While searching for another FINRA decision I came across an extended hearing panel decision from February 27, 2018 by FINRA that lays out in detail many things that some penny stock traders have guessed or suspected about broker and market maker Wilson-Davis Co and Anthony Kerrigone. That FINRA decision is against Wilson-Davis & Co, James C. Snow (President and Chief Compliance Officer), and Byron B. Barkley (Head of Trading). Do note that this decision has been appealed to the FINRA appeals panel. Until the appeal is resolved the suspensions will not take effect and the fines will not have to be paid. It is possible that the respondents will win the appeal and face lesser sanctions or no sanctions.

I previously wrote about Wilson-Davis and Kerrigone a little over a year ago when the SEC fined Wilson-Davis for Reg SHO violations.

The penalties are (all quotes in this post are from the decision):

Respondent Wilson-Davis & Co. is fined $1,170,000 and ordered to disgorge $51,624 for improper short sales. For its failure to supervise and implement adequate AML procedures, Wilson-Davis is fined an additional 300,000,

while Respondents James Snow and Byron Barkley are fined $140,000 and $115,000, respectively, and both are suspended for one year and ordered to requalify before re-entering the industry.

The really interesting things in the decision all concern Anthony Kerrigone:

Wilson-Davis hired registered representative Anthony Kerrigone (“Kerrigone”) as a trader in September of 2008. Although Kerrigone maintained a small number of retail customers, his primary business was trading in one of the Firm’s proprietary accounts as a market maker in various securities. Kerrigone’s “niche” as a market maker was the markets of penny stock companies that traded in high volume following promotional or touting campaigns. Kerrigone researched stocks to find those that were experiencing a run up in price because “they were being promoted and touted,” even though the securities were “generally worthless” and “had zippo, no value.” Because the promoters “managed to figure out how they’d get a lot of people to buy” these “worthless” stocks, they presented a “trading opportunity” for Kerrigone.

Once Kerrigone identified a suitable “trading opportunity,” his activity in the security followed a consistent pattern. Kerrigone entered the market of an actively promoted stock by first selling the security short, on the assumption that once the market impact of promotional activity dissipated the stock would lose value. Although Kerrigone typically posted both “bid” and “ask” quotes as a market maker when he was first active in a stock, during this early period his “bid” quotes were generally not competitive with other market quotes, minimizing the possibility that he would actually purchase any significant quantities of the stock from the market as he shorted.

Later, as the effect of the promotional activity dissipated and value of the stock began to fall, Kerrigone moved his “bid” to a competitive level and executed market purchases of the stock sufficient to cover his short positions. During this latter stage, his “ask” quotes were typically away from the “inside” and not competitive with other market quotes, minimizing the possibility that he would sell additional stock and increase his diminishing short position. After fully covering his short position, he exited the market of the security. His trading in each security was brief, typically only a few trading days. By starting out as a net seller of the promoted stocks, accumulating his short position, and then buying to cover the stock he shorted, Kerrigone effectively piggy-backed the trajectory of potential “pump and dump” schemes to sell stock to the public while it was artificially inflated.

Kerrigone and his superiors at Wilson-Davis knew that Regulation SHO generally required a seller to borrow a security before selling the security short. But the Firm made no effort to do so before Kerrigone’s short selling. Instead, the Firm assumed that its trading fell within an exemption to the borrow requirement provided to Firms who engage in “bona-fide market making.” Kerrigone’s strategy was lucrative for both himself and Wilson-Davis. Kerrigone, who worked on a commission based on his trading profits, made in excess of $15 million between 2011 and 2013. During this time the Firm similarly made “tens of millions of dollars in profit.” The strategy is illustrated by Kerrigone’s trading in four penny stocks—Preventia, Inc. (“PVTA”), PM&E, Inc. (PMEA”), China Teletech Holdings (“CNCT”), and Lot 78, Inc. (“LOTE”).

My previous blog post about the SEC fine against Wilson-Davis for Reg SHO violations covers most of what FINRA alleges in this decision. More interesting is the description of the short squeeze in LOTE (Lot 78 Inc).

The decision describes Kerrigone’s trading in LOTE:

Like the other companies, Lot 78 was a penny stock whose market saw little or no activity before Kerrigone decided to trade the stock. Kerrigone began trading in LOTE on April 24, 2013. Unlike the other stocks, Kerrigone’s trading did not start immediately after promotional activity—instead, the promotion began on March 10, 2013, more than a month before Wilson-Davis entered the market. Kerrigone’s trading varied slightly from his typical pattern. He briefly accumulated a long position by purchasing LOTE stock at the market open on April 24, before changing direction less than an hour later placing a sale transaction of more than 1.1 million shares, resulting in a net short position of approximately 476,000 shares.

Similar to the other stocks, Wilson-Davis did not borrow the securities it sold short. Kerrigone continued to increase his short position to approximately 1 million shares by the end of the trading day.95 Kerrigone’s last purchase of the day was at a price of $2.45 per share. The next day, Kerrigone began purchasing stock to cover his short position, but found that unlike the price trajectory of the other stocks, the price of LOTE continued to increase.

After a single purchase of 256,878 shares at $3.34 per share, Kerrigone stopped making substantial efforts to cover and traded in only small volumes of LOTE as the stock price continued to rise throughout the day. Kerrigone’s last trade of the day was at $4.05 per share. Despite the fact that Kerrigone’s net short position decreased by approximately 250,000 shares as a result of his purchase, the value of his outstanding LOTE short position increased from approximately $2.4 million to $2.9 million as a result of the rising price of the stock.

On the third day after Kerrigone entered the market, the price of LOTE continued to rise. That morning, Kerrigone purchased another 199,132 shares to reduce his short position to approximately 544,576 shares, this time at a price of $4.81 per share. Kerrigone again traded only small volumes of the stock, with his last trade of the day at $6.05 per share. Despite the fact that his short position was again reduced, the increased share price meant that the value of the outstanding position that Kerrigone still needed to cover had increased to over $3.2 million.

Despite the rising price of LOTE, Firm policy required Kerrigone to cover his short position quickly. Kerrigone finally covered his net short position on the fourth trading day. He did so by executing a purchase of 545,388 shares at a price of $7.89 per share. After that fourth day, Kerrigone never traded in LOTE again. In total, Kerrigone executed at least 102 trades in LOTE during his trading, including 51 short sales.109 Because LOTE’s stock price did not follow Kerrigone’s anticipated trajectory and he had to purchase his covering shares at prices substantially higher than where he shorted, his trading in the stock resulted in a loss to WilsonDavis of more than $4.2 million.

Shortly thereafter, Wilson-Davis required Kerrigone to reimburse the Firm for its LOTE losses, and asked him to leave the Firm.

Kerrigone’s posted market maker quotations for LOTE during the period of his trading were once again more consistent with his effort to execute his trading strategy than actually providing general liquidity to the market as a market maker. During the early part of the trading when Kerrigone was accumulating his short position, Wilson-Davis’ posted bid was significantly away from the inside bid (82 percent of the time), ensuring that his bid would usually not result in market purchases. Indeed, even when Kerrigone purchased a large quantity of stock before building his short position, he did so by initiating transactions with other brokers at prices higher than Wilson-Davis’ own quoted bid price.

Later, when Kerrigone was attempting to cover, he ensured that Wilson-Davis’ posted sell quotes would not increase his short position by moving those posted quotes to levels significantly away from the inside ask (approximately 55 percent of the time). Moreover, during this later period, Wilson-Davis’ posted bid quotes were also almost always significantly away from the inside bid (approximately 92 percent of the time), as Kerrigone sought to avoid buying as well in light of the increasing price of LOTE stock, providing little liquidity to the market in either direction.

This provides clarity about a short squeeze that traders at the time saw happen in real time. As the decision states, “He briefly accumulated a long position by purchasing LOTE stock at the market open on April 24, before changing direction less than an hour later placing a sale transaction of more than 1.1 million shares, resulting in a net short position of approximately 476,000 shares.” As I remember it (I was trading the stock at the time although in very small size), the full size of that sell order was shown to the market. After the price of the stock declined in reaction to the large sell order, the order was filled completely and the stock quickly bounced. The trading and short squeeze in LOTE was first reported by Promotion Stock Secrets.

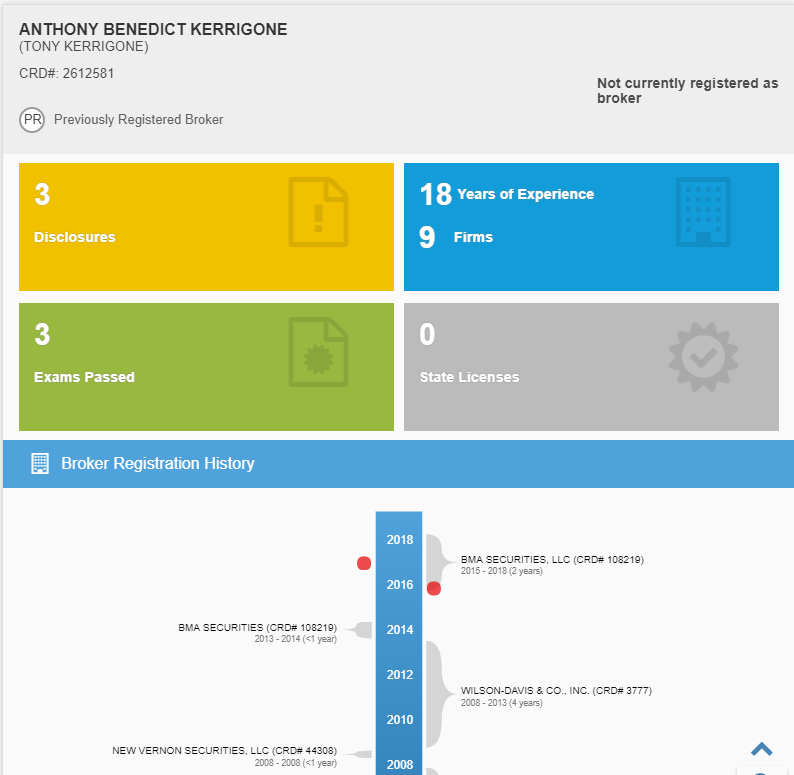

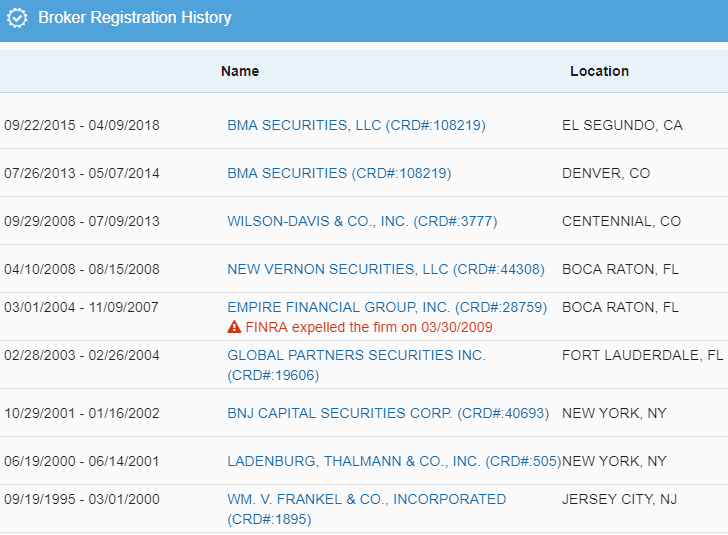

According to FINRA Brokercheck, Anthony Kerrigone is no longer employed by BMA Securities; his last day there was reportedly April 9, 2018. He is not currently registered as a broker.

Disclaimer. No position in any stock mentioned and I have no relationship with anyone mentioned in this post except that I am a subscriber to Promotion Stock Secrets and have been for a few years. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.

Nope. Not even close.

Would you care to elaborate? If you think FINRA got the facts wrong I would be happy to get your side of the story.

The NAC decision was published yesterday: https://www.finra.org/sites/default/files/fda_documents/2012032731802%20Wilson-Davis%20%26%20Co.%2C%20Inc.%20CRD%203777%20James%20C.%20Snow%20CRD%202761102%20Byron%20B.%20Barkley%20CRD%2012469%20NAC%20Decision%20%20va.pdf

Wilson-Davis’ fine was reduced somewhat and the fines and suspensions of Snow and Barkley were greatly reduced. No word yet on whether the decision will be appealed to the SEC.