Nothing is perhaps the hardest thing to do. When faced with a difficult situation, it is far easier to do something, anything, than to sit and watch and wait.

Over-activity is deleterious in many situations: in gardening, in building, in thinking, and in investing. The best thing you can do to improve your investing performance is simply to do less trading. This (and the rest of this article) summarizes the work of Brad Barber and Terry Odean in the article “Trading is hazardous to your wealth: The common stock investment performance of individual investors,” published in 2000 in The Journal of Finance.

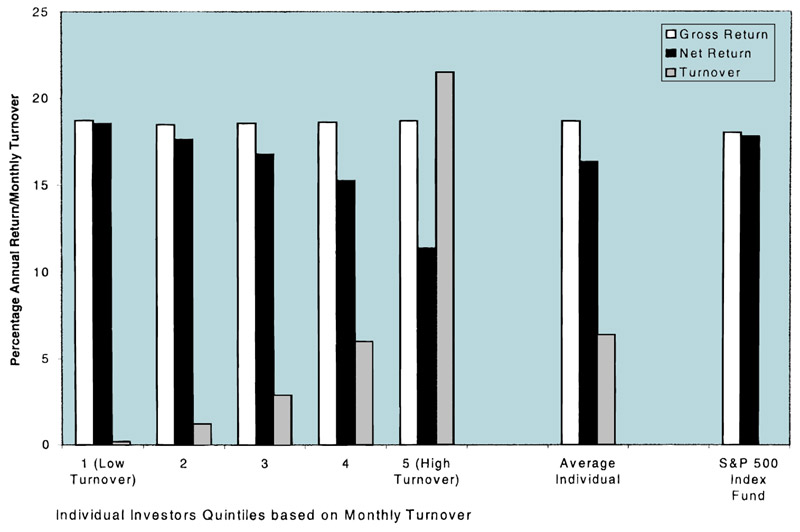

Barber and Odean analyzed the actual broker accounts of 66,000 households over a period of five years, from 1991-1996. Some of their results were quite encouraging: on average, the gross returns of those individual investors were about equal with the gross returns of the S&P 500, indicating that individual investors, by and large, do fine.

The problem was that the ‘investors’ traded way too much. Interestingly enough, it wasn’t the trading per se that hurt their performance: the most active traders had gross returns equal to the least active traders. However, their frenetic trading cost them in commissions, and those costs were huge, reducing annual returns from about 18% to about 12%. See the figure below (taken from the article; a larger version is available here). Notice how low the turnover of the quintile with the least trading is–they had maybe 5% annual turnover. Their net return is thus almost equal to their gross return.

There were some other interesting findings in the study: individual investors tend to favor small, high beta (high volatility) stocks. I would call this the ‘Peter Lynch Effect’, since Lynch recommended small companies with prospects for great growth. This is not really important, though, because it is necessitated by the size of institutional investors. Since institutional investors have so much money to invest, they shun small- and micro-caps. Therefore, individual investors have to own a disproportionate share of small-cap stocks.

Since small stocks tend to outperform the market, individuals should have done better the market as a whole. That they did not is telling. While average investors do not beat the market, good investors can do so. I certainly intend to do so.

Click on the thumbnail below for the full-sized graph of investment performance as it relates to frequency of trading.