure-roundtables/retail-fraud-round-roundtable-092618-transcript.pdf.

A “piggyback qualified” security is one that meets the frequency-of-quotation requirement described in SEC Rule 15c2-11(f)(3). The frequency-of-quotation test or “piggyback” exception is based on whether a broker/dealer has itself published quotations in the security in the applicable interdealer quotation system on at least 12 business days during the preceding 30 calendar days, with not more than four consecutive business days without quotations. Once this criteria has been satisfied, authorized participants may register on-line in a security. As long as the security remains piggyback qualified, any participant may quote the security without a Form 211 submission.

Basically, as long as one broker-dealer is posting quotations (making a market) in an OTC stock, all other brokers / market-makers can post quotes without having to file Form 211. The Form 211 is what is filed prior to the first broker making a market and requires a broker to essentially vouch for the company and the accuracy of its financials. Forcing companies to get a broker to vouch for them after doing a reverse merger would make it a lot harder for scammers running pump and dumps because they often will reverse-merge a private company into a public shell prior to a promotion. See Form 211 (pdf).

Below are SEC director Redfearn’s comments (emphasis mine):

First, following up on Rule 15c2-11, this Rule currently requires a broker-dealer, among other things, to review certain issuer information and have a reasonable basis for believing such information is accurate in all material respects and from a reliable source, before the broker-dealer initiates quotations for an OTC security.

The Rule, however, provides an exception from the information and review requirements for continuous quotations, known as the “piggyback exception.” Once a security becomes “piggyback eligible,” it can be quoted indefinitely in an interdealer quotation system without further review by any broker-dealer, provided there is not a break in quotations of more than four successive business days. As Chairman Clayton noted, panelists at the Roundtable identified circumstances where the current operation of the piggyback exception may result in retail investors having little or no relevant information about a company. I anticipate that the Division of Trading and Markets staff will present a recommendation to the Commission to update Rule 15c2-11 in the near future.

Below are Director Redfearn’s comments regarding transfer agents (footnote omitted; emphasis mine):

Finally, another potential gap in current protection for retail investors relates to transfer agents. Transfer agents who provide services to issuers of restricted and control securities generally are responsible for processing requests from selling shareholders to remove restrictive legends in connection with the intended resale of these securities by their owners. If a transfer agent improperly or inappropriately removes a legend, it could facilitate an illegal public distribution of securities that could harm investors.

This is a topic that was discussed in the Commission’s 2015 Advance Notice of Proposed Rulemaking and Concept Release on Transfer Agents, and was also the subject of a panel discussion at last year’s Roundtable. At the Roundtable, panelists discussed their current practices with respect to the removal of restrictive legends, and noted that there was an absence of specific Commission rules that govern those practices. They also identified and discussed some potential regulatory responses to fill that gap. I anticipate that the Division of Trading and Markets staff will present a recommendation to the Commission to update the transfer agent rules, including considering a rule that would specify transfer agent obligations with respect to the tracking and removal of restrictive legends.

The focus by both Clayton and Redfearn on rule 15c2-11 is not surprising to me. I have highlighted this rule and Form 211 in previous blog posts on SEC enforcement actions against Delaney Equity Group and Spartan Securities Group. I belief that the comments by Clayton and Redfearn herald two distinct potential changes in rule 15c2-11:

Companies that undergo a reverse merger will have to get a broker to file Form 211 to vouch for the accuracy of their financial statements

Companies that cease to provide current financial information will have to get a broker to file Form 211 to maintain quoting eligibility (otherwise they would get moved to the grey market)

Judging from Director Redfearn’s comments, it is likely that the SEC will also tighten the rules on transfer agents removing restrictive legends from shares. This will create another point of friction making it harder for insiders running pump and dump scams to get their shares cleared to sell.

Update 9-26-2019: Added Brett Redfearn’s name to the first paragraph

Disclaimer: I have no positions in any stocks mentioned in this blog post. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

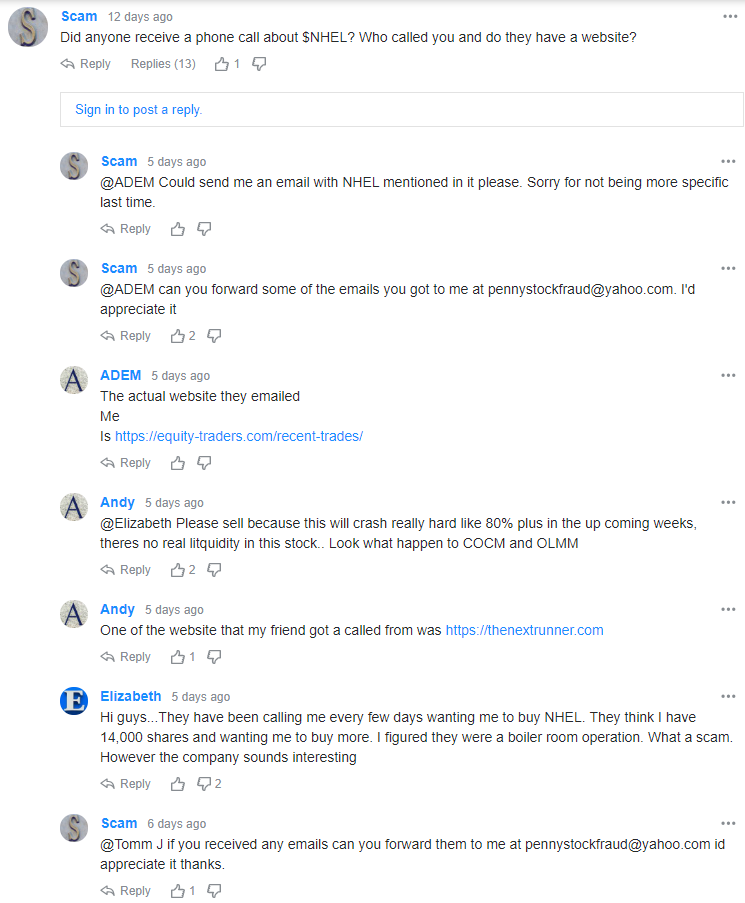

Disclosure: I am short NHEL. Even if I weren’t short, I would still advise against the stock. I am actively looking to increase my short position.

I have traded hundreds if not thousands of pump and dumps and blogged about many of them here over the last 12 years. While big email pumps and snail mail pumps are far rarer than they were 5 years ago, the pace of boiler-room pumps does not seem to me to have decreased. See my blog posts on recent boiler room pumps from October 2018, June 2018, and November 2017.

Today’s boiler-room stock promotion is Natural Health Farm Holdings (NHEL). I will only briefly touch on the fundamentals of the company, which are as usual absurd. Read the company’s SEC filings. The company has total assets valued at only $125,337 (per the most recent 10-Q). See NHEL’s company profile on OTCMarkets. A brief aside — I am sincerely impressed with the accumulation of small changes that OTCMarkets has made to their platform to bring transparency to the market. One nice feature is displaying share counts verified by the transfer agent — in the case of NHEL it is 161,859,500 shares as of 2/25/2019. With the stock at $1.25 as I write this, that gives the company a whopping $200 million market capitalization. Also, the company reports in its OTCQB certification (pdf) filed on 1/2/2019 that there are 30 million shares in the public float (some or all of these shares are being sold in the pump and dump). Another useful bit of info provided by OTCMarkets now is the shell risk disclosure displayed for NHEL. According to OTCMarkets:

The Shell Risk designation indicates that a company displays characteristics common to Shell Companies. This designation is made at OTC Markets’ sole and absolute discretion based on an analysis of the company’s annual financial data and may differ from issuers’ self-reported shell classifications in their own public filings.

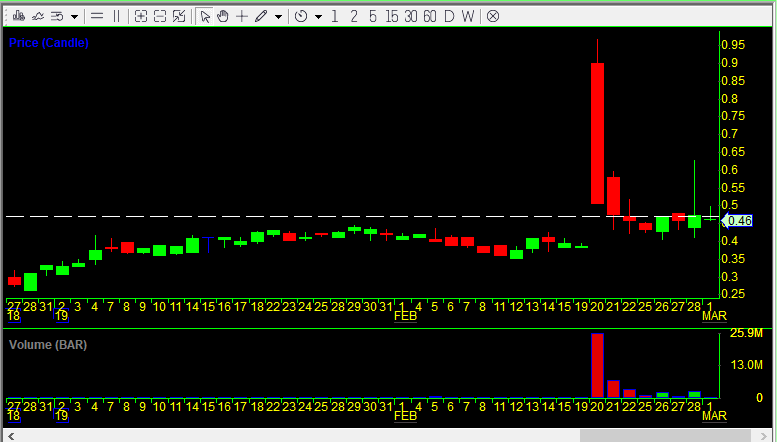

One benefit for the stock promoters / insiders in a boiler-room pump and dump is that information about the pump is not easily available: there is no paper trail of promotions. A side effect of this is that OTCMarkets seems to me to be slower to mark a stock promoted by a boiler-room as undergoing stock promotion (NHEL currently lacks that flag) or ‘caveat emptor’ (NHEL also lacks that flag). That being said, once OTCMarkets becomes aware of a boiler-room pump I believe they are more likely to give it the ‘caveat emptor’ tag than they would be to give a stock undergoing email promotion a ‘caveat emptor’ tag. In the past, boiler-room pumps have dumped right after receiving the caveat emptor tag. For example, OLMM was given the ‘caveat emptor’ tag on march 8, 2018 and the next day it gapped down from $1.34 to $1.19 and ended that day at about $0.4103. Comerton Corp (COCM) received the ‘caveat emptor’ designation from OTCMarkets on June 5th, 2018. The next day it gapped down from $0.97 to $0.91 and closed at $0.83. Two days later it closed at $0.31.

With an average daily volume of over 300,000 shares over the month NHEL has already done better than most boiler-room pumps.

Reports of the boiler-room pump of NHEL can be found on Twitter and on stock message boards such as Yahoo and InvestorsHub. See screenshots below:

Comments on NHEL on Yahoo FinanceMore comments on NHEL on Yahoo FinanceComment on NHEL message board on InvestorHub

Besides the ongoing boiler-room pump & dump, NHEL has more fun awaiting investors: a toxic financing deal with GHS Investment LLC (see S-1 registration statement for details). GHS will get shares for a nice 20% discount to the “lowest traded price of the Company Common Stock during the ten (10) consecutive trading days prior to the date the Drawdown Notice was submitted” (quote from S-1). Of course by the time the company can start to make use of this financing arrangement the stock will likely be 90% below where it currently trades.

Disclaimer: I am short Natural Health Farm Holdings (NHEL) and am trying to borrow more shares to short. I may trade around this position (cover and reshort) at any time and will not update this blog post as I do so. I have no positions in other stocks mentioned in this blog post. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

I use Tradelog to track my trades for accounting and tax purposes. I have used it for probably a decade now and for the most part I have been very happy with it. However, when looking at my trades for last year I found some discrepancies in one of my accounts between the Tradelog data (which can be directly imported from the trade data statements generated by almost all brokers) and the broker’s 1099-B. But unlike most errors, which are rare and large (for example, a broker reporting the same trade twice or accounting for a share exchange in a weird way), I noticed lots of little errors — many trades were off by just a dollar or two. In the grand scheme of things the differences didn’t make a big difference (about $50 total), but I still wanted to fix the errors and understand why they were happening.

I looked at the CSV spreadsheet that I had downloaded from my broker’s website with all the 2018 trades; I had imported my trades to Tradelog directly from this CSV file. The stock prices on all the trades matched so I then looked at the commissions in the CSV file and Tradelog. There I found that on some of my trades, high ECN rebates had been larger than my commissions, leading to a negative commission on the trades. Every single trade with a negative commission was imported into Tradelog as having a positive commission with the same absolute value. So if the commission was ($1.25) then it became $1.25 in Tradelog.

Naturally I thought that there must have been some small error in the import filter from that specific broker. Instead, I was told the following:

TradeLog is limited when it comes to ECN Rebates because the commission has to be negative. If TradeLog were to import the commissions as negative whenever the broker reports them as negative, the resulting data import would be wrong for the vast majority of our users that do not receive rebates. In fact, TradeLog has a special warning to alert the user when inadvertently entering the commission as a negative number as this is in most cases incorrect. This special situation requires that the user make the appropriate adjustments manually:

If you have any further questions, please let us know.

This boggles my mind. I had to go back through my data file and edit around 50 different trades to correct the data (at least Tradelog does allow negative commissions although it complains each time you enter one).

I should mention that this problem is not going to affect most traders — you have to trade a lot to get a low enough commission rate that your ECN rebates can be larger than your commissions. But for those of us who do trade that much even small errors can take a lot of time to find and fix.

To fix this Tradelog should allow users the ability to allow the program to import trades with negative commissions (this could be done via a checkbox while keeping the same default behavior). Frequent traders such as myself have enough trouble with brokers often giving incorrect 1099s — we should not have to deal with accounting software that doesn’t import negative numbers.

Disclaimer: I have no position in any stock mentioned above. I have used Tradelog for about a decade and other than the above problem I am a satisfied customer. I have no other relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

On March 5th, 2019 FINRA accepted an offer of settlement from TriPoint Global Equities LLC, Michael Boswell (TriPoint’s President and Chief Compliance Officer), and Andrew Kramer (TriPoint’s Head Trader). The summary from the settlement order is as follows:

1. During the period November 2011 through December 2015 (the “Relevant Period”), TriPoint Global Equities, LLC (“TriPoint” or the “Firm”) engaged in the penny stock business, effecting transactions for customers whose primary trading activity involved the deposit and prompt liquidation of low-priced securities (also known as “penny stocks” or “microcap stocks”). Nonetheless, throughout the Relevant Period, TriPoint, through AntiMoney Laundering (“AML”) Compliance Officer (“AMLCO”) and Chief Compliance Officer (“CCO”) Michael Boswell (“Boswell”), and Head of Trading (“Head Trader”) Andrew Kramer (“Kramer”), failed to establish and implement AML policies and procedures reasonably 3 designed to detect and report suspicious activity, including AML red flags, in connection with the Firm’s penny stock business.

2. Further, during the Relevant Period, Respondents TriPoint, Boswell, and Kramer failed to reasonably identify and address red flags of potentially suspicious activities presented by Customer EM’s deposits and liquidations of penny stocks. By virtue of this conduct, Respondents TriPoint, Boswell and Kramer violated FINRA Rules 3310(a) and 2010.

3. In addition, during the Relevant Period, TriPoint failed to comply with the registration requirements of Section 5 of the Securities Act of 1933 (the “Securities Act”) by engaging in the unlawful re-sales of approximately 16,907,900 shares of restricted securities of two penny stock issuers into the public market on behalf of Customer EM, in violation of FINRA Rule 2010.

4. Further, TriPoint failed to establish and maintain a supervisory system, including written supervisory procedures (“WSPs”), reasonably designed to achieve compliance with the registration requirements of Section 5 of the Securities Act of 1933 (the “Securities Act”) for the re-sales of restricted securities, in violation of NASD Rule 3010(a) and FINRA Rule 2010 for conduct prior to December 1, 2014 and in violation of FINRA Rule 3110(a) and FINRA Rule 2010 for conduct on or after December 1, 2014.

Essentially all the firm’s failures identified in the settlement relate to trading by one customer, “EM”, who deposited and sold shares acquired through “‘toxic’ or ‘death spiral'” convertible notes. From the settlement:

C. Red Flags Involving Customer EM’s Deposits and Liquidation of Low-Priced Securities

32. In or about March 2015, Customer EM opened an account with TriPoint. 33. At all times, TriPoint, Boswell, and Kramer were aware that Customer EM’s business was the liquidation of low-priced securities obtained through convertible note investments. By contrast to a traditional convertible debt arrangement, in which the conversion formula is fixed, the conversion ratio for Customer EM’s transactions was based on fluctuating market prices to determine the number of shares of common stock to be issued. This market price-based conversion formula protected Customer EM against price declines. However, a market pricebased conversion formula can lead to dramatic stock price reductions and corresponding negative effects on both the issuer and its shareholders. Accordingly, as the SEC has explained, these types of convertible debt financing arrangements have colloquially been referred to as “toxic” or “death spiral” convertibles.

34. Eight of the issuers whose stock was deposited and liquidated by Customer EM through TriPoint presented red flags signaling potentially suspicious activity for penny stock companies. These red flags included several that the Firm’s AML Plan (and FIN RA’s Small 11 Firm Template) identified, such as limited or no revenues, large net losses and accumulated deficits, and material changes in business lines, names, and structures. In addition, although each of the issuers was an SEC reporting company, several failed to make the appropriate SEC disclosures or were delinquent in their regulatory filings. As discussed further herein, one company’s CEO had been the subject of a California State Court Desist and Refrain order relating to re-sales of another penny stock issuer of which he was an owner. Several of the issuers also released numerous press releases around the time of Customer EM’s deposits and liquidations. Publicly available information, including the issuers’ own SEC filings and a website that published newsletters and maintained message boards focused on microcap stocks, pointed to risks surrounding several of the issuers’ securities. Customer EM’s liquidations of the penny stocks amounted to a significant percentage of the TMV of these securities. At times, Customer EM’s liquidations represented over 90° o of the TMV. This information was readily available in public filings made by the issuers to the SEC and on the interne.

Per the company’s Brokercheck report, it currently clears through FolioFN Investments Inc. The settlement does not mention TriPoint having changed clearing firms so I think it likely that it cleared through FolioFN Investments at the time of the events covered by the settlement (November 2011 through December 2015, the “Relevant Period”).

The settlement calls for a 30-day suspension and $10,000 fine for Boswell and a 30-day suspension and $10,000 fine for Kramer. TriPoint Global Securities agreed to a censure, a fine of $100,000, the disgorgement of $34,001 in commissions, and a 12-month ban from receiving penny stocks for deposit except if the stock comes from an offering “in which TriPoint acted as a selling agent.”

Disclaimer: I have no position in any stock mentioned above. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

It has been awhile since my last trading strategy post so I thought I would write one about something that I have been paying attention to recently. If you don’t know my core beliefs on trading strategy, read these classic blog posts first:

A good chunk of the money I make comes from day-trading. The most important thing when considering a day-trade is that fundamentals almost don’t matter — what matters is supply and demand for the stock. If you can identify situations where demand will drop throughout the day or supply will increase, or both, you will be able to profit from short-selling. Conversely, if you can identify decreasing supply or increasing demand, you can profit from buying.

Perhaps one of the most predictable sources of increased supply of stock is the company issuing shares through an already-existing ‘at-the-market’ offering, commonly known as an ATM. Now it is one thing to identify a situation where a company has an outstanding ATM facility and the company needs cash (as can be known by looking at the balance sheet and cash flow statement). That is certainly useful and many traders do that. But wouldn’t it be even better to spend the time to follow such situations prospectively and then identify how often and how much those ATMs were actually used?

This is what I am spending time and effort on right now: whenever I see a stock gapping up on news that I might want to short because the news isn’t really that great, I look for outstanding ATMs. Regardless of whether I trade the stock or not, I make a note to look back at the SEC filings in the future to see if the company actually did sell shares through the ATM on that and following days. By doing this I will get a better sense of how reliably companies will use their ATMs in these situations and this will help me better evaluate the risks of shorting these stocks.

The first stock I made a note to look back at was Arca Biopharma (ABIO). This makes for a perfect example because the company put out a 10-K soon after having a big spike on February 20, 2019, and the stock had very low volume prior to that spike. So let’s take a look. Below is the daily candlestick chart of ABIO for the year up until today.

Having identified the stock as worthy of interest and having an ATM on February 20th, we can now look at the filings to see if it used that ATM. On February 27nd, the company filed its 10-K for the year ended December 31st. On the first page we find this: “As of February 22, 2019, the Registrant had 18,355,111 shares of common stock outstanding.” The balance sheet lists 13,924,058 shares outstanding as of December 31st, 2018. So from January 1st to February 22nd, 201 ABIO issued 4.43 million shares, increasing the share count by 31.8%. Next we go to the section entitled “(7) Equity Financings and Warrants” — I knew to go there because I searched the document for “at the market” (if that doesn’t work search “at-the-market”. Unfortunately, that just describes the ATM usage for 2017 and 2018 — I want more recent issuance so I go to the “subsequent event(s)” section.