I just saw that Delaney Equity Group LLC (a small broker and OTC market maker) has been criminally charged in an ongoing ‘shell factory’ investigation. See the Palm Beach Post story. Below I have downloaded the court docket and linked all the documents currently available. I intend to post updates to this occasionally (at least for important filings). Read the complaint. The SEC had filed civil charges against Delaney back in 2015.

Excerpt from the complaint:

7. DELANEY EQUITY GROUP LLC, lndividual A, and Ian C. Kass would prepare Forms 211 on behalf of the issuers and submit them to the Financial Industry Regulatory Authority (“FINRA”) so that shares of the issuers could be quoted and traded over-the-counter. These forms falsely and fraudulently represented that the companies were executing their business plans and were operating under the direction of the straw CEO.

The allegations go on, but the fact that the forms 211 are mentioned is a big deal for OTC Markets in my opinion– this could scare off market makers from filing these forms for any sketchy company in the future.

U.S. District Court

Southern District of Florida (Miami)

CRIMINAL DOCKET FOR CASE #: 1:18-cr-20336-CMA All Defendants

| Case title: USA v. Delaney Equity Group LLC | Date Filed: 04/26/2018 |

| Assigned to: Judge Cecilia M. Altonaga | ||

| Defendant (1) | ||

| Delaney Equity Group LLC | represented by | Ryan Dwight O’Quinn DLA Piper LLP (US) 200 South Biscayne Boulevard Suite 2500 Miami, FL 33131 305-423-8553 Fax: 305-675-0807 Email: ryan.oquinn@dlapiper.com LEAD ATTORNEY ATTORNEY TO BE NOTICEDElan Abraham Gershoni DLA Piper LLP (US) 200 S. Biscayne Boulevard Suite 2500 Miami, FL 33131 305.423.8500 Fax: 305.675.0527 Email: Elan.Gershoni@dlapiper.com ATTORNEY TO BE NOTICED |

| Pending Counts | Disposition | |

| 18:371.F CONSPIRACY TO UNLAWFULLY SELL UNREGISTERED SECURITIES (1) |

||

| Highest Offense Level (Opening) | ||

| Felony | ||

| Terminated Counts | Disposition | |

| None | ||

| Highest Offense Level (Terminated) | ||

| None | ||

| Complaints | Disposition | |

| None |

| Plaintiff | ||

| USA | represented by | Jerrob Duffy United States Attorney’s Office 99 N.E. Fourth Street 4th Floor Miami, FL 33132 305-961-9273 Fax: 305-536-5321 Email: jerrob.duffy@usdoj.gov LEAD ATTORNEY ATTORNEY TO BE NOTICED Designation: Retained |

| Date Filed | # | Docket Text |

|---|---|---|

| 04/26/2018 | 1 | INFORMATION as to Delaney Equity Group LLC (1) count 1 and FORFEITURE COUNT. (wc) (Entered: 04/26/2018) |

| 04/26/2018 | 2 | NOTICE of Similar Action by USA as to Delaney Equity Group LLC (Duffy, Jerrob) (Entered: 04/26/2018) |

| 04/26/2018 | 3 | NOTICE OF ATTORNEY APPEARANCE: Ryan Dwight O’Quinn appearing for Delaney Equity Group LLC . Attorney Ryan Dwight O’Quinn added to party Delaney Equity Group LLC(pty:dft). (O’Quinn, Ryan) (Entered: 04/26/2018) |

| 04/26/2018 | 4 | NOTICE OF ATTORNEY APPEARANCE: Elan Abraham Gershoni appearing for Delaney Equity Group LLC . Attorney Elan Abraham Gershoni added to party Delaney Equity Group LLC(pty:dft). (Gershoni, Elan) (Entered: 04/26/2018) |

| 05/09/2018 | 5 | PAPERLESS NOTICE OF HEARING as to Delaney Equity Group LLC: Change of Plea Hearing set for 5/21/2018 08:30 AM in Miami Division before Judge Cecilia M. Altonaga. (ps1) (Entered: 05/09/2018) |

| 05/09/2018 | 6 | PAPERLESS NOTICE OF HEARING as to Delaney Equity Group LLC: Initial Appearance and Arraignment set for 5/21/2018 08:30 AM in Miami Division before Judge Cecilia M. Altonaga. (ps1) (Entered: 05/09/2018) |

| 05/21/2018 | 7 | WAIVER OF INDICTMENT by Delaney Equity Group LLC (ps1) (Entered: 05/21/2018) |

| 05/21/2018 | 8 | PAPERLESS Minute Entry for proceedings held before Judge Cecilia M. Altonaga: Initial Appearance and ARRAIGNMENT as to Delaney Equity Group LLC (1) Count 1 held on 5/21/2018. Date of Arrest or Surrender: 5/21/18. Total time in court: 1 minutes. Attorney Appearance(s): Jerrob Duffy, Ryan Dwight O’Quinn, Elan Abraham Gershoni, Court Reporter: Stephanie McCarn, 305-523-5518 / Stephanie_McCarn@flsd.uscourts.gov. (ps1) (Entered: 05/21/2018) |

| 05/21/2018 | 9 | PAPERLESS Minute Entry for proceedings held before Judge Cecilia M. Altonaga: Change of Plea Hearing held on 5/21/2018. Delaney Equity Group LLC (1) Guilty Count 1. Total time in court: 25 minutes. Attorney Appearance(s): Jerrob Duffy, Ryan Dwight O’Quinn, Elan Abraham Gershoni, Court Reporter: Stephanie McCarn, 305-523-5518 / Stephanie_McCarn@flsd.uscourts.gov. (ps1) (Entered: 05/21/2018) |

| 05/21/2018 | 10 | PLEA AGREEMENT as to Delaney Equity Group LLC (ps1) (Entered: 05/21/2018) |

| 05/21/2018 | 11 | PAPERLESS NOTICE OF SENTENCING HEARING as to Delaney Equity Group LLC. Sentencing set for 7/26/2018 09:00 AM in Miami Division before Judge Cecilia M. Altonaga. If more than 30 minutes will be required, please contact the courtroom deputy to arrange. Defense counsel shall report immediately to the United States Probation Office for further instructions. (ps1) (Entered: 05/21/2018) |

| 05/22/2018 | 12 | Notice of Presentence Investigation Assignment of Delaney Equity Group LLC to US Probation Officer Vanessa Pulido in the Miami Wilkie D. Ferguson, Jr. U.S. Courthouse and she can be contacted at (305)523-5454 or Vanessa_Pulido@flsp.uscourts.gov. (lrn) (Entered: 05/22/2018) |

Updated 6/27/2018.

See full docket at CourtListener.

Sentencing for Delaney Equity Group is set for 7/26/2018.

Excerpt from the plea agreement:

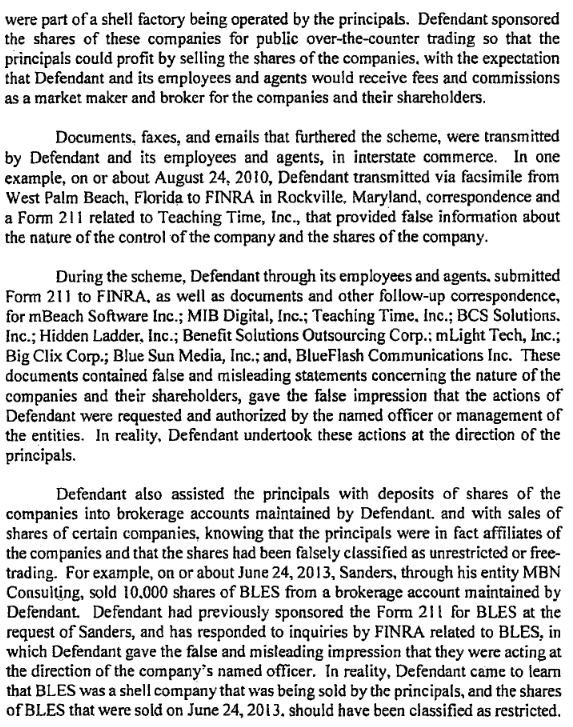

15. The Defendant hereby (i) confirms that it has reviewed the following facts with legal counsel, (ii) adopts the following factual summary as his own statement, (iii) agrees that the following facts are true and correct, and (iv) stipulates that the following facts provide a sufficient factual basis for the plea of guilty in this case, in accordance with Rule 11(b)(3) of the Federal Rules of Criminal Procedure:

Disclaimer. I have no position in any stock mentioned above. I have no relationship with any parties mentioned above. This blog has a terms of use that is incorporated by reference into this post; you can find all my disclaimers and disclosures there as well.