While doing well with real money is always nice, it is fun to play with fake money too. I am currently ranked in the 40 players out of more than 33,000 on Motley Fool Caps. There are only two other players who started after me who are ranked higher. Not bad, eh?

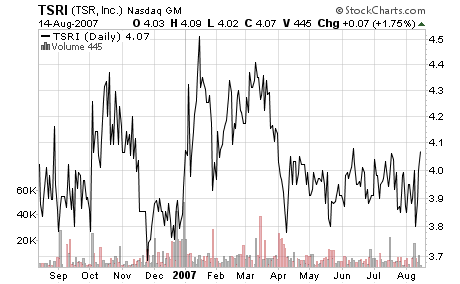

Of risk and microcaps: TSR, Inc. (TSRI)

There are those that say that microcaps are inherently risky. They are wrong. There are those that say that stocks with low prices (ie, below $5) are inherently risky. They are wrong. There are those that say that OTC BB, pink sheets, or unlisted stocks are inherently risky. They are wrong. (Although, to be fair, most unlisted stocks are not good investments; but that does not mean that being unlisted makes a stock a bad investment.)

For example, I am aware of a couple private companies based near my hometown that I would love to own (if the price were fair), even though they are private (for the record, both are closely held by only a couple people; one of them is Chemtool). As long as I don’t overpay, it doesn’t matter to me if the company is small, the stock is hard to sell, or the financials are not filed with the SEC. As long as I can get my hands on the financial statements and I can trust them, I have no problem owning tiny or illiquid companies. Neither should you.

Perhaps my favorite tiny company that you can buy is TSR, Inc. [[TSRI]], currently trading at just over $4.00. The company sports a book value of $3.05 per share, and most of that is in the form of cash, short-term treasury bills, and short-term receivables. I estimate that the company has a liquidation value of $13 million (compared to a $18.6 million market cap), meaning that in a worst-case scenario we would not expect to lose more than 31% of our investment. The company, currently going through tough times, remains profitable (even excluding interest on its investments). If the company were to utilize its excess cash to fund a special dividend or to buy back stock, while its operations improved modestly to historic norms, the stock could easily increase 50% or more in value. In the meantime, the stock’s nice 8% dividend yield is nice (although keep in mind that the payout yield is over 100%, so some of that dividend currently represents return of capital).

TSR Inc. is a staffing company in New York for computer programmers and related professionals. A large chunk of the company is still owned by its founder, who has also recently bought stock on the open market at around $4 per share. I should note that the founder, Joseph Hughes, has previously been successful when trading TSR’s stock–he sold a large number of shares back in 2004 when TSR’s stock was much higher.

Disclosure: I own TSRI. If you follow my portfolios, you will notice that I sold off a large percentage of the shares I owned a couple weeks ago. This was for strategic reasons (allocating money to a better opportunity). I continue to own what for me is a normal-sized stake in TSRI. See my disclosure policy.

A self-congratulatory post

You should now address me as Master Michael. I successfully defended my master’s thesis this morning, “Memory Systems and Memory Consolidation During Sleep”. I will now be leaving my ‘day job’ of psychology research and I hope to find work in the wonderful world of finance.

This should give me some more time to write, now that I am not frantically working 60 hours a week on my thesis.

Is college worth it? An analysis

After reading a recent very bad blog post (here), saying that college was not worth it because of high upfront costs, I thought I would take the same data and analyze it the right way.

The average (median) college grad earns about $51,110 per year, while the average (median) high school graduate earns $29,337 per year. The average annual cost of a private university is $30,367 per year. I figure that college takes 5 years and the HS graduate will thus work five more years. So there will be 40 total years of work for the college graduate and 45 for the high school graduate. Using 7% as my interest rate, I calculate the net present value (at the end of high school) of the high school graduate’s earnings to be $399,145.19. For the college graduate I figure a net present value of future earnings of $681,384 at the end of college. Discounting that plus the payments for college back to the end of high school five years earlier gives us a net present value of ($485,817 – $124,511 = $361,306). So college appears to lose. Let’s make this a little more realistic and see what happens, though.

To be more realistic we give the HS graduate an annual 2% raise starting when he starts his job. We give the college graduate an annual 3% raise beginning at the same time (because the value of a college education will be increasing each year he is in college). We increase the cost of college by 5% a year. Discounting all future college costs and earnings at 7%, we find the net present value of the college graduate’s earnings to be $651,485, whereas the net present value of the high school graduate’s earnings are $504,266. So even taking a long time to finish college (5 years), not working at the time, and going to an expensive private school with no scholarships, the college graduate makes out like a bandit relative to the high school graduate.

The benefits to college are real and large. Because non-skilled jobs will probably continue to disappear, my estimation of 2% annual raises for the HS graduate are probably way overoptimistic and the benefit to a college education is even larger than my estimate.

Of babies and bathwater: International Shipholding (ISH)

Turmoil in the markets continues. Today getting slaughtered (down below $16) was International Shipholding Corporation [[ISH]]. The company reported no news and yet the stock dropped 20%. It is now trading at 2/3 book value. One nice thing about the shipping companies–they are generally worth around book value. So if you find one that is selling at a significant discount to that and there is nothing highly wrong with the company, it could very well be a good investment. One thing to note is that most shipping companies are not the best in terms of corporate governance.

Disclosure: I own ISH. My disclosure policy will never sink.

Suggested Reading

Courtesy of James Montier. Download the pdf.

John Burr Williams’ Theory of Investment Value is a tough read but it is one of the best out there for laying out the philosophy of how to value companies.

The Value of Sloth

Are you worried that you aren’t doing enough to increase your investment performance? Perhaps all you need to do is go on a 2.5 year vacation. According to Mark Hulbert, the best performing investment newsletter over the last 5 years has not been published in the last 2.5 years. So by doing absolutely nothing it has garnered great profits. Surprisingly, this is not an isolated instance–mutual funds and individual investors who trade less often make more money. Partly because they reduce their costs and commissions, but also because the urge to always do something often leads to stupid mistakes.

Another good example of the benefits of sloth comes from investing in the S&P 500. As shown by a recent research article, you would have done better holding the original 500 companies in the S&P 500 and doing NOTHING rather than investing in the actual S&P 500 index (which adds or drops about 20 stocks each year). So even a 50 year vacation can be beneficial! And remember that the less frequently you trade, the fewer taxes you pay (because you are compounding pre-tax money–if you sell each year you compound after-tax money).

Disclosure: it has been far too long since I took a vacation!

Another record day

For my blog . . . 78 visitors yesterday, most of them reading my posts about StockLemon. I will now stop talking about that and HSOA and return to more interesting subjects, like investing.

StockLemon v. Home Solutions (HSOA) Redux

Ahh, Andrew Left’s ‘conference call‘ today regarding Home Solutions of America, Inc. [[HSOA]] was amusing. Andrew sounds very angry. His adversaries, the stupid traders who are long the stock, also sound angry. I did like the very British operator, and how she pronounced “Citron” (it sounded like ‘citrun’). That was very cute.

Me, I’m neither long nor short HSOA, and I am not angry. I think I’ll keep it that way!

My take on Andrew Left’s accusations against HSOA is that he brings up a lot of good points. The most damning evidence in my mind is the inability of the company to generate cash from their accounts receivables. There is no way I would go long HSOA.

Disclosure: I am not long or short HSOA and I have no affiliation with Andrew Left of StockLemon. I have a disclosure policy.

Can you trust the Stocklemon? Part 4

Well, I confirmed a bit more about Andrew Left of StockLemon (noted short seller and basher of bad microcap companies). He (or someone with the exact same name who lives in the same county, not likely) was convicted (in a civil case) of theft by double-cashing a check. I downloaded the original documents from the LA Superior Court website (case #bc269050). Since I am too lazy to put them up, you can see a copy of the writ of execution on the horrid StockLemon bashing site StockLemonAide.

Of course, when it comes down to it, you shouldn’t trust anyone, except maybe your mother (although don’t trust her for stock picks!). You shouldn’t even automatically trust me (although I am trustworthy). When it comes to investing especially, no one acts in a completely disinterested fashion. The kind of losers that praise a company such as HSOA on Yahoo’s message boards are long (or short) the stock and only want to pump (or deflate) it. Management of most every company wants to pump their company–sometimes this is just dumb, such as with CRMT or WHI, two stocks where I suffered losses after I trusted some bad management predictions–and sometimes this is fraudulent, such as in the case of Enron or Xybernaut. Short sellers (such as StockLemon) will try to bash a stock to get it to go lower.

The problem is that we cannot trust anyone. We need to verify the facts. Sometimes it will turn out that a company that looks to be failing or fraudulent will turn out to be a good company. Sometimes the short seller bashing the stock will turn out to be right (such as with Chanos and Enron or Andrew Left and GTX Global). What matters is the facts. Ironically, people like Andrew Left actually benefit the rubes that invest in fraudulent (or just bad) companies by ending the companies’ lives before they can obtain more money from investors.

See the previous posts in this series: Part 1, Part 2, Part 3

Disclosure: I am no longer long CRMT or WHI. I have no position in any other stocks mentioned. See my disclosure policy.