I’ll pile in along with others linking to this wonderful ode to the over-leveraged hedge fund. I will discuss recent hedge fund troubles within the next couple days. Unfortunately, the same problems that have caused Goldman Sach’s Global Alpha fund to lose 40% this year have hurt my portfolios too (although much less).

Category: Stocks

Regent Communications (RGCI) Executives Should be Fired!

You heard it here first, although if you have read the company’s SEC filings it would be obvious. First, I should state that I am not an impartial observer of the company and of the failings of its management. I have been a shareholder for a few months and I intend to remain a shareholder for some time. I bought into the company well aware of the management’s failings, but believing that the company would easily be worth 50% more than I paid should management suddenly get fired. That is not a strategy I recommend unless you are a hedge fund with the money to buy a large stake in a company. I have been burned once before with this strategy, with Career Education [[CECO]], which I bought during a shareholder’s proxy fight against management that he ultimately lost (and I lost money on that).

Regent Communications, trading around $3 currently, [[RGCI]] is a small radio company with radio stations in a number of ‘mid-market’ cities, such as Buffalo, New York. The company aims to have a number of stations in each of its markets so that it can spread out fixed costs over greater revenue. The company’s stations have eked out small increases in revenues over the last few years, despite the tough advertising market. The company increased its size last year by buying a number of stations from ABC radio. Regent Communications trades at a very modest P/CF (price to cash flow) ratio of 10.9 on a trailing twelve months basis.

So what is wrong with Regent management? For starters, they are paid too much for what they do: $670k and $500k last year for the two top executives (see the 2006 proxy for details). While that does not seem like much, that includes substantial bonuses in a year in which the company’s stock price nose-dived by 40% and operational improvements were minor. Also, keep in mind that radio is not a business where the top executives need to do much–all they really do is decide on a few broad initiatives and allocate capital. The station managers could easily do their jobs autonomously.

Oh, and with regards to allocating capital, Regent is horrible. The company bought back loads of stock at much higher prices in 2005 and 2006. Then it took on loads of debt to buy new stations last fall. Even as the stock price was falling the company stopped buying back more stock. The company generates strong and stable cash flows, and is in a mature industry, yet it pays no dividend.

I am not the only one disappointed with Regent’s management. One hedge fund, Riley Investment Management (which holds or controls 7.4% of RGCI), tried to call a special meeting to elect new directors. The company blocked the move. So earlier this week, Riley filed suit against Regent because Regent would not provide it with a list of shareholders or allow it to call a special shareholders meeting for the purpose of electing new directors. You can see Riley’s original letter to Regent dated July 19, 2007. The company’s charter allows for 20% of shareholders to call a special meeting of shareholders, and Riley asserts that it and several other shareholders easily

Just yesterday (August 15, 2007), Regent Communications filed a lawsuit against the hedge funds that are suing it–Riley Investment Partners Master Fund, L.P. and Riley Investment Management LLC, (collectively “Riley”) and SMH Capital Inc. (“SMH Capital”). While I have no clue as to the legal validity of Regent’s claim, it is obvious that this is an attempt to prevent Riley from calling a special shareholder’s meeting and getting a list of all shareholders.

I hope that the directors suddenly remember their fiduciary duty to shareholders and fire management and then began a liquidation of the company. An orderly liquidation of the company could easily bring $4.50 or more per share to shareholders. This was first proposed by Riley back in April (see their letter at the end of their 13d filing), but the company ignored them. If Riley has to win in court to get their director nominees elected and to get the company sold or liquidated, the legal costs could erode some of Regent’s value.

Disclosure: I hold RGCI stock. My disclosure policy makes for good reading.

Doing well on CAPS

While doing well with real money is always nice, it is fun to play with fake money too. I am currently ranked in the 40 players out of more than 33,000 on Motley Fool Caps. There are only two other players who started after me who are ranked higher. Not bad, eh?

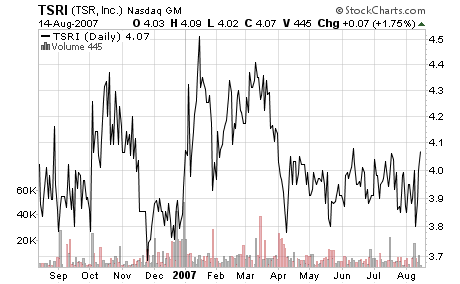

Of risk and microcaps: TSR, Inc. (TSRI)

There are those that say that microcaps are inherently risky. They are wrong. There are those that say that stocks with low prices (ie, below $5) are inherently risky. They are wrong. There are those that say that OTC BB, pink sheets, or unlisted stocks are inherently risky. They are wrong. (Although, to be fair, most unlisted stocks are not good investments; but that does not mean that being unlisted makes a stock a bad investment.)

For example, I am aware of a couple private companies based near my hometown that I would love to own (if the price were fair), even though they are private (for the record, both are closely held by only a couple people; one of them is Chemtool). As long as I don’t overpay, it doesn’t matter to me if the company is small, the stock is hard to sell, or the financials are not filed with the SEC. As long as I can get my hands on the financial statements and I can trust them, I have no problem owning tiny or illiquid companies. Neither should you.

Perhaps my favorite tiny company that you can buy is TSR, Inc. [[TSRI]], currently trading at just over $4.00. The company sports a book value of $3.05 per share, and most of that is in the form of cash, short-term treasury bills, and short-term receivables. I estimate that the company has a liquidation value of $13 million (compared to a $18.6 million market cap), meaning that in a worst-case scenario we would not expect to lose more than 31% of our investment. The company, currently going through tough times, remains profitable (even excluding interest on its investments). If the company were to utilize its excess cash to fund a special dividend or to buy back stock, while its operations improved modestly to historic norms, the stock could easily increase 50% or more in value. In the meantime, the stock’s nice 8% dividend yield is nice (although keep in mind that the payout yield is over 100%, so some of that dividend currently represents return of capital).

TSR Inc. is a staffing company in New York for computer programmers and related professionals. A large chunk of the company is still owned by its founder, who has also recently bought stock on the open market at around $4 per share. I should note that the founder, Joseph Hughes, has previously been successful when trading TSR’s stock–he sold a large number of shares back in 2004 when TSR’s stock was much higher.

Disclosure: I own TSRI. If you follow my portfolios, you will notice that I sold off a large percentage of the shares I owned a couple weeks ago. This was for strategic reasons (allocating money to a better opportunity). I continue to own what for me is a normal-sized stake in TSRI. See my disclosure policy.

Of babies and bathwater: International Shipholding (ISH)

Turmoil in the markets continues. Today getting slaughtered (down below $16) was International Shipholding Corporation [[ISH]]. The company reported no news and yet the stock dropped 20%. It is now trading at 2/3 book value. One nice thing about the shipping companies–they are generally worth around book value. So if you find one that is selling at a significant discount to that and there is nothing highly wrong with the company, it could very well be a good investment. One thing to note is that most shipping companies are not the best in terms of corporate governance.

Disclosure: I own ISH. My disclosure policy will never sink.

The Value of Sloth

Are you worried that you aren’t doing enough to increase your investment performance? Perhaps all you need to do is go on a 2.5 year vacation. According to Mark Hulbert, the best performing investment newsletter over the last 5 years has not been published in the last 2.5 years. So by doing absolutely nothing it has garnered great profits. Surprisingly, this is not an isolated instance–mutual funds and individual investors who trade less often make more money. Partly because they reduce their costs and commissions, but also because the urge to always do something often leads to stupid mistakes.

Another good example of the benefits of sloth comes from investing in the S&P 500. As shown by a recent research article, you would have done better holding the original 500 companies in the S&P 500 and doing NOTHING rather than investing in the actual S&P 500 index (which adds or drops about 20 stocks each year). So even a 50 year vacation can be beneficial! And remember that the less frequently you trade, the fewer taxes you pay (because you are compounding pre-tax money–if you sell each year you compound after-tax money).

Disclosure: it has been far too long since I took a vacation!

Another record day

For my blog . . . 78 visitors yesterday, most of them reading my posts about StockLemon. I will now stop talking about that and HSOA and return to more interesting subjects, like investing.

StockLemon v. Home Solutions (HSOA) Redux

Ahh, Andrew Left’s ‘conference call‘ today regarding Home Solutions of America, Inc. [[HSOA]] was amusing. Andrew sounds very angry. His adversaries, the stupid traders who are long the stock, also sound angry. I did like the very British operator, and how she pronounced “Citron” (it sounded like ‘citrun’). That was very cute.

Me, I’m neither long nor short HSOA, and I am not angry. I think I’ll keep it that way!

My take on Andrew Left’s accusations against HSOA is that he brings up a lot of good points. The most damning evidence in my mind is the inability of the company to generate cash from their accounts receivables. There is no way I would go long HSOA.

Disclosure: I am not long or short HSOA and I have no affiliation with Andrew Left of StockLemon. I have a disclosure policy.

Can you trust the Stocklemon? Part 4

Well, I confirmed a bit more about Andrew Left of StockLemon (noted short seller and basher of bad microcap companies). He (or someone with the exact same name who lives in the same county, not likely) was convicted (in a civil case) of theft by double-cashing a check. I downloaded the original documents from the LA Superior Court website (case #bc269050). Since I am too lazy to put them up, you can see a copy of the writ of execution on the horrid StockLemon bashing site StockLemonAide.

Of course, when it comes down to it, you shouldn’t trust anyone, except maybe your mother (although don’t trust her for stock picks!). You shouldn’t even automatically trust me (although I am trustworthy). When it comes to investing especially, no one acts in a completely disinterested fashion. The kind of losers that praise a company such as HSOA on Yahoo’s message boards are long (or short) the stock and only want to pump (or deflate) it. Management of most every company wants to pump their company–sometimes this is just dumb, such as with CRMT or WHI, two stocks where I suffered losses after I trusted some bad management predictions–and sometimes this is fraudulent, such as in the case of Enron or Xybernaut. Short sellers (such as StockLemon) will try to bash a stock to get it to go lower.

The problem is that we cannot trust anyone. We need to verify the facts. Sometimes it will turn out that a company that looks to be failing or fraudulent will turn out to be a good company. Sometimes the short seller bashing the stock will turn out to be right (such as with Chanos and Enron or Andrew Left and GTX Global). What matters is the facts. Ironically, people like Andrew Left actually benefit the rubes that invest in fraudulent (or just bad) companies by ending the companies’ lives before they can obtain more money from investors.

See the previous posts in this series: Part 1, Part 2, Part 3

Disclosure: I am no longer long CRMT or WHI. I have no position in any other stocks mentioned. See my disclosure policy.

Can you trust the Stocklemon? Part 3

Andrew Left of StockLemon (www.citronresearch.com) has been accused of many things. One accusation that I have verified (assuming the person is not a different Andrew Left) is that he was barred from the commodities/futures industry for three years back in 2000. You can see details of the case here.

Basically, the whole firm for which he worked was accused and convicted of wrongdoing. A number of the principals and employees were fined, whereas Andrew Left was not fined at all. So while this is a mark against him, it is not as black a mark as StockLemon’s enemies believe it to be.

Here is a snippet of the decision regarding left:

“ANDREW LEFT-

THE PANEL FOUND THAT LEFT MADE FALSE AND MISLEADING STATEMENTS TO CHEAT, DEFRAUD OR DECEIVE A CUSTOMER IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). LEFT’S CONDUCT WAS INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE.

CONSEQUENTLY, THE PANEL BARRED LEFT FROM ASSOCIATION WITH AND FROM ACTING AS A PRINCIPAL OF ANY NFA MEMBER FOR THREE YEARS; ORDERED HIM TO TAKE AN ETHICS TRAINING COURSE; AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR TWO YEARS WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO TAPE RECORD AND LOG ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS.”

The full decision can be found online at the National Futures Association website. Following is the complaint by the NFA:

COMPLAINT –

THE COMPLAINT ALLEGED THAT UCC, STERN AND SAATHOFF USED DECEPTIVE AND MISLEADING PROMOTIONAL MATERIAL, IN VIOLATION OF NFA COMPLIANCE RULES RULES 2-29(a)(1), 2-29(b)(1) AND 2-29(b)(2). THE COMPLAINT ALSO ALLEGED THAT UCC, BURSTEEN, SOMMERS, BUSHEY, BRIDGES, STEINFELD, DAYAN, PARKS, ZAGER, ZINNER, VITELLO, GETZ, LEFT AND MULLER CHEATED, DEFRAUDED AND DECEIVED COMMODITY FUTURES CUSTOMERS AND ENGAGED IN SOLICITATIONS WHICH OPERATED AS A FRAUD OR DECEIT, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). MOREOVER, THE COMPLAINT ALLEGED THAT UCC, SOMMERS, ZAGER, GROSS AND GETZ FAILED TO OBSERVE HIGH STANDARDS OF COMMERCIAL HONOR AND JUST AND EQUITABLE PRINCIPLES OF TRADE IN THE CONDUCT OF THEIR COMMODITY FUTURES BUSINESS, IN VIOLATION OF NFA COMPLIANCE RULE 2-4. FURTHERMORE, THE COMPLAINT ALLEGED THAT UCC, STERN, SAATHOFF, KAHN, FREEDBERG AND CIARAMELLA FAILED TO DILIGENTLY CARRY OUT THEIR SUPERVISORY RESPONSIBILITIES, IN VIOLATION OF NFA COMPLIANCE RULE 2-9.

Following are the more severe punishments meted out to some of the other people involved, which involve fines and longer bans / suspensions from the futures industry:

DECISION – SOMMERS

ON JUNE 16, 1997, NFA’S BUSINESS CONDUCT COMMITTEE ISSUED A DECISION ACCEPTING SOMMERS’ SETTLEMENT OFFER IN WHICH HE NEITHER ADMITTED NOR DENIED THE ALLEGATIONS OF THE COMPLAINT. THE BCC SUSPENDED SOMMERS FOR TWO YEARS AND SIX MONTHS, WITH CREDIT TOWARDS THE SUSPENSION PERIOD GIVEN FOR THE PAST TWO YEARS AND THREE MONTHS THAT SOMMERS HAS NOT WORKED IN THE COMMODITIES INDUSTRY. THE BCC ALSO ORDERED THAT SOMMERS SHALL TAPE RECORD ALL OF HIS TELEPHONE SOLICITATIONS FOR TWO YEARS AND RETAIN ALL TAPES FOR AT LEAST TWELVE MONTHS AND MAKE THE TAPES AVAILABLE TO NFA UPON REQUEST. IN ADDITION, THE BCC ORDERED THAT SOMMERS SHALL TESTIFY AT THE HEARING FOR RESPONDENTS IN THIS MATTER REGARDING HIS EXPERIENCE WHILE WORKING AT UCC. THE BCC FURTHER ORDERED THAT SOMMERS SHALL SUBMIT TO AN EXPEDITED HEARING PROCESS REGARDING ALLEGED SALES PRACTICE VIOLATIONS OR FAILURE TO FULFILL THE AFOREMENTIONED TAPE RECORDING REQUIREMENTS. FURTHERMORE, THE BCC ORDERED SOMMERS TO PAY A $10,000 FINE. THIS DECISION BECOMES EFFECTIVE JULY 1, 1997.

DECISION – UCC, STERN AND SAATHOFF

ON JUNE 16, 1997, NFA’S BCC ISSUED A DECISION ACCEPTING UCC, STERN AND SAATHOFF’S SETTLEMENT OFFER IN WHICH THEY NEITHER ADMITTED NOR DENIED THE ALLEGATIONS OF THE COMPLAINT. THE BCC ORDERED UCC, STERN AND SAATHOFF TO REDUCE THE NUMBER OF THE FIRM’S APS TO NO MORE THAN 66 WITHIN 60 DAYS. THE BCC ALSO ORDERED UCC, STERN AND SAATHOFF TO SUBMIT PROMOTIONAL MATERIAL TO NFA FOR REVIEW AND APPROVAL AT LEAST TWENTY-ONE DAYS PRIOR TO ITS FIRST USE. IN ADDITION, THE BCC ORDERED UCC, STERN AND SAATHOFF TO TAPE RECORD AND RETAIN TAPES OF ALL TELEPHONE CONVERSATIONS BETWEEN APS AND EXISTING AND PROSPECTIVE CUSTOMERS AND MAINTAIN A DAILY WRITTEN LOG FOR EACH CONVERSATION REFLECTING THE IDENTITY OF EACH CUSTOMER OR PROSPECTIVE CUSTOMER AND THE DATE OF EACH CONVERSATION. THESE TAPES SHALL BE PRODUCED WITHIN TEN DAYS FROM NFA’S WRITTEN REQUEST. IN ADDITION, THE BCC ORDERED THAT UCC, STERN AND SAATHOFF RESTRICT PROMOTIONAL MATERIAL AND AP SOLICIATIONS TO EXCLUDE ANY STATEMENT WHICH MAKES REFERENCE TO PROFITS WHICH COULD BE ACHIEVED IN THE FUTURE OR COULD HAVE BEEN ACHIEVED IN THE PAST BY TRADING FUTURES OR OPTIONS ON FUTURES. THE BCC ALSO ORDERED THAT UCC AND ITS APS SHALL NOT DEMONSTRATE THE EFFECTS OF LEVERAGE IN TRADING FUTURES AND OPTIONS BY USING SPECIFIC EXAMPLES OF THE PROFITS WHICH CAN BE ACHIEVED UNLESS THEY MAKE IT CLEAR THAT NO REPRESENTATION IS MADE THAT UCC’S CUSTOMERS HAVE MADE OR ARE LIKELY TO MAKE SUCH PROFITS. THE BCC FURTHER ORDERED THAT UCC, STERN AND SAATHOFF PROVIDE ADDITIONAL ETHICS TRAINING FOR APS. THE BCC ALSO ORDERED THAT UCC, STERN AND SAATHOFF EMPLOY A FULL-TIME COMPLIANCE OFFICER AND TO AGREE NOT TO COMPENSATE SUPERVISORS BASED ON THE NUMBER OF TRADES EXECUTED BY THE FIRM. THE BCC ORDERED UCC, STERN AND SAATHOFF TO SUBMIT TO AN EXPEDITED HEARING PROCESS WITH 75 DAYS BEFORE A SUBCOMMITTEE OF NFA’S HEARING COMMITTEE REGARDING ALLEGED VIOLATIONS OF ANY CONDITIONS OR TERMS OF THE OFFER OF SETTLEMENT AND THE DECISION. THE BCC FURTHER ORDERED UCC, STERN AND SAATHOFF TO PAY A FINE IN THE AMOUNT OF $200,000. FURTHERMORE, THE BCC ORDERED THAT UCC, STERN AND SAATHOFF AGREE THAT THE TERMS AND CONDITIONS OF THIS DECISION AND THE OFFER OF SETTLEMENT SHALL APPLY TO ANY NFA-REGISTERED FIRM OF WHICH STERN AND/OR SAATHOFF ARE LISTED PRINICPALS. THIS DECISION BECOMES EFFECTIVE JULY 1, 1997.

DECISION – FREEDBERG, KAHN AND CIARAMELLA

ON JULY 2, 1997, NFA’S BCC ISSUED A DECISION ACCEPTING FREEDBERG’S, KAHN’S AND CIARAMELLA’S SETTLEMENT OFFERS IN WHICH THEY NEITHER ADMITTED NOR DENIED THE ALLEGATIONS OF THE COMPLAINT. THE BCC ORDERED FREEDBERG AND KAHN TO EACH PAY A FINE IN THE AMOUNT OF $20,000 AND ORDERED CIARAMELLA TO PAY A FINE IN THE AMOUNT OF $10,000. THE BCC ALSO ORDERED FREEDBERG, KAHN AND CIARAMELLA TO ONLY ACT AS NFA ASSOCIATES AND PROHIBITED THEM FROM ACTING AS A PRINCIPAL OF AN NFA MEMBER OR IN A SUPERVISORY CAPACITY FOR A PERIOD OF FIVE YEARS. THE BCC ORDERED THAT FOR A PERIOD OF TWO YEARS FREEDBERG AND KAHN SHALL TAPE RECORD ALL TELEPHONE CONVERSATIONS WITH CUSTOMERS AND RETAIN THESE TAPES FOR TWO YEARS. FREEDBERG AND KAHN SHALL MAKE THE TAPES AVAILABLE TO NFA UPON REQUEST. FREEDBERG AND KAHN SHALL ALSO MAINTAIN DAILY WRITTEN LOGS OF THEIR SOLICITATIONS. THIS DECISION BECOMES EFFECTIVE JULY 17, 1997.

DECISION – MICHAEL D. BUSHEY

ON JULY 28, 1997, THE HEARING PANEL ISSUED A DECISION ACCEPTING BUSHEY’S SETTLEMENT OFFER IN WHICH HE NEITHER ADMITTED NOR DENIED THE ALLEGATIONS ALLEGED IN THE COMPLAINT. THE HEARING PANEL BARRED BUSHEY FROM APPLYING FOR NFA MEMBERSHIP OR ASSOCIATE MEMBERSHIP, OR FROM ACTING AS A PRINCIPAL OF AN NFA MEMBER, FOR A PERIOD OF SIX YEARS, WITH CREDIT FOR THE THREE YEARS DURING WHICH HE HAS NOT WORKED IN THE FUTURES INDUSTRY. AT THE END OF THE AFOREMENTIONED BAR, BUSHEY MAY APPLY FOR NFA ASSOCIATE MEMBERSHIP ONLY, PROVIDED THAT HE SHALL NOT ACT AS A PRINCIPAL OR SUPERVISE ANY NFA MEMBER FOR TWO YEARS AFTER NFA ASSOCIATE MEMBERSHIP IS GRANTED.

IN ADDITION, BUSHEY MUST TAPE RECORD ALL OF HIS CONVERSATIONS WITH EXISTING AND POTENTIAL CUSTOMERS FOR TWO YEARS AFTER HE IS GRANTED NFA ASSOCIATE MEMBERSHIP AND RETAIN EACH TAPE FOR TWO YEARS. BUSHEY MUST ALSO MAINTAIN A DAILY WRITTEN LOG OF EACH CONVERSATION, IDENTIFYING THE CUSTOMER HE SPOKE WITH AND THE DATE. MOREOVER, ANY MEMBER SPONSORING BUSHEY AS AN ASSOCIATE MUST AGREE IN WRITING TO PERFORM THE SUPERVISORY UNDERTAKINGS CONTAINED IN THE SUPERVISORY AGREEMENT ATTACHED TO BUSHEY’S OFFER OF SETTLEMENT.

AT THE END OF THE AFOREMENTIONED MEMBERSHIP BAR, NEITHER THE COMPLAINT NOR THE DECISION IN THIS CASE SHALL SERVE AS THE SOLE BASIS FOR A PROCEEDING TO DENY BUSHEY’S NFA ASSOCIATE MEMBERSHIP. THIS DECISION BECOMES EFFECTIVE AUGUST 12, 1997.

…

WILLIAM KELLY PARKS –

THE PANEL FOUND THAT PARKS MADE FALSE AND MISLEADING STATEMENTS THAT WERE INTENDED TO CHEAT, DEFRAUD, AND DECEIVE CUSTOMERS, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). PARK’S CONDUCT WAS INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE.

CONSEQUENTLY, THE PANEL FINED PARKS $10,000; BARRED HIM FROM ASSOCIATION WITH OR ACTING AS A PRINCIPAL OF ANY NFA MEMBER FOR ONE YEAR; ORDERED HIM TO TAKE AN ETHICS TRAINING COURSE; AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR THREE YEARS, WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO TAPE RECORD AND LOG ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS.

…

ARNOLD ZAGER –

THE PANEL FOUND THAT ZAGER MADE FALSE AND MISLEADING STATEMENTS THAT WERE INTENDED TO AND DID CHEAT A CUSTOMER, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). FURTHER, ZAGER ENGAGED IN CONDUCT INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE, IN VIOLATION OF NFA COMPLIANCE RULE 2-4.

CONSEQUENTLY, THE PANEL FINED ZAGER $10,000; BARRED HIM FROM ASSOCIATION WITH AND FROM ACTING AS A PRINCIPAL OF ANY NFA MEMBER FOR THREE YEARS; ORDERED HIM TO ATTEND AN ETHICS TRAINING COURSE; AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR THREE YEARS WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO TAPE RECORD AND LOG ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS. DAVID BRIDGES –

THE PANEL FOUND THAT BRIDGES MADE FALSE AND MISLEADING STATEMENTS IN RECKLESS DISREGARD FOR THE TRUTH, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). BRIDGES’ CONDUCT WAS INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE.

CONSEQUENTLY, THE PANEL FINED BRIDGES $5,000 AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR THREE YEARS WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO TAPE RECORD AND LOG ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS.

…

BENJI DAYAN –

THE PANEL FOUND THAT DAYAN MADE FALSE AND MISLEADING STATEMENTS WITH A RECKLESS DISREGARD FOR THE TRUTH, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). DAYAN’S CONDUCT WAS INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE.

CONSEQUENTLY, THE PANEL FINED DAYAN $2,000; AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR THREE YEARS WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO TAPE RECORD AND LOG ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS.

JEFFREY BURSTEEN –

THE PANEL FOUND THAT BURSTEEN MADE STATEMENTS THAT WERE INTENDED TO CHEAT, DEFRAUD, OR DECEIVE CUSTOMERS, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). BURSTEEN’S CONDUCT WAS INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE.

CONSEQUENTLY, THE PANEL FINED BURSTEEN $5,000; BARRED HIM FROM ASSOCIATION WITH AND FROM ACTING AS A PRINCIPAL OF ANY NFA MEMBER FOR ONE YEAR; ORDERED HIM TO TAKE AN ETHICS TRAINING COURSE; AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR THREE YEARS WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO LOG AND TAPE RECORD ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS.

KENNETH ZINNER –

THE PANEL FOUND THAT ZINNER MADE FALSE AND MISLEADING STATEMENTS THAT WERE INTENDED TO AND DID CHEAT, DEFRAUD, AND DECEIVE CUSTOMERS, IN VIOLATION OF NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1). ZINNER’S CONDUCT WAS INCONSISTENT WITH JUST AND EQUITABLE PRINCIPLES OF TRADE.

CONSEQUENTLY, THE PANEL FINED ZINNER $15,000; BARRED HIM FROM ASSOCIATION WITH AND FROM ACTING AS A PRINCIPAL OF ANY NFA MEMBER FOR THREE YEARS; ORDERED HIM TO TAKE AN ETHICS TRAINING COURSE; AND PLACED RESTRICTIONS ON HIS ACTIVITIES FOR THREE YEARS WHICH PREVENT HIM FROM SUPERVISING ANY AP AND REQUIRE HIM TO LOG AND TAPE RECORD ALL CONVERSATIONS WITH CURRENT AND POTENTIAL CUSTOMERS.

…

BRIDGES’ AND DAYAN’S APPEALS –

ON MARCH 3, 1998, DAVID RAY BRIDGES AND BENJI SCOTT DAYAN FILED NOTICES OF APPEAL FROM THE HEARING PANEL’S DECISION WITH NFA’S APPEALS COMMITTEE. BRIDGES AND DAYAN REQUEST THAT THE APPEALS COMMITTEE REVERSE THE HEARING PANEL’S DECISION AS TO THEM IN ITS ENTIRETY.

DECISION –

ON MAY 13, 1998, NFA’S APPEALS COMMITTEE ISSUED A DECISION ACCEPTING DAYAN’S SETTLEMENT OFFER. THE APPEALS COMMITTEE AFFIRMED THE HEARING PANEL’S FINDINGS THAT DAYAN VIOLATED NFA COMPLIANCE RULES 2-2(a) AND 2-29(a)(1).

THE APPEALS COMMITTEE ALSO ORDERED DAYAN TO WITHDRAW FROM ANY STATUS WHICH HE HAS WITH NFA AND/OR THE CFTC AND ORDERED DAYAN TO NOT APPLY WITH NFA OR THE CFTC IN ANY CAPACITY FOR ONE YEAR. DURING THIS ONE-YEAR BAR FROM NFA AND THE CFTC, DAYAN IS REQUIRED TO ATTEND A FOUR-HOUR ETHICS TRAINING COURSE AND TO TAKE AND PASS THE SERIES 3 EXAM BEFORE RE-APPLYING FOR REGISTRATION. THE APPEALS COMMITTEE ALSO IMPOSED RESTRICTIONS AND CONDITIONS ON DAYAN’S REGISTERED ACTIVITIES FOR A PERIOD OF THREE YEARS EXCLUSIVE OF ANY PERIOD DURING WHICH DAYAN IS NOT AN ASSOCIATE OF AN NFA MEMBER. THIS DECISION BECOMES EFFECTIVE ON MAY 18, 1998.

NFA APPEALS COMMITTEE DECISION–PARKS, ZINNER AND BRIDGES

On March 14, 2000, NFA’s Appeals Committee issued a Decision affirming in all respects the NFA Hearing Panel’s findings that Parks and Bridges violated NFA Compliance Rules, and affirming in part and modifying in part the NFA Hearing Panel’s penalties imposed on Parks, Zinner and Bridges.

Specifically, the Appeals Committee affirmed the $10,000 fine the Hearing Panel had imposed on Parks, but modified the sanctions to permanently bar him from NFA membership and Associate and principal status with any NFA Member.

Furthermore, the Appeals Committee affirmed the $15,000 fine the Hearing Panel had imposed on Zinner, but modified the sanctions to permanently bar him from NFA memberhsip and Associate and principal status with any NFA Member.

Moreover, the Appeals Committee affirmed the $5,000 fine the Hearing Panel had imposed on Bridges, but modified the sanctions to bar him for two years from NFA membership and Associate and principal status with any NFA Member. Further, the Appeals Committee imposed the following restrictions and conditions on Bridges’ activities for three years after his two-year bar expires: (i) he may not function as a principal, partner, officer, director, or branch manager of any NFA Member; (ii) he may not become or remain associated with any NFA Member (sponsor) unless the sponsor agrees in writing to establish and implement written supervisory policies and procedures to ensure that his activities are in compliance with the restrictions imposed by this Decision, and certifies that it understands that any violation of its obligation under this Decision may be grounds for disciplinary action against the sponsor; (iii) he may not directly or indirectly exercise supervisory authority over any person required to be registered as an AP; and (iv) his sponsor must tape record all conversations that occur between him and both existing and potential customers (and Bridges must have no control over the taping process), retain each tape for two years, and maintain a daily written log that reflects, at a minimum, the first and last name of each existing and potential customer that he spoke with on that day.

This Decision becomes effective April 13, 2000.

Disclosure: I have no connection with Andrew Left. I have never traded futures. I have never been convicted of anything above the level of a parking ticket. This article was edited on June 4, 2009 to remove some of the complaint (the full complaint had been posted) to make the article more concise and also at the request of one of the three named defendants against whom the NFA dropped its charges.