Many people have argued that the current high house price to income ratio is not reason for house prices to decline, considering that interest rates are very low now. These people argue that what is important is not the actual price of the house, but the mortgage payment required to carry the house (for an example see user jcrash’s comments on my previous aritcles on the coming mortgage crisis at SeekingAlpha).

To some extent, these arguments are correct. Most home buyers use mortgages, and the difference in monthly payments between a 5.5% and a 8% mortgage is staggering. However, there are two important reasons why low interest rates do not mean that houses are affordable now: household debt is at an all-time high and mortgage rates will certainly go higher.

Total Debt Matters

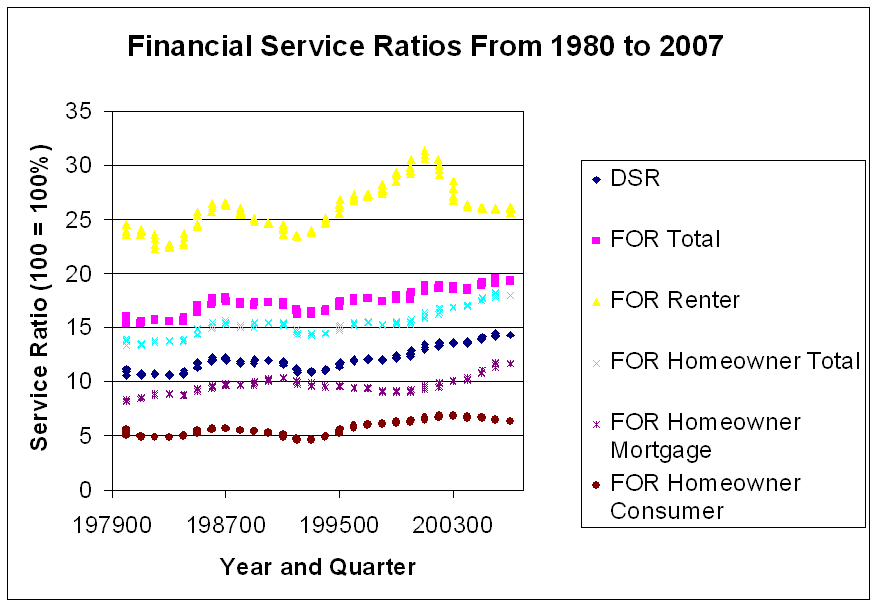

Housing affordability is not independent of the affordability of other consumer goods. What matters for the affordability of housing and all consumer goods is the money available to pay for those goods (ie, money not spent on necessities). Total household debt is at an all-time high. The savings rate is close to zero. The most instructive number to look at is the household financial obligation ratio, or the ratio of income to household debt servicing and house or apartment-related expenses. To quote the Federal Reserve definition, “Debt payments consist of the estimated required payments on outstanding mortgage and consumer debt. The financial obligations ratio (FOR) adds automobile lease payments, rental payments on tenant-occupied property, homeowners’ insurance, and property tax payments to the debt service ratio.”

Keep in mind that these ratios do not include other non-discretionary expenses such as food and gasoline, the price of both of which has been increasing at staggering rates, which means that consumers have less ability to service their debt than even the following graph shows (click for a full-sized image). The data are available from the Federal Reserve. The key number to look at is the FOR Homeowner Total (light blue). Over the last decade this has increased from about 15% of income to about 19% of income.

These are the costs on debt and home-related expenses that current homeowners pay. Because these are broad averages (many homeowners do not have mortgages after paying them off, reducing these ratios), it is important to look at the change over time. The ratio is currently about 4 percentage points higher than anytime prior to 2000. While this may not seem like much, consider that house prices are set on the margin and that approximately 40% of homeowners do not have mortgages. The marginal home buyer has much larger debt payments of all kinds than ever before, reducing his ability to buy. This alone indicates that home prices need to fall. However, the picture gets even bleaker when we look at mortgage rates.

These are the costs on debt and home-related expenses that current homeowners pay. Because these are broad averages (many homeowners do not have mortgages after paying them off, reducing these ratios), it is important to look at the change over time. The ratio is currently about 4 percentage points higher than anytime prior to 2000. While this may not seem like much, consider that house prices are set on the margin and that approximately 40% of homeowners do not have mortgages. The marginal home buyer has much larger debt payments of all kinds than ever before, reducing his ability to buy. This alone indicates that home prices need to fall. However, the picture gets even bleaker when we look at mortgage rates.

Inflation Matters

Those that argue that house prices are affordable would agree that lower interest rates make houses more affordable, ceteris parabus. This is true not just for houses but for all capital assets. As interest rates increase, asset prices decrease. As interest rates fall, asset prices rise. If a buyer finances a high-priced asset with cheap financing and does not sell when financing becomes expensive, that buyer will do fine. However, a buyer who cannot hold indefinitely must pay attention to asset prices. Even when payments are equal, it is better to buy a cheap asset with expensive financing than to buy an expensive asset with cheap financing. The reason is simple: interest rates change. Interest rates are more likely to fall when they are high than when they are low. If they do fall, the seller who had bought when interest rates were high will have a capital gain as the price of the asset increases. However, the seller who buys when interest rates are low will take a capital loss if he sells after rates rise.

Inflation in the US is at a 4% annual rate as of March, and investors expect inflation to continue or get worse, as evidenced by the low yields on TIPS (Treasury Inflation Protected Securities). With 15- and 30-year fixed rate prime mortgages near their lowest rates since before the 1960s/1970s inflation epidemic, there is little place for mortgage rates to go but up. Even if housing were fairly affordable now (which the FOR ratios above show that it is not), higher interest rates will ensure that it becomes less affordable and that house prices need to continue to drop.

See Also

Option ARMageddon take on this issue

The Coming Mortgage Crisis: Part 1

The Coming Mortgage Crisis: Part 2

Disclosure: I have significant real estate holdings and I plan on selling short one or more regional banks.

hi mike-

i found out about you through portfolio123. all went to heck for awhile and i let go of my subscription. these days the site has a bunch of errors, but the site was effective in a bull market.

wondering what your opinion is of p123 and if you’re still a member?

i still somehow think that p123 might actually work even though the small cap value quant approach went bust in the bear market. thanks in advance.

and, of course, awesome blog and writing style also.

bk

Howdy! For tax reasons I have switched my taxable accounts to ETFs. Most of my effort is focused on short selling now. I do still run my IRA using ports on P123. You can see my performance here: http://icarra.com/viewPortfolio.php?id=1925

I have continued to do fairly well, so I am happy. Of course, last July/August was scary when everything stopped working for awhile, but I am pretty confident that my ports will do fine in the long run.

I also use P123 to screen for many of my short ideas.

Oh, and I still believe that small value will outperform in the long run, even if there will be stretches where it does poorly.

Mike-

Nice write-ups. One other factor nobody seems to address when speaking to “affordability” are RE taxes. In order to pay for the ever increasing expenditures in our town RE taxes have gone up every year for what I can remember (not too long, but long enough). While I don’t live in the town, I know people in Naperville, IL who pay five figures in taxes for a 450-500k home. To me that’s astounding and a big part of why my wife and I choose not to buy there…

Scott, RE taxes are actually included in the FOR. It is not going to look pretty over the next few years as towns that were accustomed to free money from rising valuations have to make due with much less. Vallejo is a perfect example of this.

hi mike-

thanks for the perspectives. do you think it’s worth checking the p123 models’ output against other indicators? i was thinking a motley fool caps rating of 1 or 2 might increase the odds or maybe some technical indicator. in the past, i just blindly went with the picks.

BK – that is possible. I do like CAPS as a way to get ideas. However, when I do quant I stick with the quant model. I don’t second guess it because I can’t backtest the performance of my second guesses. When I do short selling, it is all discretionary, and I do not pull the trigger unless I am convinced by reading the financials that I am right.

that makes sense. the one thing you really need to have with small caps and short selling is guts. i need to develop the mentality to hold through the drawdown with small caps. with shorts, i don’t think i can get myself to put on a greater than 2k position and only a few here and there. there should be a book on how to mentally withstand short squeezes. clearly, you have an aptitude for reading the financials and it really seems to serve you well as the squeezes occur. kudos and keep rocking.

Thanks. I’m actually planning on writing a book. Only problem is that I need to make a whole bunch more money and get a bit more famous before I could ever hope to sell the book.

mike-

what are your thoughts on glre – holding company run by david einhorn, the value investor/poker champion? looks like it might be a decent entry here.

You’re basically buying into his hedge fund. His management firm charges hedge fund like prices to manage the investment portfolio — 1.5% of assets and 20% of profits, with a 150% clawback provision on losses (no money paid if there is a loss and not until the loss has been more than erased).

For a fan of Einhorn it isn’t a bad entry at only 10% above book.

Actually, it looks more like 15% above book.

hi mike-

thanks for the perspective. ah. yeah. i might hold off now. the blog, world beta, has some interesting stuff on einhorn. i might have to read his book when i get a chance.

i’m on the fence as to whether it’s worthwhile to read the niederhoffer book, education of a speculator. the book, moneyball, strangely enough, has had the most positive effective on my investing/trading, so maybe i’ll read that again. are there any books you recommend?

I’ve heard good things about his book as well. I do really like Einhorn and I would seriously consider buying GLRE at book value. As for books, some on my to read list are O’Glove’s books Quality of Earnings. I am currently reading Plight of the Fortune Tellers. Somewhere I have a list of my thoughts on the books I’ve read and when I get around to it I’ll post my list of recommended investment books.

not sure if you’re into this sort of thing, but one place to find ideas that have been profitable for me are the buys of john burbank of passport capital (219% last year) and phil falcone of harbinger capital. zinc, for example, was quite cheap on a recent pullback and then just exploded today. some of their picks are extended though. easiest places to find their holdings are tickerspy. harbinger’s picks are generally at the top of finviz insider transactions.